Uncategorized

New tech-led solar energy boom to fuel silver mining M&A ‘frenzy’

KITCO’s Ernest Hoffman was in conversation with Peter Krauth, editor of SilverStockInvestor and author of The Great Silver Bull, during which he made…

KITCO’s Ernest Hoffman was in conversation with Peter Krauth, editor of SilverStockInvestor and author of The Great Silver Bull, during which he made the case for an interesting new dynamic emerging in silver investing.

As a side note, in my opinion, gold and silver’s sustained historical role as money cannot be ignored.

The world’s reserve currency, the dollar, only came off the silver standard and gold standard in 1964 and 1971, respectively.

As a result, other than their mainstream investment characteristics, these metals have always held a special place in the economics of money and the portfolios of a certain type of investor.

However, by being priced considerably higher than silver, gold usually gets significantly more attention, is available more abundantly, and belongs to a much larger paper market.

To get a sense of the differences between physical and paper markets, interested readers can take a look at this article.

Silver is often thought of as a much more volatile and speculative investment, which could potentially lead to higher returns.

Indeed, that is what history shows.

During the precious metals bull run of the 1970s, Krauth notes that gold prices increased dramatically by 1400%, while silver surged 3700% higher.

With several economists expecting a commodity bull market to materialize in the future, history would suggest that silver returns could play an invaluable role in gold investors’ portfolios.

Interested readers can check out my earlier piece on Invezz about Zoltan Pozsar’s and George Gammon’s contrasting views on the coming commodity bull run.

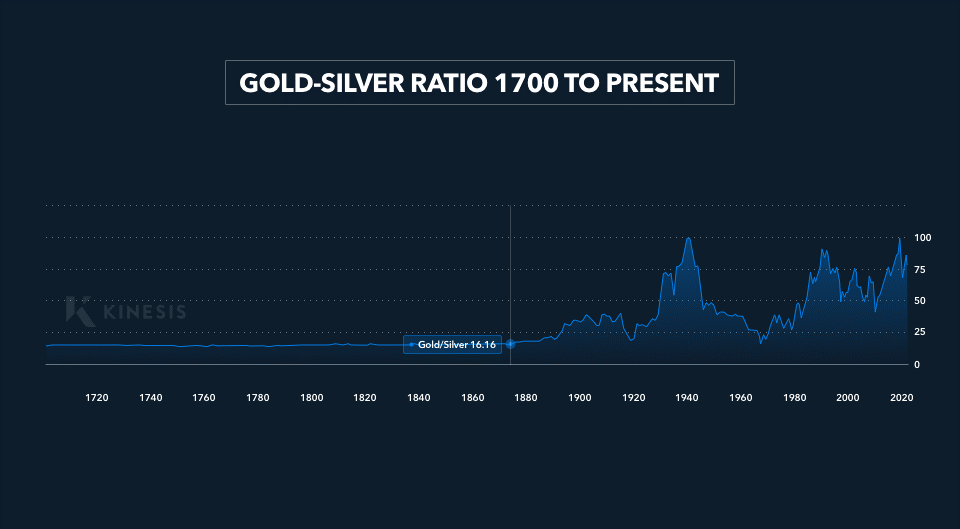

Krauth adds that the Gold-Silver ratio is currently trading in the 80s, well above its twenty-year average of 55 to 60, and many multiples above its 1980 bottom.

As a result, silver should ideally display incredible upside while merely reverting to its recent averages, let alone the multi-year lows.

Crucially, Krauth points out that silver is unique in that it has not yet outdone its 1980s top of $49.45, unlike gold, palladium, platinum and even the common base metals.

At the time of writing, silver is trading 53.6% lower than its all-time high, suggesting the potential for a lot of upside.

Demand-Supply dynamics

As per the Silver Institute, demand for the metal skyrocketed to a new high of 1.24 billion oz in 2022.

The bulk of the added demand was in the silverware and jewellery segments, rising 80% and 29%, respectively, principally driven by Indian customers.

Investment demand was a significant component, rising more than a fifth and reaching well-above 300mn oz. last year.

Another potential source of emerging demand is directly from governments, including US states.

I covered this dynamic in an earlier piece entitled, “Gold and silver outlook as 23 states move to reclaim precious metals as legal tender.”

For instance, it is estimated that the state of Missouri would alone need to purchase $9 million worth of bullion (gold or silver) to meet the regulations suggested in a draft bill.

Stalled supplies

Despite the pull of higher demand, supply was nearly stagnant, rising 1% over 2021, dragged lower by falling mine production, particularly in China and Peru.

The rise came through recycling activity which increased by 3%, reaching a 10-year high of 180.6 million oz.

This situation is not expected to improve with the Silver Institute projecting 2023 to yield the second largest deficit on record at 142.1 million oz.

This mismatch is primarily driven by the subdued market price of silver, as well as the difficulty in the identification of geologically sound areas that could produce economically viable deposits.

Further, a new mine could take well over a decade till the first silver makes it above ground.

Secondary silver operations

Moreover, pure-play silver mines are a rarity in the industry.

At least 70% of silver is derived as a by-product from gold, lead, zinc, and copper mines.

Thus, any risks from financing, licensing, environmental permits, geopolitical factors, and falling market demand to these sectors or individual operations are automatically transferred to silver volumes.

Given that silver supply is so inelastic, and can not be improved in a hurry even at higher prices, any significant additional supply is likely to come from consumers redeeming silver products for cash, and major investors draining exchanges of their physical inventories.

A piece on the drawdowns in physical silver from major exchanges in 2022 is available here.

Solar demand

The crux of Krauth’s argument comes from the expectation that the solar sector is poised for an unstoppable surge.

At present, solar demand makes up about 12% of market demand at 140mn oz.

He notes,

…forecasts are to about 160 million ounces this year which I believe are going to be dramatically outpaced…

This is because of the confluence of multiple factors that are bullish for solar.

Firstly, governments around the world, at a variety of levels, are pushing solar-led electricity generation policies.

As per the International Energy Agency, these efforts have received a major boost with solar now becoming the cheapest form of electricity in many jurisdictions.

Further, generous incentives and tax credits are being rolled out to support more installations and mould the solar sector into an attractive long-term investment opportunity.

New technology

The development of TOPcon and HJT solar cells is paving a new path for electricity generation and silver consumption.

TOPcon technology refers to ‘Tunnel Oxide Passivated Contact’ solar cells, while HJT is ‘Heterojunction’.

Krauth noted that available studies suggest that these technologies, being more efficient than traditional Passivated Emitter and Rear Cell (PERC) technology, shall soon make up 80% of the new capacity brought online.

He added,

TOPcon uses 50% more silver per panel (while) HJT uses up to 150% more silver per panel.

The argument that solar-led silver demand will explode in the near to medium term was supported by a recent study by Bloomberg New Energy Finance which noted,

…expects (China) to add nearly three times the capacity it did just two years ago or more than the entire total in the US.

The Internal Energy Agency has also projected that there needs to be a 25% annual growth in solar generation till 2030 to meet the net zero emissions goal by 2050.

Thus, if the policy push stays in place, both solar and silver have tremendous room for development.

As per Krauth, the silver demand from TOPcon and HJT has not been absorbed into these forecasts, and thus, he believes that investors are currently underestimating the full-year solar-silver demand for 2023, which is likely to be between 180-200 million oz.

Mining M&A

Krauth expects that with the supply-demand balance only expected to deteriorate further, the silver price will have to head higher.

With the inelasticity in silver output, higher prices may stay higher for longer, driving a valuations boom for leading silver miners.

As a result, these players would become cash-rich and look to expand their operations through acquiring new silver assets, particularly smaller mining operations that have so far been overlooked due to the low market incentives.

This scenario is supported by studies showing a significantly wider distribution in global silver production, meaning that more operations have come online over the past two decades.

With larger players looking to increase their footprint through M&As (given the challenges of identifying rich, untouched deposits), operations across the board could see higher valuations purely due to market forces, independent of any new geological surveys, technological improvements, and additional discoveries.

In addition, as the net-zero thesis has become mainstream, miners that specialize in gold, copper and other metals are interested in the economics of silver, and may become key players in driving the long-term potential of an M&A ‘frenzy.’

Potential risks

Risks to Krauth’s thesis could emerge from a hard landing and the concerns of some economists that we may be looking at a depression-style slowdown as interest rates continue to head higher.

If such an event were to occur, electricity demand and global emissions would both fall, potentially dampening policy momentum and perhaps taking some off the sheen of solar.

Further, silver demand is highly correlated with economic growth given its many industrial uses.

Secondly, China is a key component of the coming solar decade argument.

With falling PMIs, a weaker consumer at home, the possibility of a downward revision in GDP and policy uncertainty going ahead, the country may not be able to deliver in line with these impressive projections.

A recent piece on the Caixin PMIs for China is available here.

Although geopolitical factors have spurred the expansion of solar power in many countries, renewed potential disruptions in the global supply chain, and commodity and semiconductor protectionism may dampen installation activity.

In the future, analysts would also need to identify the likelihood of reaching a silver price at which the competitiveness of solar installations may be sufficiently dented.

The post New tech-led solar energy boom to fuel silver mining M&A ‘frenzy’ appeared first on Invezz.