Precious Metals

Mispricings Everywhere as We Enter Stagflation-Lite

Mispricings Everywhere as We Enter Stagflation-Lite

Authored by Simon White, Bloomberg macro strategist,

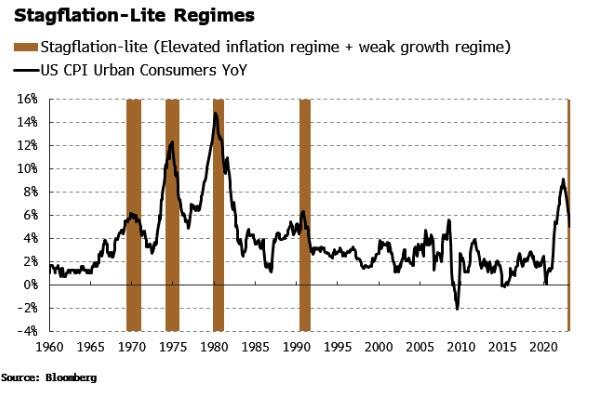

The US is now in “stagflation-lite”…

Mispricings Everywhere as We Enter Stagflation-Lite

Authored by Simon White, Bloomberg macro strategist,

The US is now in “stagflation-lite” as faltering growth has joined heightened and persistent inflation, leaving many assets materially mispriced and liable to sizable corrections.

The US is already in, or will likely soon be in, a recession. But even on the slim chance one is avoided, the economy is already undergoing a transition to “stagflation-lite”: the combination of an elevated inflation regime with a structural fall in growth.

Full stagflation is when unemployment also begins rising. That will happen, but the investment outlook is changing now, meaning portfolios should be reflective of this new reality today.

Previous instances of stagflation-lite show asset returns are often very different to those delivered so far this year. That means there are many assets that are likely significantly underpricing or overpricing the economic environment, including oil companies, commodities and financials (too cheap); and gold, tech and auto companies (too rich).

Further, equities are performing better than might typically be expected versus previous stagflation-lite regimes, while bonds are more in line.

To show this, we need to first define stagflation-lite regimes using the following criteria:

-

The one-year moving average of year-on-year headline CPI > the two-year average;

-

One-year moving average of headline CPI is > 4.5%;

-

Inflation volatility is above trend on a persistent basis; and

-

The one-year moving average of year-on-year real GDP is less than the 10-year average

This yields four distinct historical periods:

-

1969–1971: a period when the Federal Reserve was over-easing in a mistaken belief the economy was further away from the unemployment rate that leads to accelerating inflation

-

1974-1975: the tail-end of the 1973-1975 recession and heightened inflation after the Arab oil embargo

-

1979-1981: the second big oil shock of the 1970s after the Iranian Revolution in 1979 and a recession induced by Volcker’s rate rises; and

-

1990-1991: an inflation aftershock at the start of Greenspan’s tenure at the Fed and the 1990 recession

Based on the above definition, the US entered stagflation-lite at the beginning of this year:

There’s a saying in the military that amateurs talk strategy, professionals talk logistics. It’s fair and well to define and label regimes, but what are the practical takeaways?

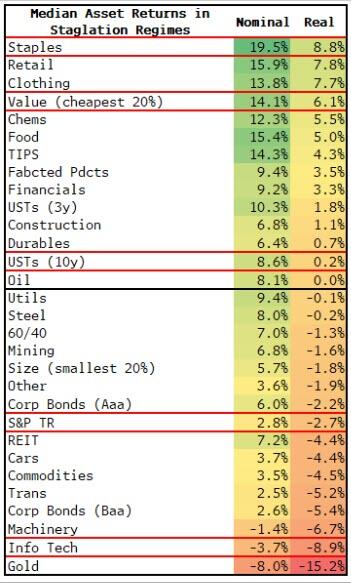

I took a whole range of asset classes, stock sectors and factors and looked at their median performance through the four historical stagflation-lite regimes, shown in the table below

There are some surprising results. The most eye-popping is gold. It has performed worst in previous stagflation-lite regimes, with a median real annualized return of -15.2%. This is at odds with how it has been performing of late, up over 30% this year on an annualized basis. (The poor performance of gold is not skewed by the drop after the near-vertical rally at the beginning of 1980. Taking this period out would still leave gold at the bottom of the list).

But on reflection it makes more sense when you remember gold often underperforms when the economy is in trouble as it is a liquid asset investors can jettison quickly to pay margin elsewhere.

Gold, however, performed well throughout the 1970s. This is a reminder that gold is not a trade, but a form of insurance owned, and added to, over the very long term.

More expected is tech, at second from bottom. Tech stocks tend to be higher-duration (although the the type of companies in the tech sector of the 1970s look very different to those of today), and are therefore more exposed to higher inflation through higher rates.

The performance of value and staples, near the top, also looks intuitive, as does machinery’s placement near the bottom, given high fixed costs are a major disadvantage when inflation is elevated.

But tech has performed very well this year, way ahead of where you might expect given the economic backdrop, while staples are lagging and underperforming the index.

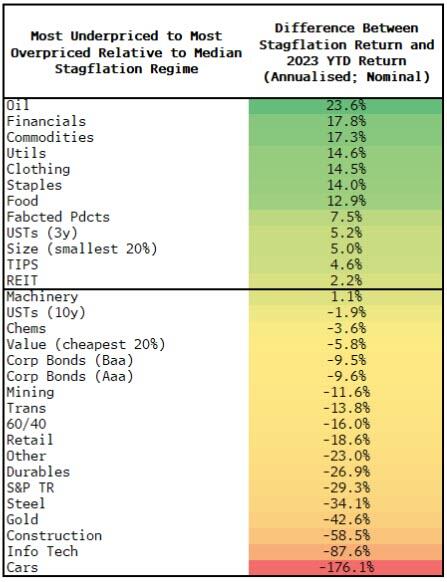

In fact, we can reorder the table to show the most underpriced to the most overpriced assets based on their median stagflation-lite return and their 2023 year-to-date return:

The most underpriced are oil companies and commodities. Oil companies peaked out last year and have been in a range since, but they are in good position to begin rising again due to continued underinvestment in especially downstream products, a rising oil price supported by production cuts, and greater investor need for inflation hedges.

At other end of the scale are automakers. These have been on a tear this year, in stark contrast to their typical weak performance in stagflation regimes. Again this is intuitive given the inflation challenges to businesses with high fixed costs and low pricing power dependent on the consumer.

The table above should not be taken as a ready-reckoner for which assets will rally or fall. Nonetheless, portfolios straying too wildly from the asset mix implied by it may not be best placed to weather the new and emerging economic reality.

Tyler Durden

Thu, 04/20/2023 – 08:05

gold

inflation

stagflation

commodities

reserve

fed

Canadian Silver Co. Will See Big Changes in 2024

Source: Michael Ballanger 12/22/2023

Michael Ballanger of GGM Advisory Inc. takes a look at the current state of the market and shares on stock…

EGR options out Urban Berry project in Quebec to Harvest Gold – Richard Mills

2023.12.23

EGR Exploration Ltd. (TSXV: EGR) has moved from owner to shareholder at its Urban Berry project in Quebec, this week announcing it is optioning…

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…