Companies

Copper: indispensable but under-appreciated – Richard Mills

2023.04.21

For years AOTH has been reporting on how a decline in productivity from existing copper mines, driven by open-pit to underground expansions,…

2023.04.21

For years AOTH has been reporting on how a decline in productivity from existing copper mines, driven by open-pit to underground expansions, a decline in ore quality and resource nationalism has been combining with a lack of new discoveries caused by a shortage of investment in exploration, to produce a shortfall of mined copper supply at exactly the wrong time. i.e. just as the demand for the red metal is ramping up due to the global electrification (of the transportation system) and decarbonization trend.

Some of the world’s largest mining companies and metal traders are warning that by 2025, a massive shortfall will emerge for copper, which is now the world’s most critical metal due to its essential role in the green economy.

The deficit will be so large, The Financial Post stated, “that it could itself hold back global growth, stoke inflation by raising manufacturing costs and throw global climate goals off course.”

Along with the usual applications, in construction wiring and plumbing, transportation, power transmission and communications, there is the added demand for copper in electric vehicles and renewable energy systems.

Millions of feet of copper wiring will be required for strengthening the world’s power grids, and hundreds of thousands of tonnes more, are needed to build wind and solar farms. Electric vehicles use over twice as much copper as gasoline-powered cars, which contain about 30 kg. An offshore wind turbine contains 8 tonnes of copper per megawatt of generation capacity. There is more than 180 kg of copper in the average home. The Biden administration plans to replace all the nation’s lead water pipes with copper piping.

Yet despite copper’s indispensable role in the modern economy, its criticality goes largely unrecognized, unlike, say, lithium, cobalt, manganese or graphite — used in electric vehicle batteries. All of these battery metals appear on the US critical minerals list, but not copper.

The US Geological Survey defines a critical mineral as:

1/ essential to economic and national security

2/ playing a key role in energy technology, defense, consumer electronics and other applications

3/ its supply chain vulnerable to disruption

By these three criteria, copper is clearly critical. So why was it omitted?

I won’t deny the importance of battery metals in making the transition from fossil-fueled power to electric and renewable. We are going to need more, much more, of these raw materials, too.

I just can’t understand why there isn’t more of an outcry from governments, who let’s face it are driving electrification & decarbonization, with their carbon reduction targets, about how a lack of copper supply could stop E&D in its tracks. They should be banging down the mining industry’s door to explore for and mine more copper, and doing as much as they can to remove obstacles to mining and mineral processing. The fact that they’re not, shows the failure of governments to understand how natural resources, in particular forward-facing metals like copper, should be managed.

Copper and the green transition

According to McKinsey, a consulting firm, electrification is expected to increase annual copper demand to 36.6 million tonnes by 2031, with supply forecast to be around 30.1Mt, creating a 6.5Mt shortfall at the start of the next decade.

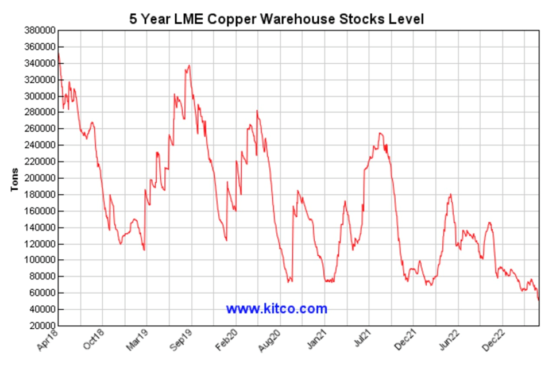

Copper stockpiles in London Metal Exchange (LME) warehouses are at their lowest in 18 years, currently sitting at least than a week’s worth of consumption.

“The market overall is pretty tight,” said Robert Edwards, copper analyst at CRU, in a recent Wall Street Journal piece. “Longer term there’s a narrative around resource scarcity and the green transition with EVs and renewables as well as the build-out of electricity grids. On paper it’s quite a substantial supply gap opening up over the next 10 years.”

How are we going to find the copper?

Increasing mine output has proved a challenge, prompting a wave of deal-making in the copper sector. Mining.com reports that “top miners are hungry for copper assets as demand for the metal accelerates and a global shortfall looms,” with BHP, Rio Tinto and Glencore all having disclosed they are seeking to grow their copper exposure. Gold majors including Newmont and Barrick have indicated they are interested in adding more copper to their metals mix.

Glencore has for weeks been trying to acquire Canadian diversified miner Teck Resources, thus creating the world’s third largest copper mining company. BHP on Monday gained court approval for the takeover of OZ Minerals, a deal valued at $6.34 billion.

A lot of companies would rather buy mines than build them. An analyst quoted by WSJ said prices would need to rise to $15,000 a tonne to incent new mines. Copper futures currently trade at around $9,000/t.

Among the issues impeding new supply are lower ore grades, depletion of existing mines, a lack of new discoveries, and resource nationalism in three of the main copper-producing countries: Chile, Peru, and the DRC.

Reluctant governments in the United States and Canada have not inspired much hope of new copper supply in North America, where it can take up to 20 years to build a mine. The Biden administration has prevented or stood in the way of new mining properties in Minnesota, Arizona and Alaska.

Yet copper demand is booming, especially for green applications. An analyst at Goldman Sachs was quoted saying that green uses of copper are expected to increase from 4% of total copper consumption in 2020 to 17% by 2030. A “net zero emissions” path would mean the world needs an additional 54% of copper on top of that forecast.

Chile developments

Chile serves as a good example of why new copper supply is so hard to come by.

The country’s output has stagnated due to deteriorating ore quality and water restrictions in the arid north. Permitting is also getting tougher.

Research firm Fitch Solutions estimates 2023 copper production in the world’s top producer will be about 5.7Mt, the same as in 2020.

In 2021, leftist candidate Gabriel Boric was elected president of Chile, on a mandate to impose higher taxes, sending a chill through the mining industry which argued the change would impede competitiveness.

Constitutional reform was also on the agenda. Since then, cooler heads have prevailed. A proposed new constitution was rejected by voters last September, while an ambitious tax overhaul plan was voted down by Congress in March.

A government plan for new royalties on mining, currently moving through Congress, has been tempered to 46%.

Large mining companies have been watching these developments closely. BHP, majority owner of the world’s biggest copper mine, Escondida, wants the Chilean government to make further concessions on the tax legislation before investing an estimated $10 billion in the country. A BHP executive says Chile’s major competitors have a tax burden of 41 to 43%.

The company also says it is obligated to expand Escondida and is looking to tap what BHP’s President, Minerals Americas Ragnar Udd calls “a fantastic sulfide deposit” at its Cerro Colorado in northern Chile.

Canada’s Lundin Mining and US copper giant Freeport McMoRan, meanwhile, have been vocal about their concerns in Chile. The latter has said it will pause expansion plans, citing political uncertainty.

Lundin is more confident, agreeing last month to pay $950 million for 51% of Chile’s Caserones copper mine. The company is considering raising its stake to 70% mine for an additional $350 million. The addition of Caserones would boost Lundin’s copper output by 50%, adding to the Candaleria mine it already operates, 160 km away.

Reuters notes that Lundin’s purchase from JX Nippon Mining & Metals comes at a time when companies are seeing longer delays for permits as opposition has risen from local communities. Some projects have been rejected by the state or by courts on environmental impact concerns.

Teck has submitted for environmental approval this year, a $3 billion project to increase capacity at its Quebrada Blanca 2 mine.

Peru

[For] three months, vital highways were choked off by boulders and burning tyres, lucrative copper mines were paralysed and the rail lines leading to the ancient Inca citadel, like much of Peru’s economy, were ground to a halt amid shockingly violent demonstrations. (Al Jazeera, March 10, 2023)

Although the unrest has faded, Bloomberg reported earlier this week that miners are struggling to move tens of thousands of tons of copper concentrate from the Andes mountains to ports.

Peruvian copper exports fell 20% in January and February even as production climbed, leaving mining companies with excess stored inventory that has contributed to tight global supplies.

Exports at Las Bambas were most affected — the joint venture shipped 55% less copper in the first two months of the year compared to the same period last year — but the top three copper miners also saw two-digit declines, Bloomberg said. Exports from Antamina, co-owned by BHP and Glencore, were down 11%, Cerro Verde’s (Freeport McMoRan) fell 24%, and exports from Grupo Mexico’s Southern Copper Corp. dropped 23%.

As the major copper miners deal with logistical problems in Peru, at least one major mining company is looking to bring on new supply.

Vale SA has reportedly been looking for copper deposits in Peru, including two early-stage projects known as Umami and Chaska.

The Brazilian iron ore giant holds copper concessions in 17 of Peru’s 24 states, and has bought as many as 1,200 separate mining rights, half of those active totaling 450,000 ha, according to a government agency.

It is extremely interesting, from my point of view, and highly unusual, to see a major mining company like Vale taking an interest in such greenfield copper projects. Majors typically lack the exploration expertise and shy away from the risk associated with such early stage projects, preferring to leave the development of early-stage properties to the juniors.

Apparently Vale’s move is part of the firm’s plan to separate its base metal assets — nickel and copper — so as to unlock value as demand for battery metals picks up.

Bids for Teck

Canada’s Teck Resources is doing the same thing, in its case spinning off its steelmaking coal business to focus on base metals, particularly copper and zinc.

Experts correctly predicted that the split would make Teck, which owns four copper mines in South America and Canada, a takeover target.

A few weeks after the spin-off was announced, Switzerland’s Glencore, currently the world’s largest mining company, launched a $23.1 billion hostile takeover bid. The deal would create two new companies combining their respective metals and coal businesses.

However, it was rejected by the Teck board and its controlling shareholder, Norman Keevil, despite Glencore sweetening its initial bid with an $8.2 billion cash component.

Yet even if the takeover bid fails — Glencore has until the April 26 vote on whether to split the company to convince shareholders — there are other suitors waiting in the wings. Such is the interest in companies with significant copper assets right now.

Mining.com reported that Teck has been approached by Vale, Anglo American and Freeport-McMoRan, on potential deals for its base metals business. In fact the trio are among six companies that have expressed interest in the Canadian miner, post-split, states Toronto-based newspaper The Globe and Mail.

With all that is going on with copper — record-low LME inventories, a flurry of M&A, low ore grades, more complicated metallurgy, mine depletion, a lack of new discoveries, resource nationalism, and of course, demand for the metal steadily increasing as E&D ramps up, it’s curious why the copper price is now under $4 a pound, after reaching its best-ever $5.02/lb in May, 2022.

China

Arguably the only reason why copper isn’t higher is due to continued worries about China. The world’s largest copper consumer sharply reduced its copper imports during the first quarter of 2023.

However, there are high expectations of the Chinese economy getting back to normal following last year’s covid-19 restrictions.

Zero Hedge reported that China’s delayed “liftoff was imminent”, and that “it is once again China that is — willingly or otherwise — set to serve as the world’s growth dynamo at a time when the entire developed world is about to max out at the same time. This is precisely what happened in 2008 when China unleashed the biggest credit expansion in modern history, sparking not only historic growth spree but also an exponential debt increase that sent China’s debt to over 300% of GDP.”

The country’s first-quarter GDP surprised to the upside by growing 4.5%, the strongest performance since Q1, 2022, fueled by exports and infrastructure investment, as well as a rebound in retail consumption and property prices.

While Q1 growth missed the government’s 5% full-year target, economists expect it to pick up pace as the year progresses.

“Definitely the recovery’s on track,” said Tao Wang, UBS chief China economist.

Citigroup economists upgraded their 2023 GDP growth forecast to 6.1% from 5.7% previously, after seeing strong data. Manufacturing investment rose 7% in the first quarter and industrial output gained 3%. The jobless rate fell to 5.3% in March from 5.6% in February. New home prices climbed at their fastest pace in 21 months.

The bright forecasts for Chinese growth bode well for the copper market. Research by the International Copper Association found that Belt and Road projects in over 60 Eurasian countries will push the demand for copper to 6.5 million tonnes by 2027. And this was before Beijing’s most recent Five-Year Plan, that calls for developing high-speed rail, power infrastructure and new energy.

As infrastructure needs multiply, copper supply can’t keep up

The European Union’s “Green Deal” aims to make the continent climate neutral by 2050, with funding mechanisms totaling over €1 trillion.

President Joe Biden plans on spending $2 trillion on remaking the American economy, hoping to “build it back better”.

According to S&P Global, Among the metals-intensive funding in the [Infrastructure Investment and Jobs Act] is $110 billion for roads, bridges, and major projects, $66 billion for passenger and freight rail, $39 billion for public transit, and $7.5 billion for electric vehicles.

Again I have to ask, where are we going to find the copper? Without a serious push to develop new mines, the supply deficit predicted by 2025 is going to arrive even sooner.

Where are the world’s future copper mines?

All of the recent deal-making in the copper space has got me thinking, “Who’s next”? The majors are buzzing around Teck like bees on flowers and Vale is even looking to develop exploration-stage properties in Peru — activities typically done by juniors. It just shows that they are starting to work their way down the food chain.

I predict juniors will become targets right across the geographical and mine development spectrum, because they own the world’s next copper mines. Anybody with a copper deposit that has the grades and the scalability to interest a major will become the belle of the ball.

Gold miners are also looking at copper, reflecting the rising profile of the red metal. Indeed people ignore copper at their peril, because as I’ve said many times before, nothing happens without it. No electric vehicles, no charging stations, no renewable power, smart power grids, transmission lines, 5G, etc.

Problem is, the massive and increasing demand for copper is like a hammer blow to dwindling supplies. The mining industry simply must find more of it, to avoid this fatal flaw in the electrification and decarbonization thesis.

New supply is coming online, but little of it is coming to the West. The handful of new copper mines already have offtake agreements that guarantee a pre-determined amount of production is shipped to Asia.

We can hardly call this situation Western security of supply, when most of the raw copper material (cathodes or concentrate) is going to China, South Korea and Japan, who then turn around and sell more expensive copper end products to North America and Europe.

Three of the biggest copper producers — Chile, Peru and the DRC — are becoming less reliable due to resource nationalism. These countries have a lot of poverty, inequality is rampant, and governments face constant pressure to increase resource rents.

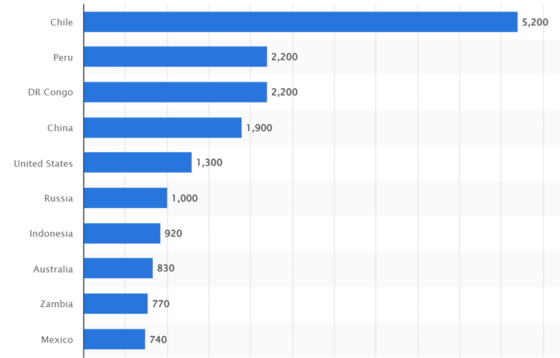

Major countries in copper mine production worldwide in 2022(in 1,000 metric tons)

Why don’t we develop more copper mines in North America? Well the mining industry is trying, but there are many obstacles. As mentioned the Biden administration has already blocked copper mines in three states.

Look no further than northwestern British Columbia.

“53 per cent of the exploration spending in B.C. in 2020 went to the northwest of the province, home of the Golden Triangle exploration and mining district around Stewart B.C.” Gordon Clarke, director of the B.C. Mineral Development office

“The great mineral endowment of the Iskut district is due to its location along intersecting sets of long lived deep crustal lineaments that provided conduits for magmas and fluids during a succession of tectonic regimes… Such lineaments provide ideally fertile ground and permeability conditions that can, and do, result in near-superposition of vastly different mineral deposit types.” JoAnne Nelson, Emeritus Scientist with the British Columbia Geological Survey (BCGS)

Major porphyry camps and porphyry-related gold deposits within the Golden Triangle include: Schaft Creek, Galore Creek, the Red Chris-GJ-North Rok-Tatogga cluster and the KSM-Brucejack and Snip Bronson camps.

Chief among the GT’s deposits/ camps is the giant Kerr-Sulphurets-Mitchell (KSM) deposit being developed by Seabridge Mining.

The copper-gold-silver porphyry, and its estimated mineral content, is spectacular — Sulphurets’ 199 million ounces of gold and 790Moz of silver makes the KSM project, being advanced by Seabridge Gold, the largest undeveloped gold deposit in the world. It also has 51 billion pounds of contained copper.

In fact, based strictly on its copper content, Sulphurets would rank 14th on the USGS list; if its gold value is counted, Sulphurets would be number 5.

Nobody therefore can argue that Sulphurets doesn’t rank as among the monster porphyry gold systems in the world.

Interesting fact: The Sulphurets Hydrothermal System is effectively the porphyry system that generated KSM, Ironcap, Treaty Creek and Brucejack.

The current resources of KSM, Treaty, Snowfield and Brucejack are: 199Moz gold, 730Moz silver and 51B pounds Cu in a 20 km circle representing one of the greatest concentrations of metal value on the planet.

But the Sulphurets Hydrothermal System is just one of many hydrothermal systems in the Golden Triangle.

Porphyry copper-gold deposit Galore Creek, explored in the 1960s and 70s, now owned jointly by Newmont (TSX:NGT) and Teck Resources (TSX-B:TECK), has 9 billion pounds of copper, 8 million gold ounces and 136 million ounces of silver.

Another porphyry, Schaft Creek, a JV between Copper Fox Metals (TSXV:CUU) and Teck, contains 7.7 billion pounds of copper, 6.9 million ounces of gold, 511 million pounds of molybdenum and 54.2 million ounces of silver. (2021 mineral resource estimate)

Red Chris had reserves of over 300 million tonnes grading 0.359% copper and 0.274 g/t gold, plus additional low-grade silver, however, the known resources outside the open pit model are ten times that amount. First run by Imperial Metals, then 70%-purchased by Australia’s Newcrest in 2019, this $700 million gold and copper mine entered production in 2015 and is expected to go until 2043.

Newmont now owns GT Gold and its Tatogga gold-copper discovery in the Golden Triangle. Tatogga is located about 14 km west of Red Chris and includes the primary Saddle North asset.

All the copper mined in British Columbian is shipped to Asia.

The only copper processing facilities in Canada are the Horne smelter in Rouyn-Noranda, Quebec, and the CCR refinery in Montreal.

Why don’t we process it here? British Columbia’s northwest would be an excellent place to shore up new copper supply and to build, close to tidewater, smelting and refining capacity.

There has been a lot of small talk about building a copper smelter in BC for years, but so far the political will hasn’t been there.

It’s a great idea.

CESL Process

The smelter’s ore feed could not only be derived from KSM, but all of the neighboring deposits, including Red Chris, Schaft Creek, Galore Creek, Newmont’s Tatogga, and no doubt from the many deposits already discovered and waiting to be discovered. Elsewhere in BC Tech’s partially owned Highland Valley, Gibralter and Copper Mtn could potentially supply feedstock for a BC copper smelter/hydromet. And the Yukon has a lot of copper, Carmacks and Casino for example.

The key to this plan, wild as it may seem, is the smelter must have the ability to process copper and gold. Well it just so happens that Teck Resources, part-owner of Highland Valley, Galore Creek and Schaft Creek, has the technology to do it.

Cominco Engineering Services (CESL), a subsidiary of then-Teck Cominco Metals, began developing the CESL Process in 1992, as an alternative to conventional smelting and refining of copper concentrates for the production of LME Grade A copper cathode.

The proprietary hydrometallurgical processes are for the treatment of nickel, copper and copper-gold concentrates. According to a technical paper, Besides successfully treating standard concentrates, the processes have a demonstrated capability to refine “dirty” concentrates containing fluoride, arsenic, bismuth and other impurity elements that pose serious challenges in conventional smelting.

The first commercial facility constructed using CESL technology was built by Vale in the Carajas region of Brazil. The 10,000 tonne per year CESL copper plant was reportedly intended to be a prototype, supporting construction of a much larger plant to process nearby concentrates from future Vale projects.

The plant was successfully able to meet all objectives including training personnel in the region and demonstrating the technology on a commercial scale, according to Teck:

In 2002 through 2005, pilot-scale test work conducted by CESL indicated that gold was recoverable through cyanidation of the copper plant residue. Preliminary results have shown exceptional gold extraction and minimal cyanide consumption.

Conclusion

If Teck’s CESL Process was brought to somewhere in the Golden Triangle, seemingly the ideal location for a new refinery, considering all the copper-gold deposits grouped so closely together, it could prove to be just what the area needs, i.e., the key to unlocking the huge mining potential of the Triangle which up until now, has stayed locked within the area’s vast copper-gold porphyries and epithermal gold deposits.

A shared refinery would lower each project’s transportation costs and make the economics workable even if copper and gold prices were to fall, which seems unlikely given current market conditions.

Although we envision the world’s copper majors supporting a refinery, in a kind of “build it they will come” scenario (some are already there, including Teck, Newmont and Newcrest), we don’t see this happening without government backing. Refineries cost hundreds of millions, and no company is likely to take it on, alone, or even through a partnership.

Consider: while it is usually better for governments to stay out of the way of markets, there are cases when pushing industry in a certain direction can make a difference.

An example is what happened when Robert Friedland’s Diamond Fields sold its Voisey’s Bay nickel discovery to Inco, then the world’s largest nickel producer, for $4.3 billion.

If Inco wanted to extract minerals in Newfoundland, the provincial government maintained that they had to build a processing plant. As a result of negotiations, hundreds of millions of dollars in research funding went into the development of “hydromet” (hydrometallurgy) mineral processing technology to replace the normal smelting process. Hydromet is better for the environment and gets better recoveries.

And it’s not like there hasn’t been a precedent set in British Columbia. In the 1940’s, the government wanted to develop BC’s considerable natural resources particularly in the sparsely populated northwest and northcentral regions. A survey of the hydroelectric power potential, done in the 1920’s, identified the Nechako watershed, a vast river and lake system draining 14,000 square kilometers of northcentral BC.

Aluminum producer Alcan was invited by the government to investigate the concept of developing an aluminum industry in the area.

The resulting Kitimat-Kemano project in its day was the largest privately funded construction undertaking in Canada. It cost $500 million in 1950 dollars, or more than $3.3 billion in today’s currency.

Some remarkable engineering feats were achieved, including: building the largest rockfill dam in the world at the time; constructing the Kenney Dam 193 km east of the Nechako reservoir; completing an 82-km power transmission line from the former town of Kemano to Kitimat, built at an elevation of 1,500m through rugged mountain territory; and boring 16 kilometers through coastal mountains to complete a water intake tunnel as wide as a two-lane highway, to carry river water to the twin penstocks of the Kemano powerhouse, where it tumbles 800 meters, nearly 16 times the height of Niagara Falls, to drive the generator turbines.

Located 75 km southeast of Kitimat, the Kemano Generating Station was completed in 1954, providing hydroelectricity for Alcan’s Kitimat aluminum smelter. The cathedral-shaped powerhouse, drilled and blasted 427m inside the granite base of Mt. DuBose, produces 896 megawatts of power from its eight generator units, making it the largest power producer in the province when it was built in the early 1950’s. Even today, the 67-year-old facility is the biggest high-pressure hydropower generation facility in North America.

A 2016 upgrade involved a $6 billion investment to upgrade the smelter, using technology to lower its carbon footprint and make the smelting process more efficient and cost-competitive. In 2017 Rio Tinto approved $600 million for a second tunnel.

The new, second, 16-kilometre tunnel was filled up with water and produced its first megawatt of electricity in July 2022 after its construction was completed in May 2022. Both T1 and T2 are now operating together

Back on point, it is our opinion that, with northwestern BC’s exceedingly rich mineral endowment — an estimated 188 million ounces of gold reserves (47.7Moz proven and probable), 1.2 billion ounces of silver (214Moz P&P) and 55 billion pounds of copper (10B lbs. P&P) — along with updated road and power infrastructure, receding glaciers, new geological theories and good relationships between mining/ exploration companies and First Nations, these are all good reasons for building a new smelter in northwestern BC to chemically separate copper, gold, silver and other metals using Teck’s CESL Process.

We don’t have to follow the lead of the United States and become like the anti-mining Biden administration, through preventing large projects like Pebble and Resolution from being developed, and legislating royalty fee increases that discourage mining and mineral exploration.

We could choose to get ahead of the West’s insecurity of copper supply, i.e., not having enough copper to handle the oncoming crush of demand, due to electrification & decarbonization, by proactively developing our resources, and becoming a secure Western supplier. Right here in BC.

A new study by S&P Global examines the growing mismatch between available copper supply and future demand resulting from the energy transition. The study, entitled The Future of Copper: Will the Looming Supply Gap Short-circuit the Energy Transition? projects global copper demand to nearly double over the next decade, from 25 million metric tons today to about 50 million metric tons by 2035 in order to deploy the technologies critical to achieving net-zero by 2050 goals. The record-high level of demand would be sustained and continue to grow to 53 million metric tons in 2050.

Canada only has one copper smelter and one refinery, in Quebec. The richness of BC’s mineral endowment justifies at least one smelter/ hydromet complex. British Columbia has the minerals, the roads, the power and deep seaport infrastructure, the processing technology and the expertise. All we need is the political will.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

tsx

tsxv

ax

gold

silver

manganese

nickel

copper

zinc

iron

aluminum

molybdenum

bismuth

diamond

tsx-ngt

newmont-corporation

tsxv-cuu

copper-fox-metals-inc

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…

GoldTalks: Going big on ASX-listed gold stocks

Aussie investors are spoiled for choice when it comes to listed goldies, says Kyle Rodda. Here are 3 blue chips … Read More

The post GoldTalks: Going…

Gold Digger: ‘Assured growth’ – central bank buying spree set to drive gold higher in 2024

Central banks will drive the price of gold higher in 2024, believe various analysts Spot gold prices seem stable to … Read More

The post Gold Digger:…