Precious Metals

Silver price outlook mixed even as Comex drained and global GDP diverges

Something rather peculiar has been happening at the Comex. The exchange which has traditionally been dominated by unallocated trades has been seeing a…

Something rather peculiar has been happening at the Comex.

The exchange which has traditionally been dominated by unallocated trades has been seeing a thick outflow of physical precious metals from its vaults.

Unallocated gold and silver is another way of saying that there are no physical precious metals held in your name.

Instead, the customer takes an interest in a contract which represents metal that they can never physically withdraw.

These are essentially derivatives that are meant to track the underlying price of the commodity, and the issuing entity may not have the requisite metal in custody.

This is because when traders take a position in these contracts, they execute a profit-taking strategy or use this for short-covering purposes without any physical metal exchanging hands.

Interested readers can read more about the underlying dichotomy in this piece.

Comex silver drained

However, investor attitudes towards physical metals appear to be rapidly shifting away from this paper-based system.

A report shows that in the year leading up to March 17th, exchange participants have taken delivery of 17.3% of the physical silver available at the Comex instead of maintaining them as tradable contracts.

This is an extraordinary reversal which becomes clear from a memorandum signed between the London Bullion Markets Association (LBMA) and the London Platinum and Palladium Market (LPPM) in 2013,

Investors acquire an interest in the metals, although in most situations, physical delivery will not occur and in 95% of trades, trading in unallocated metals will be

undertaken…95% of transactions are in unallocated metal: therefore, because they are treated as services, the location of the underlying metal is

not relevant…However, in the case of unallocated metal (about 95% of the total) there is no actual charge for storage as the metal belongs to the bank.

This becomes even more exceptional when one considers margins.

For traders wanting to take an interest in a block of 1000 contracts, they would only be required to put up a proportion, say 10-15% of the total value of the metal to begin transacting.

By making such massive withdrawals, the markets are essentially arguing that physical silver is the more durable source of wealth compared to paper contracts, and they are willing to make payments of approximately 7 to 10 times the value to secure the real thing.

This is in line with central bank demand for precious metals which has been surging for well over a year.

Given this activity, popular substack GoldFix expects that,

A massive price tornado is brewing for precious metals.

Physical imbalances play second fiddle

Silver buying surged last year with the Silver Institute’s World Silver Survey 2023 estimating a 22% rise in physical investment purchases and a 5% increase in industrial application demand.

All major categories were propelled to record highs in 2022, resulting in aggregate buying of 1.242 billion ounces, nearly two-fifths above 2020 levels.

Applications included photovoltaics and electrification segments, automakers, 5G network technology and the construction industry.

Jewellery and silverware demand was spurred on by the Indian market following lower prices, improved employment, the release of pent-up demand and diversification away from financial holdings.

Yet, Comex prices remained largely range-bound, at least until Q4 2022 when markets were debating if a Fed pause was on the cards, before sharply moderating in Q1 2023.

This is due to the sheer scale of the paper-derivatives market which follows big investor demand for financial securities and dwarfs the prevailing physical fundamentals.

Unlike retail demand which found a driver in persistent inflation, high rates kept institutional demand at bay leading to a largely bearish view on the Comex.

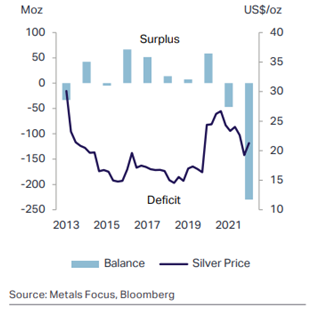

Supply gap and structural deficits

Despite the rising demand for the precious metal, supply contracted last year, falling by 5.2 million ounces worldwide, pushing silver into a second consecutive year of deficits.

Mine production struggled, owing to lower by-products yields among lead and zinc mines in China, while Peruvian output plummeted due to falling metal grades, work suspensions and social disruptions, which contributed significantly to the record shortfall of 237.7 million ounces in the market.

According to the Silver Institute, combining the heavy deficits of 2021 and 2022,

…more than offset the cumulative surpluses of the previous 11 years.

Although the Institute expects this imbalance to narrow to 142.1 million ounces in 2023, this would still equate to half of the global mining output.

However, the effects of the physical divergence on price are unlikely to contribute meaningfully to bullish sentiments in the near term, except possibly through additional physical buying.

Citi’s read

Over the past few weeks, silver spot prices have begun to respond by showing some upside momentum, likely following expectations of a weaker dollar and the possibility of the Fed ceasing its rate hikes.

Maximillian J. Layton, Managing Director, Head of EMEA Commodities Research at Citi, is bullish on silver, resulting in an upward revision to the bank’s three-month forecasts by $4 to $28, and the six-month forecast by $2 to $30.

His core thesis draws on the divergence in economic growth in advanced countries versus emerging markets.

The IMF expects advanced economies to see a ‘pronounced growth slowdown’ to 1.3% in 2023 while emerging economies are forecast to grow at 3.9%.

The following year, this gap is expected to widen to 1.4% and 4.2%, respectively.

The Citi team identified such growth dynamics to be in line with previous silver bull markets in 2007-08, 2010-2011 and the summer of 2020.

For instance, starting from August 2010, prices surged by $30 per ounce within six months, while in 2020 they increased by $10 per ounce within a few weeks.

Again, such sharp increases are in part due to the small size of the international silver market which is prone to high volatility but can also see much sharper breakouts.

Higher growth in the EMs may suggest higher industrial demand as well as enforcing already strong retail demand, while weaker growth in developed markets may prompt more precious metal demand from institutions, especially at lower interest rates.

Dollar weakness

The team at Citi expects the greenback to continue to weaken against other currencies, with the DXY down nearly 2% YTD.

The strength of the dollar is directly correlated with higher interest rates due to capital inflows as international investors search for better returns in global reserve currency-denominated assets.

However, May 3rd could mark the final rate hike for the Federal Reserve as financial conditions tighten, the debt ceiling looms large, stresses in the regional banking sector re-emerge, business sentiment continues to deteriorate and the housing sector shows signs of weakening.

Interested readers can find out more about the outlook for key central banks in this article.

A lower dollar would support the international silver price which is priced in the currency.

Another important aspect to consider is the rise in national commitments pushing the de-dollarization narrative which if successful could substantially weaken dollar demand.

The latest developments in this regard are available in this article.

How successfully and how quickly such initiatives can emerge as truly viable monetary alternatives is yet to be seen.

However, the confidence of central banks in making precious metals purchases instead of self-insurance via foreign exchange is a signal that this highly sophisticated class of market player is preferring to at the very least, hedge against the possible decline of the dollar.

ETF demand

Citi analysts also noted,

ETF buying seems strongly negatively correlated with U.S. real interest rates… (demand for precious metals could) move higher during 2023.

Since precious metals do not generate a regular flow of income, they tend to compete poorly against interest-bearing assets.

As real interest rates rise, they tend to become less favoured.

If the Feds Funds Rate begins to decline, possibly later this year, silver ETF demand could grow significantly with Citi noting that earlier bull markets saw demand for futures products rise 2 to 4 times the current levels.

Mixed views and physical opportunity

The Citi group expects that silver could see a greater than 10% upside, and even rise as high as $34 per ounce in a six-to-twelve-month window.

The risk to this outlook would materialize if the Fed manages to continue to hike rates despite financial fragilities, which would likely harm both institutional and industrial demand.

On the contrary, if interest rates continue to remain elevated amid high inflation, both institutional and industrial demand could take a hit.

Accordingly, analysts from the Silver Institute have a much more muted view and factor in the price falling as low as $18 before year-end.

The sharp split in the view is a demonstration of the sway the Fed still holds over nearly every financialized market.

At this juncture, the derivatives market is still responsible for price-setting, despite the supply-demand picture.

Yet, the vast withdrawals of physical metal from paper exchanges could pave the way for a silver price which is more dependent on the physical picture.

For investors who are interested in exploring the security of the physical markets as opposed to paper products, higher-for-longer rates may prove to be a buying opportunity.

The post Silver price outlook mixed even as Comex drained and global GDP diverges appeared first on Invezz.

dollar

gold

silver

inflation

derivatives

commodities

commodity

monetary

markets

reserve

metals

mining

interest rates

fed

central bank

reserve currency

palladium

precious metals

Canadian Silver Co. Will See Big Changes in 2024

Source: Michael Ballanger 12/22/2023

Michael Ballanger of GGM Advisory Inc. takes a look at the current state of the market and shares on stock…

EGR options out Urban Berry project in Quebec to Harvest Gold – Richard Mills

2023.12.23

EGR Exploration Ltd. (TSXV: EGR) has moved from owner to shareholder at its Urban Berry project in Quebec, this week announcing it is optioning…

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…