These Were The Best And Worst Performing Assets In March And Q1

These Were The Best And Worst Performing Assets In March And Q1

Q1 was a turbulent period in markets, with a surge in volatility (especially…

These Were The Best And Worst Performing Assets In March And Q1

Q1 was a turbulent period in markets, with a surge in volatility (especially in bonds, if not so much in stocks) during March after the collapse of Silicon Valley Bank. That led to fears about broader contagion across the banking system, while the sudden implosion of Credit Suisse led to its acquisition by UBS with guarantees from the Swiss government, and further bank crisis fears. As a result, as DB’s Henry Allen writes in his quarterly performance recap, “some of the daily moves were the largest seen for decades, and the MOVE index of Treasury volatility hit levels last seen at the height of the GFC in 2008.“

By the end of the quarter, the immediate volatility had subsided – in large part due to the market’s near certainty that the Fed’s rate hike cycle is effectively over – but the turmoil led to speculation about whether something was finally breaking after a rapid series of central bank rate hikes. Nevertheless, even with that market turbulence in March, Q1 as a whole saw some incredibly broad gains after the weakness of 2022, with advances for equities, credit, sovereign bonds, EM assets and crypto. The only major exception to that pattern were commodities, with oil prices losing ground in every month of Q1.

Quarter in Review – The high-level macro overview

Q1 started on a fairly positive note, with lots of good news stories in January helping markets to rebound after an awful 2022. For instance, European natural gas prices fell by -24.8% over January, which helped to allay fears about a potential recession. That was echoed among various sentiment indicators, with consumer confidence rising to its highest level in months. Meanwhile in China, the economy’s reopening continued and restrictions were eased, boosting hopes that global growth would be lifted more broadly. This brighter macro outlook meant that plenty of assets began the year very strongly. For instance, the S&P 500 (+6.3%) had its best start to a year since 2019, and Europe’s STOXX 600 (+6.8%) had its best start since 2015.

However, as we moved into February, the tone in markets became decidedly more negative. The main culprit was a series of strong US data releases and higher-than expected inflation, which led investors to ramp up the likelihood of future rate hikes. Indeed, the unemployment rate fell to a 53-year low of 3.4%. This even sparked discussion about the US economy experiencing a “no landing” scenario, where inflation stayed high and growth remained strong, requiring the Fed to take rates even higher.

This trend wasn’t just confined to the United States however. In the Euro Area, data released in February showed core inflation hitting a record high of +5.3% in January. And in Japan, headline and core CPI for January reached their highest level since 1981. This sparked a major sell-off among global bonds, with Bloomberg’s Global Aggregate Bond Index (-3.3%) seeing its worst February performance since its inception back in 1990.

By March, the persistence of inflation saw investors keep ratcheting up their expectations for central bank terminal rates. That was then validated by Fed Chair Powell, who said in his semi-annual congressional testimony that “we would be prepared to increase the pace of rate hikes”, which explicitly opened the door to 50bp moves again. Shortly afterwards on March 8, 2yr yields closed at a post-2007 high of 5.07%, and expectations of the Fed’s terminal rate stood at a new high for the cycle of 5.69%. In the meantime, the 2s10s curve closed at an inverted -109bps that day, which hadn’t been seen since 1981.

But all this changed shortly afterwards, as concern grew about the financial system after Silicon Valley Bank collapsed, raising fears about broader contagion. Credit Suisse then came under investor scrutiny and saw large deposit outflows, which culminated in a purchase by UBS that included guarantees from the Swiss government. This led to significant market turmoil, and investors speculated whether central banks might call it a day on their current hiking cycles, with yields on 2yr Treasuries seeing their largest daily decline since 1982 on March 13. Bank stocks were also hit, with the KBW Bank Index down -17.9% over Q1, despite the broader equity rally.

However, by the end of the month, there were signs that calm was returning to financial markets again. Measures of volatility like the MOVE index and the VIX index had come down substantially, and financial conditions had also eased since the height of the turmoil. And with investors far less concerned about aggressive rate hikes, sovereign bonds put in a very strong performance. In fact, for US Treasuries it was their best monthly performance in 3 years since March 2020, back when investors poured into save havens and the Fed slashed rates and restarted QE.

The big question now, the DB strategist concludes, is whether the turmoil from March proves to be an isolated incident, or whether it proves the harbinger of further shocks ahead.

Which assets saw the biggest gains in Q1?

- Equities: Despite the market turmoil, equities overall saw solid gains over Q1. For instance, the S&P 500 (+7.5%), the STOXX 600 (+8.6%) and the Nikkei (+8.5%) all advanced on a total return basis. Tech stocks were one of the best performers on a sectoral basis, and the NASDAQ (+17.0%) had its best quarter since the Q2 2020. However, given the financial turmoil, banks were one of the weaker performers, and the KBW Bank Index fell -17.9% over Q1.

- Credit: There was a decent start to the year in credit, with gains across all indices in USD, EUR and GBP credit. The strongest gains were seen among GBP IG non-fin (+4.3%) and US HY (+4.2%), whereas the weakest was among EUR Fin Sub (+1.1%).

- Sovereign Bonds: US Treasuries (+3.3%) just experienced their best quarter since the pandemic turmoil of Q1 2020, back when investors poured into save havens and the Fed slashed rates to zero and restarted QE. For Euro sovereign bonds (+2.4%) it was also their best quarter since Q3 2019, and brings an end to a run of 5 consecutive quarterly declines.

- EM Assets: Having struggled in 2022, emerging markets saw a much better start to 2023 across the major asset classes. For instance, the MSCI EM Equity Index was up +4.0%, EM Bonds were up +4.9%, whilst EM FX was up +2.0%.

- Precious Metals: Gold (+8.0%) and silver (+0.6%) prices both advanced over Q1. Prices have been supported by growing demand for safe havens, along with the prospect that central banks might be ending their hiking cycles shortly. That came after some very strong performances in March specifically, with gold up +7.8% over the month and silver up +15.2%.

- Crypto: After significant losses in 2022, crypto-assets rebounded in Q1. Bitcoin had its best quarterly performance in two years, with a +71.7% advance that left it at $28,395. And this was echoed among other cryptocurrencies too, with Ethereum (+51.6%) also seeing a sharp rebound, whilst Bloomberg’s Galaxy Crypto Index was up +59.7%.

Which assets saw the biggest losses in Q1?

- Commodities (except precious metals): Commodities were the only major asset class to lose ground over Q1. For instance, Brent crude oil prices were down -7.1%, marking a third consecutive quarterly decline for the first time since 2014-15. In Europe, natural gas futures were down -37.3% over Q1, building on their -59.6% decline in Q4 last year. And plenty of agricultural commodities also fell back, including wheat (-12.6%), corn (-2.7%) and soybeans (-0.9%).

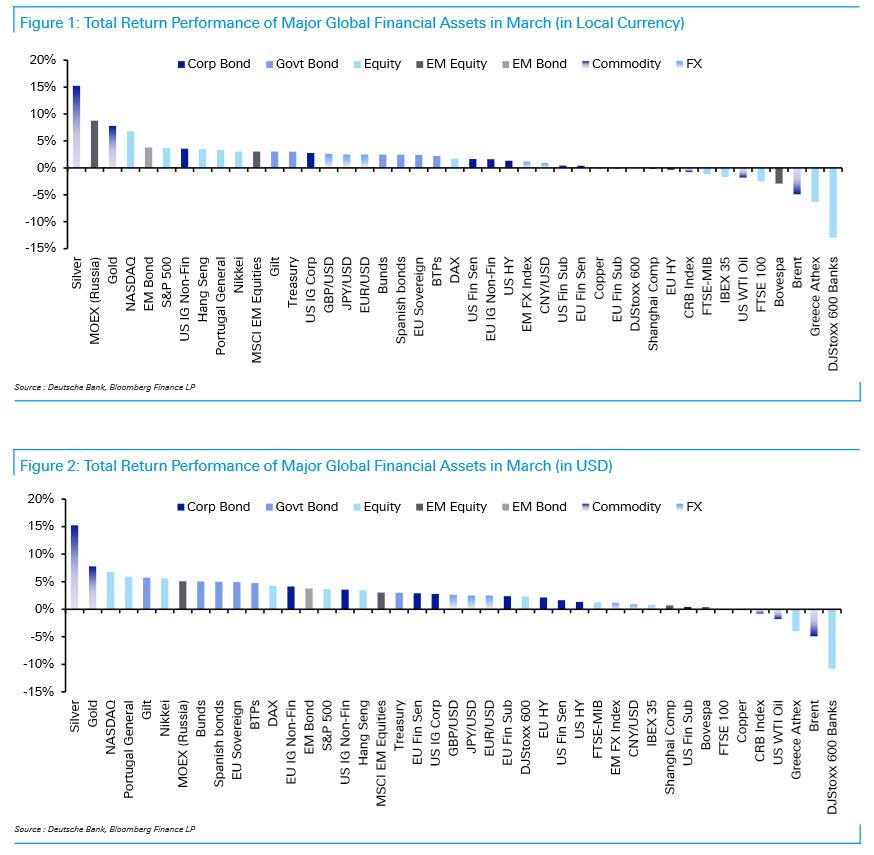

Finally, here is the visual summary of best and worst performers in March…

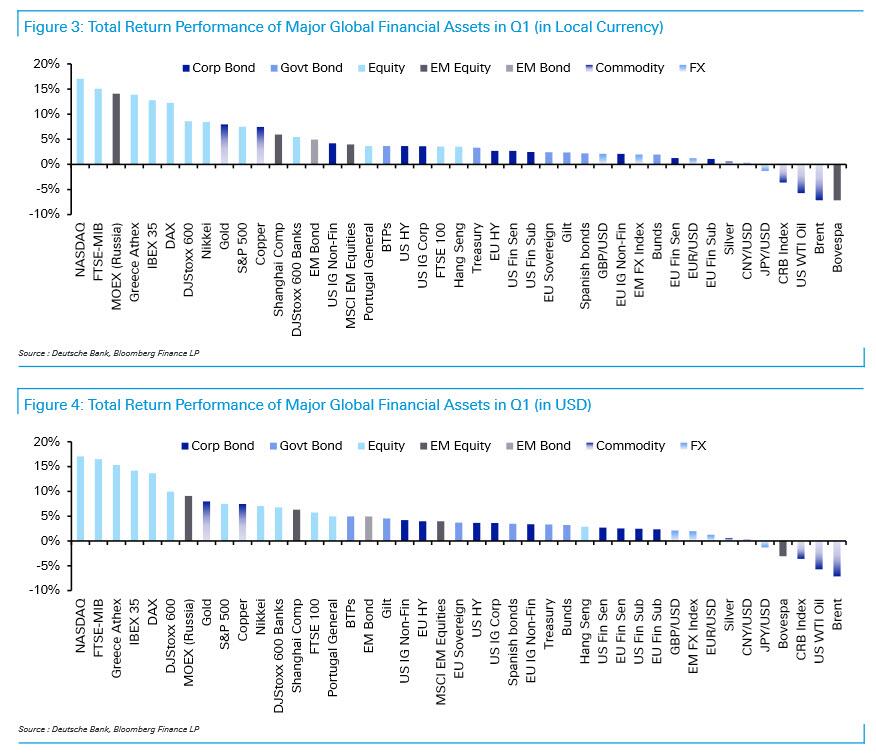

… and March.

Tyler Durden

Mon, 04/03/2023 – 15:30

nasdaq

gold

silver

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.