Articles

Portofino Resources; Cheapest Lithium Portfolio in Argentina

Portofino Resources holds some valuable properties in Argentina & Canada, secured at very low cost by option agreements…

In writing about Portofino Resources (TSX-v: POR) / (OTCQB: PFFOF) over the years, there have been ups, downs & delays, but at the end of the day the Company holds some valuable properties in Argentina & Canada, secured at very low cost by option agreements. Management just raised $735k, giving it an enterprise value {market cap + debt – cash} = $7M.

Portofino controls a meaningful Li portfolio in Salta province, Argentina

This update will focus entirely on Portofino’s Argentina lithium brine prospects. Last year management signed a MOU to substantially increase its lithium (“Li“) footprint in Salta province. That agreement currently covers five land parcels. This, in addition to the Company’s option to acquire 100% of the Yergo project in Catamarca province.

Portofino is partnering with state-owned REMSa. S.A. Management executed a collaboration agreement to form a JV or other arrangement with REMSa that enables it to earn majority interests (assume ~70%) in the five claims blocks. The map above shows the Salta prospects & Yergo project at the bottom.

The timing & amount of exploration to be financed by Portofino is entirely in management’s hands. REMSa has a clearly stated goal of facilitating the development of mining projects in Salta province. To that end, it works with local communities, mining companies & agencies, politicians, service providers, etc.

The Salta properties enjoy strong potential as both stand alone & satellite deposits as they are in the same province as producers Livent & Allkem. Ganfeng’s & Lithium Americas’ [LAC] world-class Cauchari-Olaroz project (in Jujuy, but near Salta) is slated to enter production within months.

Salta also hosts LAC’s Pastos Grandes project, Galan Lithium’s Hombre Muerto West & Candelas projects, and Allkem’s advanced-stage Sal de Vida project, (in Catamarca, but near Salta).

“Portofino & state-owned mining company of the province of Salta (REMSa) continue to work within the framework of the previously executed MOU and have filed a JV proposal pursuant to the provincial mining law regarding an 8,445-ha property in the Arizaro salar in close proximity to world-class projects operated by Ganfeng, Rio Tinto & Eramet.“

above from recent press release

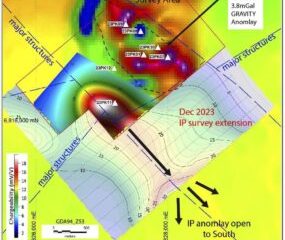

Geologists have been on the ground at both the Arizaro & Hombre Muerto prospects. Surface sampling, trenching and a geophysical survey has been undertaken at Arizaro. Results are expected in March or April. Portofino has spent $100’s of thousands and will spend up to $1M on the initial evaluation of Arizaro alone.

Yergo project could be worth $10’s of millions

Regarding Yergo, a drill permit has been in process for well over a year. Five months ago the claim-owner launched an effort to wiggle out from under the option transaction signed in 2019. The Company’s in-country team & lawyers are confident the law is firmly on their side, but this remains a risk factor.

Management notes that the provincial court examined a substantial amount of evidence provided by Portofino and agreed to grant an injunction stopping the vendor from acting outside the terms of the agreement.

There have been two sampling programs + a geophysical survey done on Yergo. Surface & near-surface samples averaged 278 ppm, and up to 373 ppm Li.

As disappointing as delays are, readers are reminded of what has happened in Argentina, and in Li generally, since 2021.

The Li price (in US$) soared from a low in the mid- $5,000’s/tonne to nearly $85,000/t (China spot price battery-quality Li carbonate). Since November the price has retreated to ~$55,000/t (investing.com).

However, to put that figure in perspective, it remains 3x higher than that used in any PEA or Feasibility study done before mid-2022.

Another important development is the rise of Direct Lithium Extraction (“DLE“). DLE proposes to make 200 ppm Li brine deposits viable. PFS-stage Lake Resources has a ~$650M valuation on its 5.3M tonne LCE Kachi project grading 202 ppm Li. Pre-PEA junior Alpha Lithium ($135M valuation) has a 3.3M tonne resource grading 270 ppm Li.

Li prices have soared (though down recently), DLE is coming, watch for more blockbuster M&A

Since 2021 Rio Tinto, Ganfeng & Zijin Mining made acquisitions of Argentinian brine projects with price tags ranging from US$735 to $962M, LAC acquired two projects for > US$600M, and Tsingshan invested US$375M for 50% of Eramet’s brine project.

POSCO plans to spend US$4B on a project to initially produce 25k tonnes LCE. In addition to potential expansions by those companies, others are presumably looking for footholds, perhaps SQM or Tianqi.

Over a dozen Chinese companies are actively investing in Li; players like; Suzhou TA&A Ultra Clean Technology, Sichuan Yahua Industrial Group, Zangge Mining Company & Sunresin New Materials — names valued in the US$ billions to US$10’s of billions.

Also searching for Li assets are auto / battery makers & commodity traders like Glencore, Mitsui & Co., Traxys, Hanwa Co., Ltd. & Trafigura.

The chart above shows what Portofino’s properties could be worth as they become better known. To be conservative, one could take out the two highest valuations, making the average $1,271/ha.

At that indicative level, the Company’s 14,596 hectares [100% option on Yergo + five (70%) options on Salta prospects] would be worth $1,271 x 14,596 = $18.5M.

Argentina; the world’s proving ground for DLE/brine projects

Drilling will provide a better sense of indicative values, but Portofino has two main Salta plays (of 5 total — each with options to earn majority interests) + an option on 100% of Yergo in Catamarca. Yet the market is valuing the entire portfolio at just $3.5M (50% of the Company’s enterprise value)

NOTE: These properties at 2,932 to 8,445 ha might seem small, but Lithium South Development has booked 571k tonnes LCE at 756 ppm Li on a 383 ha portion of its 5,687 ha project.

Four companies paid > US$600M each to enter into, or expand, in Argentina. Two of the four were not Li, auto or battery makers! I see no reason why $10’s of millions couldn’t be offered for Portofino’s interests in Salta upon initial drilling success. And, Yergo could also be a game-changer.

Peer [pre-PEA] tonnes in Salta/Catamarca are valued at $41 to $185/t. Lithium Chile’s [2.6M tonne LCE, 23,300 ha project] is eight km from Portofino’s [option to acquire 70% of] Arizaro prospect (5,912 net ha). Lithium Chile’s project has a Measured + Indicated + Inferred grade of ~300 ppm Li.

That project’s value is roughly $41/tonne LCE or ~$4,500/ha. If Portofino/REMSa’s Arizaro project is worth a quarter of Lithium Chile’s asset (based on relative # of hectares) it would be valued at $26M.

Could Yergo host over a million tonnes LCE? Yes! One million pre-PEA tonnes would arguably be worth $40M. Yergo is 15 km from Zijin’s BFS/DFS stage, very high-grade (921 ppm Li) / low impurity 3Q project acquired for ~US$735M.

Yergo covers an entire Salar, making it attractive to DLE technolgy players like Lilac Solutions, who agreed to invest US$50M in Lake Resources, or Koch Industries, Sunresin & POSCO.

Conclusion

Portofino Resources’ (TSX-v: POR) / (OTCQB: PFFOF) Argentinian portfolio spanning Salta & Catamarca provinces is early-stage, but any one of the prospects could be a company-maker. M&A activity has been intense with five major deals totaling > US$3 billion in the past few years. I believe M&A in the next few years could be equally spectacular.

Readers are reminded that when most of those blockbuster transactions were announced, Li prices were well below today’s level of US$55,000/t.

While investors don’t know if Portofino is sitting on any sizable Li deposits in Salta/Catamarca, or what the grades might be, one can’t rule out 400 ppm+ Li and/or (spanning several projects) multi-million tonnes of LCE.

If a grade of 200 ppm Li is proven viable at commercial scale, which I believe it will, there’s a good chance Portofino can clear that bar! Billions of dollars are flowing into Argentina’s brine projects.

All Portofino needs is one or two (among many dozens) much larger companies to partner on some or all of its exciting opportunities.

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Portofino Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Portofino Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Portofino Resources is an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

NOA Lithium Brines Might Be Better Named WHOA! Lithium Discoveries

The company’s recent drilling results at the Rio Grande project have been nothing short of groundbreaking…

Lithium Rush in Ontario: Westmount Minerals and the Georgia Lake Kaba Property

Amidst the Ontario lithium rush, Westmount Minerals is making strides with its Kaba Lithium property…