Companies

The three minerals indispensable to decarbonization – Richard Mills

2023.08.16

Faced with the grim prospect of falling short of our climate targets, the race to find more minerals needed to accomplish both electrification…

2023.08.16

Faced with the grim prospect of falling short of our climate targets, the race to find more minerals needed to accomplish both electrification and decarbonization becomes ever more important.

The International Energy Agency, which provides analysis and data on the entire global energy sector, forecasts that mineral demand for use in electric vehicles and battery storage will grow at least 30 times by 2040.

Lithium should see the fastest growth, with demand growing by over 40x in its Sustainable Development Scenario, followed by graphite, cobalt and nickel (around 20-25 times). The expansion of electricity networks also means that copper demand could more than double over the same period, the Agency estimates.

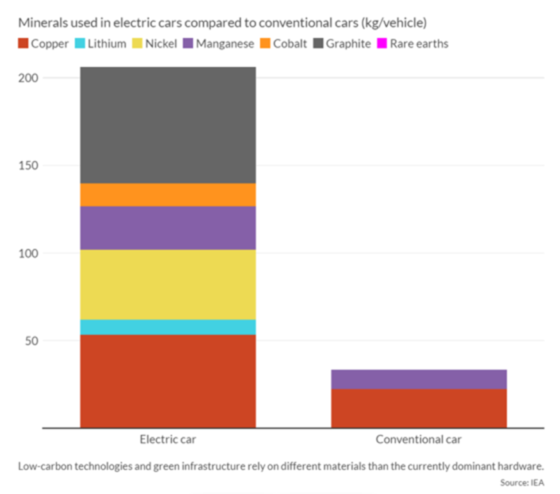

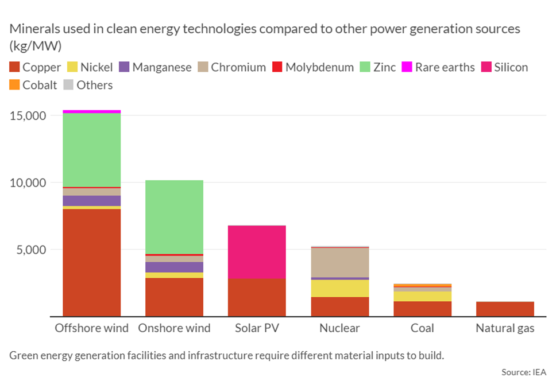

The basis of IEA’s estimation is that solar plants, wind farms and EVs generally require more minerals to build than their fossil fuel-based counterparts. A typical electric car, for example, requires 6x the mineral inputs of a conventional car and an onshore wind plant requires 9x more mineral resources than a gas-fired plant.

To meet the goals of the Paris Agreement, IEA data previously showed that sectors contributing to the green energy transition will be responsible for over 45% of the total copper demand, 61% of the nickel demand, 69% of the cobalt demand, and a whopping 92% of lithium demand by 2040.

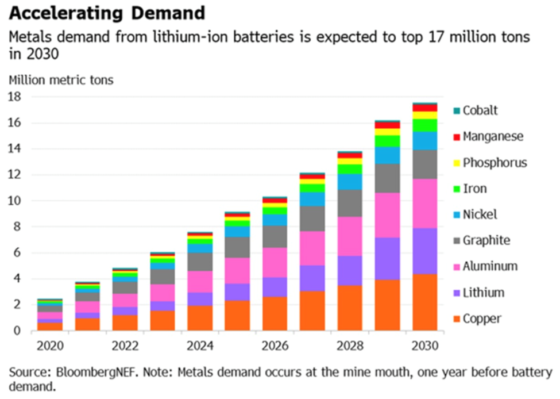

To reach net-zero, demand for these key metals needed for the deployment of energy transition technologies such as solar, wind, batteries and electric vehicles will grow fivefold by 2050, BloombergNEF research finds.

Amongst the minerals required are copper, an essential metal used to build EV charging stations and renewable energy infrastructure; graphite, a vital ingredient in EV batteries; and silver, which is used to make solar panels.

As things stand, all three minerals are on the cusp of significant supply shortfalls (if not already) as global decarbonization efforts continue to gather pace. Below, we detail the importance of each, and more importantly, just how much of these metals the world is actually missing to keep our climate goals alive.

Copper: Heartbeat of Energy Economy

Simply put, electrification doesn’t happen without copper, the heartbeat of the global energy economy.

Along with the usual applications in construction wiring and plumbing, transportation, power transmission and communications, there is now an added demand for copper in electric vehicles and renewable energy systems.

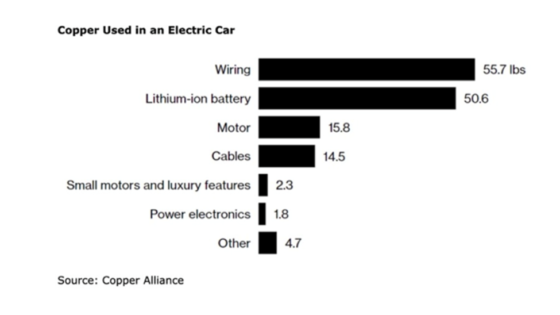

Millions of feet of copper wiring will be required for strengthening the world’s power grids, and hundreds of thousands of tonnes more are needed to build wind and solar farms. Electric vehicles use triple the amount of copper as gasoline-powered cars. There is more than 180 kg of copper in the average home.

However, some of the world’s largest mining companies, market analysis firms and banks, are warning that by 2025, a massive shortfall will emerge for copper, which is now the world’s most critical metal due to its essential role in the green economy.

The deficit will be so large, The Financial Post stated last September, that it could itself hold back global growth, stoke inflation by raising manufacturing costs and throw global climate goals off course.

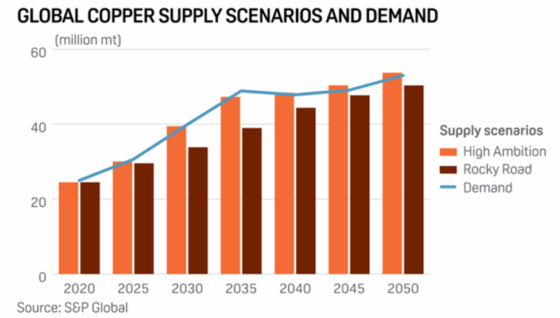

How big are we talking? Well, the speed at which copper demand outpaces supply will depend on the successful meeting of net-zero emission goals. According to a 2022 study by S&P Global, these goals will double the demand for copper to 50 million tonnes annually by 2035. BloombergNEF predicts demand will increase by more than 50% from 2022 to 2040.

“The energy transition is going to be dependent much more on copper than our current energy system,” Daniel Yergin, S&P Global vice chairman, told CNBC. “There’s just been the assumption that copper and other minerals will be there. … Copper is the metal of electrification, and electrification is much of what the energy transition is all about.”

In a scenario that meets the Paris Agreement goals (as in the IEA’s Sustainable Development Scenario), the energy sector’s share of total demand must rise significantly over the next two decades to over 40% for copper.

However, looking further ahead in a scenario consistent with climate goals, the expected supply from existing mines and projects under construction is estimated to meet only 80% of the world’s copper needs by 2030, the IEA says.

According to consulting firm McKinsey, electrification is expected to create a 6.5 million ton shortfall at the start of the next decade, highlighting a substantial output gap that the mining industry has to address.

Graphite: The Essential Battery Mineral

As for the electrification of the global transportation system, it doesn’t happen without graphite. That’s because the lithium-ion batteries in electric vehicles are composed of an anode (negative) on one side and a cathode (positive) on the other. Graphite is used in the anode.

The cathode is where metals like lithium, nickel, manganese and cobalt are used, and depending on the battery chemistry, there are different options available to battery makers. Not so for graphite, a material for which there are no substitutes.

Due to its natural strength and stiffness, graphite is an excellent conductor of heat and electricity. It is also stable over a wide range of temperatures.

Graphite is thus found in a wide range of consumer devices, including smartphones, laptops, tablets and other wireless devices, earbuds and headsets. Besides being integral to electric car batteries, graphite is found in e-bikes and scooters.

Graphite has the largest component in batteries by weight, constituting 45% or more of the cell. Nearly four times more graphite feedstock is consumed in each battery cell than lithium and nine times more than cobalt.

Needless to say, graphite is indispensable to the EV supply chain. BloombergNEF expects graphite demand to quadruple by 2030 on the back of an EV battery boom transforming the transportation sector.

The IEA goes 10 years further out, predicting that growth in graphite demand could see an 8- to 25-fold increase between 2020 and 2040, trailing only lithium in terms of demand growth upside.

Given that demand for graphite is accelerating at a rate never seen before, and the EV industry is now gradually shifting towards natural graphite, the impending supply crunch could get serious.

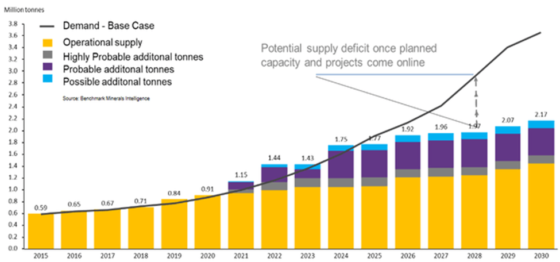

Analysis by Benchmark Mineral Intelligence projects that natural graphite will have the largest supply shortfalls of all battery materials by 2030 — even more than that of lithium — with demand outstripping expected supplies by about 1.2 million tonnes.

And this is just counting EV battery use only; the mining industry still needs to supply other end-users. The automotive and steel industries remain the largest consumers of graphite today, with demand across both rising at 5% per annum.

BMI previously stated that flake graphite feedstock required to supply the world’s lithium-ion anode market is projected to reach 1.25 million tonnes per annum by 2025. For reference, the amount of mined graphite for all uses in 2022 was just 1.3 million tonnes.

The lithium price reporting agency has said as many as 97 average-sized graphite mines need to come online by 2035 to meet global demand.

Silver: Era of Massive Supply Gap

Analysts have long been pointing to a “severe shortage” of silver due to the relentless growth in demand for the metal, which is used in many industrial applications such as automotive and electronics.

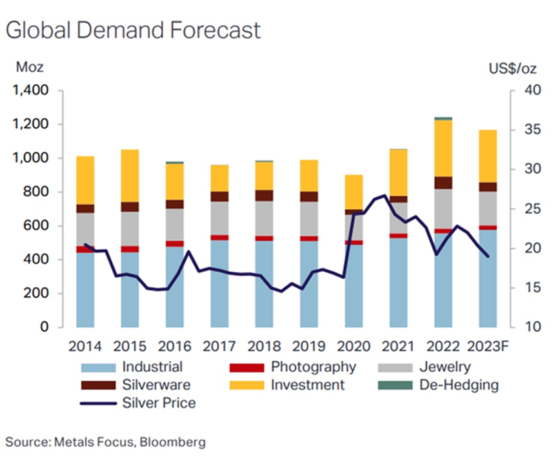

The new industry figures help to paint a clearer picture. Data from the Silver Institute shows that global silver demand has increased by 38% since 2020 as world economies continue to recover from the Covid-19 pandemic.

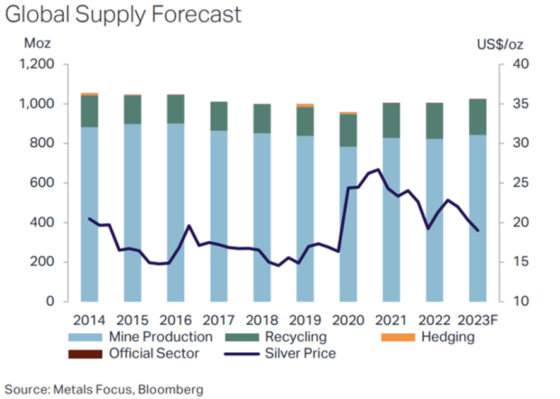

Last year, demand for silver surged by 18% to a record high 1.24 billion ounces against a stagnant supply, stretching the market deficit to a second straight year, the Silver Institute said in its latest publication.

According to the 2023 World Silver Survey, the global silver market was undersupplied by 237.7 million ounces in 2022, which the Institute says is “possibly the most significant deficit on record.”

What’s more unsettling is that it took just two years of undersupply — the 2022 deficit and the 51.1 million oz shortfall from 2021 — to wipe out the cumulative surpluses from the previous decade, and this demand-supply gap is likely to remain for the foreseeable future.

“We are moving into a different paradigm for the market, one of ongoing deficits,” said Philip Newman at Metals Focus, the research firm that prepared the Silver Institute’s data.

This year, we are most likely going to see a repeat of last year, with solid demand and a slight increase (2%) in mine production.

The Silver Institute is forecasting another 1.17 billion ounces being demanded this year, against a projected supply of 1.02 billion ounces. While this would close the gap to 142.1 million ounces, it would still be the second-largest deficit in over two decades.

Looking into the next decade, the Institute is expecting demand — and hence the supply shortall — to grow even further as the global transition to renewable energy intensifies.

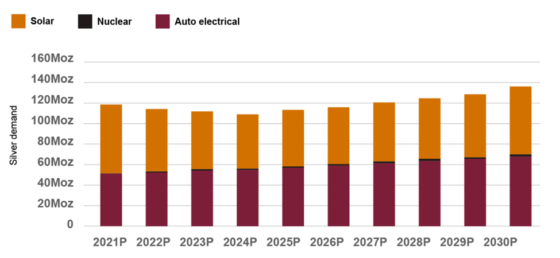

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. A 2020 Saxo Bank report stated that “potential substitute metals cannot match silver in terms of energy output per solar panel.

Using silver as conductive ink, photovoltaic cells transform sunlight into electricity. Silver paste within the solar cells ensures the electrons move into storage or towards consumption, depending on the need. It is estimated that approximately 100 million ounces of silver are consumed per year for this purpose alone.

Analysis by BMO Capital Markets has annual silver consumption by the solar industry growing even higher at 85% to about 185 million ounces within a decade.

In the Silver Institute’s report, demand from photovoltaics climbed 15% last year to 140.3 million ounces, and is expected to surge another 28% to 161.1 million ounces in 2023, by which demand would’ve been about three times that of 2015.

Longer term, demand from the solar market is expected to keep up this pace. The institute, which references a World Bank projection for the energy technology segment as a basis for its predictions, forecasts that consumption could eventually hit 500 million ounces by 2050.

And without a sudden, large injection of supply, it won’t be surprising to see the current silver deficit extend beyond the end of this decade while setting new records along the way.

Projects of Interest

The message is clear: the world needs more mines (copper, graphite, silver) to come online over the coming years to avoid a significant supply deficit that derails our decarbonization goals. This starts with identifying the right projects in favorable mining jurisdictions that can be developed in a timely manner.

Fortunately, many of the companies featured here on AOTH have exploration assets that fit this profile and should warrant the industry’s attention for their growth potential.

Max Resource

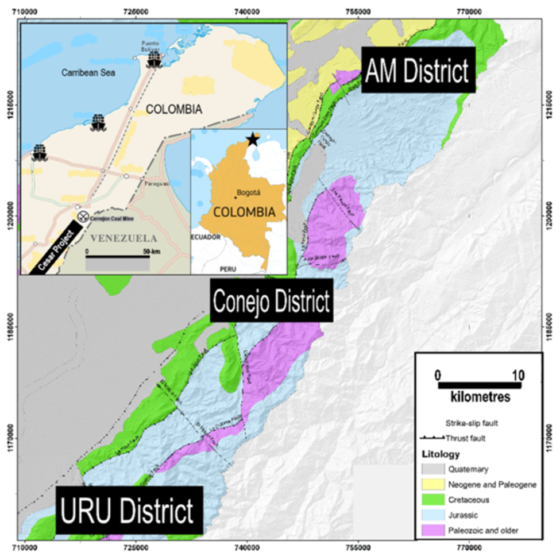

For copper, we have Max Resource Corp (TSX.V:MXR, FSE:M1D2, OTC:MXROF), which currently holds the largest area prospective for the metal in Colombia’s Cesar sedimentary basin, with mining concessions collectively spanning over 188 km².

The company’s flagship project, named CESAR after the prolific mineral-rich basin, is situated along the world-famous Andean Copper Belt, where silver is also abundant. The property is considered to be district-scale, divided between three major copper-silver zones (AM, Conejo & URU) that are individually located along a 90 km long belt.

Currently, there are two primary depositional models being used for the CESAR project.

The sediment-hosted stratiform copper-silver mineralization found in the southern end (URU and Conejo zones) of its Cesar project is interpreted to be analogous to the Central African Copper Belt (CACB), while the northern end (AM zone) is compared to the Kupferschiefer deposits in Poland.

It’s estimated that nearly 50% of the copper known to exist in sediment-hosted deposits is contained in the CACB, headlined by Ivanhoe’s 95 billion lb. Kamoa-Kakula discovery in the Democratic Republic of Congo.

Kupferschiefer, considered to be the world’s largest silver producer and Europe’s largest copper source, is a mining orebody ranging from 0.5 to 5.5m thick at depths of 500m, grading 1.49% copper and 48.6 g/t silver. The silver yield is almost twice the production of the world’s second-largest silver mine.

Exploration on the AM mining concessions so far this year has confirmed Max’s hypothesis that the mineralization found at the northern end of its property is sediment-hosted and stratiform, similar in style to the Kupfershiefer.

Copper Road Resources

Another copper exploration company to monitor is Copper Road Resources Inc. (TSXV: CRD), which is looking to leverage the geological advantage offered by one of the world’s greatest continental rifts.

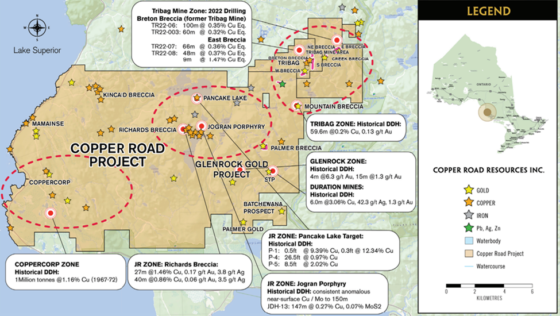

The company’s namesake property covers 21,000 hectares within the Batchewana Bay district, about 85 km north of Sault St. Marie, making it just one of few copper developments on the Ontario side of the mineral-rich Mid-Continental Rift.

The property package has a proven history of copper production, containing two former mines: The Tribag mine processed 1 million tonnes at 1% Cu, and the Coppercorp mine with historic production of 1 million tonnes at 1.16% Cu.

There are several confirmed zones of mineralization within property boundaries — Tribag, Glenrock, JR (Richards/Jogran) and Coppercorp — each hosting multiple targets for exploration. Together, they span a total length of 30 km.

The company is currently focused on two zones of known near-surface mineralization at Tribag and JR, which are approximately 12 km apart.

The former Tribag mine represents a porphyry-style copper deposit, consisting of four breccias (Breton, West, East, South). Its reported historical production (1967-1974) was predominantly from the Breton breccia.

Historical estimates by Teck Resources, its former operator (1966-1972) and a household name in the Canadian mining industry, identified 40 million tonnes at 0.4% copper from the Breton breccia, and estimated 125 million tonnes at 0.13% copper and 0.05% molybdenum from the East breccia.

Renforth Resources

Quebec-focused Renforth Resources (CSE:RFR, OTCQB:RFHRF, FSE:9RR) recently expanded its exploration portfolio with the acquisition of two projects in Ontario, one of which is known to host copper mineralization.

The Copper Prince project consists of 15 claims that cover part of a known copper-bearing vein system (Copper Prince) with limited historic production, and a less well-documented vein/disseminated copper system (North Summit).

Historic work on the Copper Prince system (partially covered by Renforth claims) began in the 1920s, when trenching, drilling and limited underground development was completed by the Consolidated Mining and Smelting Company of Canada (Cominco). Historically recorded assays from the Renforth portion of the property include several copper values exceeding 1%, along with low-grade gold and silver values.

The acquisition of the Copper Prince project allows Renforth to diversify its project portfolio headlined by the Surimeau district-scale property in Quebec, which hosts several areas prospective for gold/silver and battery/industrial metals (nickel, copper, zinc, lead, cobalt, lithium and manganese).

For the better part of two years, Renforth’s exploration focus has been on the more advanced Victoria mineralized battery metals horizon and parts of the longer Lalonde horizon lying parallel to the north.

Victoria is a ~20-km-long magnetic structure bearing nickel, copper, zinc and cobalt mineralization at surface. It stretches between the Victoria West mineralization, which has been drilled over 2.2 km, and the Colonie mineralization, drilled and surface-sampled by Renforth in the eastern part of the property.

The Lalonde mineralization, ~3 km north of Victoria West, was only recently drilled by Renforth. This surface mineralized system, similar to Victoria, currently stretches over ~9 km of ground-truthed strike.

Both zones are about 250-500 meters thick, running east-west across the central portion of the property. The two systems are interpreted by the company as two arms of a fold, with the fold nose located off the property and to the east.

While the defined area of mineralization spans a total length of ~29 km, which by industry standards is a long distance to cover, this is still just a small portion of a district-scale property that remains underexplored.

Dolly Varden Silver

In terms of silver exploration companies, few can match the growth potential of Dolly Varden Silver (TSXV:DV, OTC:DOLLF), whose flagship asset covers 163 square kilometres of BC’s Golden Triangle, a region that has seen $5 billion in M&A activity since 2018.

The land package, which combines the company’s original Dolly Varden silver project and the newly acquired Homestake Ridge gold-silver project, is said to host one of the largest undeveloped high-grade precious metals assets in all of Western Canada.

The combined mineral resource of its consolidated Kitsault Valley property is estimated at 34.7 million oz of silver and 166,000 oz of gold in the indicated category and 29.3 million oz of silver and 817,000 oz of gold in the inferred category.

While the resource is already impressive at this stage, the more fascinating aspect of the project is its rich history, which can be traced back to the early 20th Century when Scandinavian prospectors first made the silver discovery in what is now the Stewart Complex.

Within the boundaries of the company’s original property are two past-producing silver mines: Dolly Varden and Torbrit, which formed a prolific silver mine camp starting in 1919 that produced more than 20 million ounces in the span of 40 years, with assays of ore as high as 2,200 ounces per tonne.

It should be noted that Dolly Varden was amongst the most important silver mines in the British Empire during its heyday.

Other historically active mines in this area include North Star and Wolf, which remain underexplored to this day. Together, the four deposits comprise about 90 sqkm within the Stewart Complex.

While these deposits were already enough to work with, DV always believed that the Kitsault Valley property is prospective for hosting more precious metal deposits, being on the same structural and stratigraphic belts that host numerous other high-grade deposits on the same trend such as Eskay Creek and Brucejack.

Graphite One

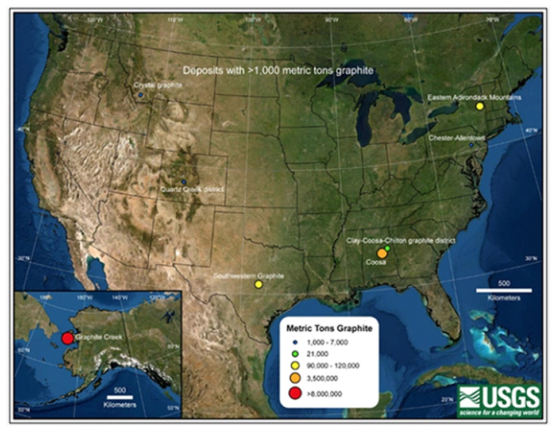

Graphite projects are few and far between simply because China has dominated the mineral’s supply chain for years, and many countries have solely relied heavily on Chinese imports. One of those is the United States, which has just started to realize the importance of producing graphite domestically during the clean energy era and is willing to make the necessary investments to build up its own supply.

Its largest graphite resource, as identified by the US Geological Survey, is the Graphite Creek deposit in Alaska, which has 1.93 million tonnes of natural graphite in measured resource and 12.3 million tonnes inferred.

The deposit is being developed by Vancouver-based Graphite One (TSXV:GPH, OTCQX:GPHOF) as part of its Graphite Creek property situated along the northern flank of the Kigluaik Mountains, spanning a total of 18 km.

In early 2021, Graphite Creek was given High-Priority Infrastructure Project (HPIP) status by the Federal Permitting Improvement Steering Committee (FPISC), which is responsible for the environmental review and authorization process for certain large-scale critical infrastructure projects.

The HPIP designation allows Graphite One to list on the US government’s Federal Permitting Dashboard, which ensures that the various federal permitting agencies coordinate their reviews of projects as a means of streamlining the approval process. In other words, the Graphite Creek project will likely be fast-tracked to production.

Last fall, Graphite One underwent a major de-risking event with the release of a prefeasibility study (PFS), which portrays the Graphite One project as highly profitable, with expected costs of $3,590 per tonne measured against an average graphite price of $7,301 per tonne.

Once up and running, the mine would produce, on average, 51,813 tonnes of graphite concentrate per year during its projected 23-year mine life. The company itself would produce about 75,000 tonnes of products a year, of which 49,600 tonnes would be anode materials, 7,400 tonnes purified graphite products and 18,000 tonnes unpurified graphite products.

The PFS is based on the exploration of only one square kilometer of the 16-km deposit, meaning that it could easily crank up production by a factor several times the current (proposed) run rate of 2,860 tonnes per day.

Given its significant graphite resource, which the USGS now places amongst the world’s largest, and the exploration upside, the company has the foundation to achieve its goal of becoming the first vertically integrated producer to serve the domestic EV battery market.

Last month, the project was given a vote of confidence from the US Department of Defense, which awarded Graphite One with a technology investment grant of $37.5 million under Title III of the Defense Production Act.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

tsx

tsxv

cse

otc

otcqb

otcqx

ax

gold

silver

lithium

cobalt

manganese

nickel

copper

zinc

molybdenum

tsxv-dv

dolly-varden-silver-corporation

tsxv-gph

graphite-one-inc

cse-rfr

renforth-resources-inc

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…

GoldTalks: Going big on ASX-listed gold stocks

Aussie investors are spoiled for choice when it comes to listed goldies, says Kyle Rodda. Here are 3 blue chips … Read More

The post GoldTalks: Going…

Gold Digger: ‘Assured growth’ – central bank buying spree set to drive gold higher in 2024

Central banks will drive the price of gold higher in 2024, believe various analysts Spot gold prices seem stable to … Read More

The post Gold Digger:…