Companies

Getchell Gold: Era of M&As may spur gold industry convergence to proven hunting grounds like Nevada – Richard Mills

2023.05.01

As a major economic driver, gold mining has traditionally been a fragmented industry due to its low barriers to entry and the advanced processing…

2023.05.01

As a major economic driver, gold mining has traditionally been a fragmented industry due to its low barriers to entry and the advanced processing techniques available to miners of any scale.

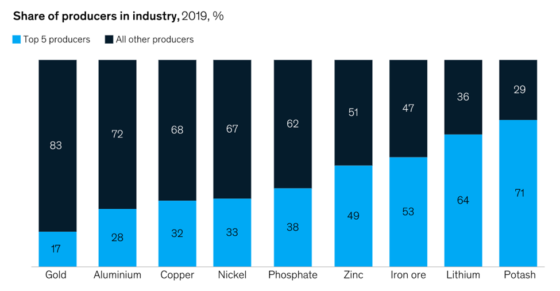

The top five gold producers contribute to less than 20 percent of the world’s total supply, according to a 2021 report by McKinsey. In contrast, for most other metals, the top five producers make up between one-third and two-thirds of global production, data compiled by the firm reveals (see below).

However, disruption to the global supply chain in recent years means that costs are fast rising in the industry. In 2022, the average all-in sustaining costs (AISC) in the mining industry reached a record high $1,276/oz, up 18% from the previous year.

Mining companies, already facing depleted gold reserves, are beginning to feel the pressure to consolidate to sustain themselves in the current economic environment, hence the growing momentum in mergers and acquisitions.

Naturally the industry will need to converge towards places where high-grade ores are abundant and gold deposits are guaranteed to be economically viable.

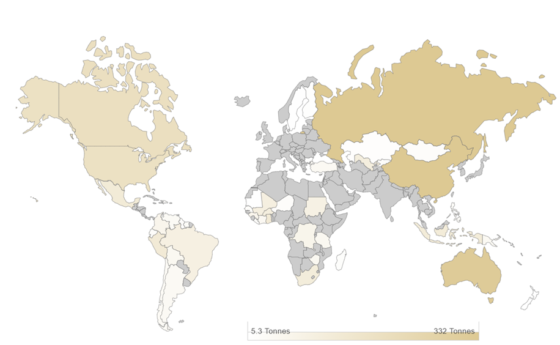

In fact, the gold sector has already become much more concentrated than before. Data from the World Gold Council shows that the “Big 5” — China, Russia, Australia, Canada and the US — combined for around 43% (1,358 million tonnes) of last year’s global mined supply (3,100Mt).

Worth noting is that North America (including the 8th-placed Mexico) is supplying about 16% of the global supply at 504 million tonnes, establishing the continent as the best place to mine gold in the Western Hemisphere.

While Canada houses several key mining hubs such as the Golden Triangle of British Columbia and the Abitibi Greenstone Belt, and Mexico is famous for its affluence of precious metals, none can match the sheer scale and productivity of Nevada, which by itself accounts for three-quarters of the US total gold production.

Today, it is consistently ranked as one of the top 5 gold-producing jurisdictions in the world.

The state is host to the largest gold mining complex on Earth: the Nevada Gold Mines joint venture between Newmont and Barrick. Formed in 2019, NGM consists of as many as 10 underground and 12 open-pit mines, plus autoclave, roasting and heap leach facilities.

Total production last year from NGM reached more than 3 million ounces, about 3% of the world’s total.

Nevada – the Golden State

To see why Nevada is so prolific in its gold production, we have to appreciate its geological profile, which is amongst the most diverse on the planet.

Nearly every type of rock known to geologists can be found in the state’s desert landscape. It contains a wealth of precious metals and is also an important source of many of the world’s most critical base metals including copper, zinc and molybdenum.

Incidentally, the state was first known for its silver following the discovery of the Comstock silver lode in 1859, hence why it’s still known by many as “The Silver State”. But as miners saw the considerable quantities of gold that came with the early silver mines, a new “gold rush” followed.

With the millions of ounces sitting underground yet to be undiscovered, it took another 100 years for Nevada to really become gold famous. Following the discovery of microscopic gold in the early 1960s, which led to Newmont establishing its operations there, Nevada officially became a “golden state”.

The Three Trends

Nevada owes its unique geology and prolific gold production to the complex tectonic history of the North American Great Basin, which gave rise to its widespread landscape of fault-dominated mountain ranges and valleys.

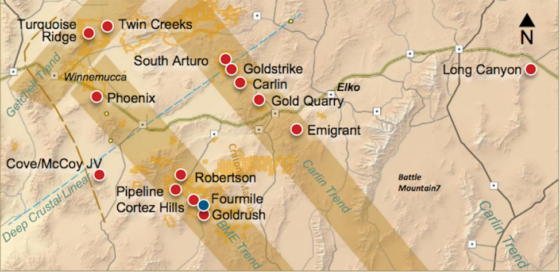

Most of Nevada’s gold deposits are now found within three northwest-trending belts. The most famous is the Carlin Trend, where sedimentary, disseminated gold appears near surface, often surrounded by smaller deposits of similar geology.

Estimated to contain up to 180 million ounces, the Carlin Trend is the second-largest gold endowment behind South Africa’s Witwatersrand Basin. The three major players operating mines in the Carlin Trend are Newmont Mining, Barrick Gold and Kinross Gold.

Barrick’s Goldstrike mine is one of the world’s most prolific. Between the Betze-Post open-pit mine and the Meikle and Rodeo underground mines, the Goldstrike mines have produced over 1.1 million ounces and have 8.1 million ounces of reserves.

Newmont’s Carlin operations have produced 944,000 ounces out of 15 million ounces in reserves. Kinross’s Bald Mountain mine, purchased from Barrick in 2016, outputted 130,144 gold-equivalent ounces, with 2.1Moz in reserves.

The other two trends, Battle Mountain-Eureka-Cortez (or just Cortez) and Walker Lane, also host some of the world’s most important gold mines, including SSR Mining’s Marigold mine in Humboldt County and McEwen Mining’s Gold Bar operation.

Together, the three major trends accounted for nearly 170 million ounces of the gold produced in Nevada between 1835 and 2018.

While Carlin-style mineralization is a common feature of these trends, Nevada also has epithermal, low-sulfidation gold deposits, which are generally smaller and are not unique to Nevada. Still, these deposits are often high grade, making them excellent targets for gold exploration companies.

Among the reasons for retaining its competitive edge are Nevada’s lack of income tax, the fact that mining is governed under the federal Mining Act of 1872, which would take an act of Congress to change, and that mining taxes are set out in the state’s Constitution.

Not only does Nevada produce a lot of gold from existing mines, it is also an excellent place to put a new mine into production. That’s because conducting exploration, constructing and building a mine in Nevada is relatively easy.

The state isn’t the country’s number one gold producer by far without good reasons. The only question is will it get even bigger?

Year of Gold M&A

In the era of depleting reserves and few new discoveries, mergers and acquisitions are typically the way to go for gold companies.

Since 2019, the year the Barrick-Newmont JV was formed, there has been a major uptick in M&As in the gold sector, both in terms of the number of transactions and the total dollar value of deals. Last year, the top 10 gold deals equated to $17.5 billion, eclipsing the record set in 2021.

The momentum in gold M&A activity continued into 2023, led by Newmont’s $16.9 billion offer to buy Australia’s Newcrest. Regardless of the outcome of this deal, the mining industry is set for a new wave of consolidation, industry executives concur.

This year is likely to see more mergers in the gold mining sector, Endeavour Mining’s chief executive Sébastien de Montessus told Reuters in an interview in February, days after news broke of Newmont’s mega-merger proposal.

“I think we will probably see more [deals], simply because some companies are lacking a clear strategy,” de Montessus said, adding that:

“You’ve got historical companies like IAMGOLD, Gold Fields, AngloGold, Kinross, where there are a lot of questions about whether their portfolio is well-suited, and whether their strategy is clear enough for investors and shareholders.”

In short, stacking up on quality assets held by others, preferably in Tier 1 jurisdictions, offers gold majors a less risky option to spend their piles of cash given the lack of growth options at their disposal.

More mergers and acquisitions in the gold mining sector are inevitable as companies will look to replace depleting assets, Harmony Gold’s CEO Peter Steenkamp said in a separate Reuters interview.

Those wanting to grow their reserves without incurring large capital expenditures are all hunting for the right assets in the right place, and where else to look for that than Nevada? The state has the pedigree and history to more than match any other in the gold mining space.

Getchell Gold

Nevada currently hosts our favorite company in the junior gold space right now: Getchell Gold (CSE:GTCH, OTCQB:GGLDF), which has an advanced-stage gold project ready to be taken to the next stage.

The company was formed about four years ago with a mandate to source out a major flagship project. After acquiring its flagship Fondaway Canyon project in 2020, Getchell first spent some time delving into the history of the operation.

To summarize, there were 40 years of small-scale mining on surface at Fondaway, and multiple drill campaigns focused mainly on the shallow oxide deposits scattered throughout the 3.5 km-long trend. While previous operators found a lot of gold, they also missed quite a bit, which captured the imagination of Getchell’s management team.

“A lot of the old companies that worked on it were just wanting to take the eyes out of it at the surface and do a hodgepodge of drilling, and so it was very surficially looked at, but what really intrigued me is that there were all kinds of little hidden jewels that indicated that the mineralizing system at Fondaway Canyon was a lot bigger than what people realized,” Getchell Gold’s President Mike Sieb said in a presentation earlier this month.

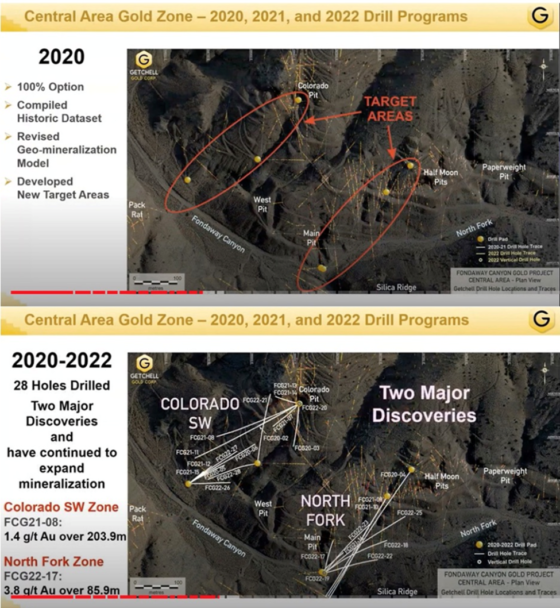

Getchell identified two priority areas to begin with, shown as ellipses on the map below. As they started to drill, Getchell kept hitting gold, and continued to hit mineralization in step-out holes. In its first year of exploration, 2020, Getchell outlined three new gold zones: Colorado SW, North Fork and Juniper.

The early wide-spaced drilling demonstrated the presence of high-grade shear veins enveloped in thick bands of mineralization and extended the mineralization model a remarkable 800 meters down dip from surface.

Five drill holes hit substantive zones of mineralization, between 50 and 100 meters thick. The company kept drilling in 2021 and 2022, upping the scale and capitalizing on its discoveries.

At the end of 2021, Getchell made a new discovery: a very high-grade zone that was running 10 grams per tonne over 25 meters near surface.

Substantive mineralization in four holes was highlighted by hole FCG21-08, the most northwestern hole, intersecting the Colorado SW zone extending for over 200 meters down hole, and hole FCG21-10, intersecting the North Fork zone extending 82 meters down hole.

The latter interval, hosting the highest-grade gold intercept in the 40+ year drilling history at Fondaway Canyon, and reporting 47 g/t Au over 1.5m, is a prime example of the structures that promote the high-grade concentration of gold at the project.

Mineral Resource Upgrade

Partway through the 2022 drill program, an open-pit model mineral resource estimate was commissioned and published (see below).

Eighteen drill holes doubled the previous resource from 2017, with 550,000 ounces of gold in the indicated category and an additional 1.5 million ounces inferred, all at comparatively excellent gold grades for active Nevada operations (1.56 g/t Au indicated, 1.23 g/t inferred).

Note, however, that this resource estimate is already out of date. There are nine holes that were excluded in the resource estimate because they missed the cut-off date, and Getchell plans to do a lot more drilling on its wide-open deposit in 2023.

Also worth noting is that Getchell hit mineralization in all 18 holes, which is almost unheard of in mineral exploration.

To date, the gold mineralization at Fondaway has been traced for a half a kilometer on surface and half a kilometer down dip. It remains open as the drilling has yet to encounter any limits, with the potential size and ultimate scale of the mineralization unknown.

“We’ve doubled the reported mineralization in a short 2.5 years and I don’t know how big this is going to get to,” Sieb told Proactive Investors earlier this month, explaining that the large footprint on surface is shallowly dipping, making for a perfect open-pit model.

He went on to say: “This is a marked difference from what it looked like it in 2020. We’ve increased not only the length of the mineralization from surface but also the thickness as well, right now we’ve modeled an extent about 550 to 600 meters down dip, the mineralization is still continuing on strong.”

Simply put, the upside potential of Fondaway Canyon is evident from the fact that Getchell just continues to find more gold.

Conclusion

In a protracted M&A cycle, gold assets with million-ounce resources like Fondaway Canyon may hold the key to unlocking the growth strategy of many major companies. The project ticks many boxes: location, history, size, you name it.

The hot gold market also presents the perfect time to advance these assets, as higher metal prices equate to higher returns and better project economics.

And with the gold industry sitting on piles of cash, there is a window of opportunity for gold explorers to keep growing their resource base and extract more value. That’s exactly what Getchell will set out to do this year, as the company will work to expand the Fondaway resource through further drilling. Preparations for a much larger drill program than before are already underway.

“We’ve been increasing the drill meterage into the ground from 2020 through 2022, and this year we’re targeting two drills turning all year long to continue to expand and increase the resources at Fondaway Canyon,” Sieb said.

The chief executive added the market can expect an updated resource estimate and the completion of Getchell’s next major milestone, a preliminary economic assessment (PEA), in the first half of 2024.

“We’re moving up the tiers of de-risking and adding confidence to the project as we go,” he added.

Given what Getchell has accomplished in such a short amount of time (i.e. a near doubling of the previous resource), there’s no reason to not get excited by what the company has in store.

Getchell Gold Corp.

CSE:GTCH, OTCQB:GGLDF

Cdn$0.26, 2023.04.28

Shares Outstanding 106m

Market cap Cdn$27.6m

GTCH website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Richard owns shares of Getchell Gold Corp. (CSE:GTCH). GTCH is a paid advertiser on his site aheadoftheherd.com

cse

otcqb

ax

gold

silver

zinc

molybdenum

cse-gtch

getchell-gold-corp

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…

GoldTalks: Going big on ASX-listed gold stocks

Aussie investors are spoiled for choice when it comes to listed goldies, says Kyle Rodda. Here are 3 blue chips … Read More

The post GoldTalks: Going…

Gold Digger: ‘Assured growth’ – central bank buying spree set to drive gold higher in 2024

Central banks will drive the price of gold higher in 2024, believe various analysts Spot gold prices seem stable to … Read More

The post Gold Digger:…