Economics

Luke Lango Just Sold an AI Darling

The rise and fall of Sun Microsystems … Nvidia’s absurd valuation … some popular AI stocks are looking wobbly … a powerful tool to improve your…

The rise and fall of Sun Microsystems … Nvidia’s absurd valuation … some popular AI stocks are looking wobbly … a powerful tool to improve your investing

We begin today’s Digest with a story we first told back in the spring…

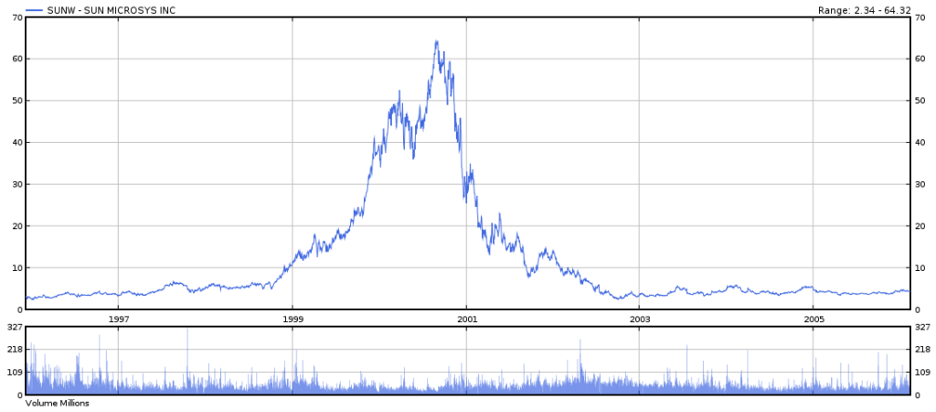

Older investors will remember Sun Microsystems. It was a tech stock darling that created overnight riches for investors in the late 1990s.

From 1996 through its high in 2000, the stock rose from about $5 to $64 for gains of well-over 1,000%.

Of course, when the dot com bubble burst, so too did Sun Microsystem’s stock.

By 2006, Sun had round-tripped, falling back to $5, losing all its gains.

Investors who bought Sun late in its run-up in the late 90s and held onto their stock found themselves sitting on staggering losses they never recouped.

Now, there’s nothing inherently noteworthy about this story. You’ve heard these “rags-to-riches-to-rags” tales plenty of times.

What makes Sun’s story unique is the postmortem from its own CEO after the meltdown

And as you’ll see in a moment, his analysis is important for you and me in this current market environment.

In 2002, Scott McNealy, the CEO of Sun Microsystems, looked back at the jaw-dropping climb of his company’s stock and had the following to say to investors who bought near the top and found themselves destroyed when the bubble burst:

Two years ago, we were selling at 10 times revenues when we were at $64.

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends.

That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company.

That assumes zero expenses, which is really hard with 39,000 employees.

That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal.

And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64?

Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes.

What were you thinking?

Well, investors weren’t thinking.

They were wrapped up in the excitement of the transformative power of the internet… they were watching explosive gains in internet stocks… and they wanted to get rich.

This past May we compared Sun Microsystems to AI-darling Nvidia

Nvidia had just come out with great earnings, and with AI excitement rippling through the market, the stock price went vertical.

From May 24th through May 30th, the Nvidia erupted 31% (a longer timeline for context below).

Source: StockCharts.com

Source: StockCharts.com

And how did this leap impact the price-to-sales ratio?

Did it shoot up to maybe 8?

Perhaps it mirrored Sun Microsystems and that laughable 10 multiple?

Maybe it reached an even more absurd valuation at 12 or 13?

It hit 40.

Let’s borrow McNealy’s quote about Sun and adapt it for Nvidia

Imagine yourself seated before your computer back in May, logged into your brokerage account, considering buying Nvidia stock at that price.

Behind you stands Nvidia’s CEO Jensen Huang saying…

At 40 times revenues, to give you a 40-year payback, I have to pay you 100% of revenues for 40 straight years in dividends.

That assumes I have zero cost of goods sold… That assumes zero expenses… That assumes I pay no taxes… And that assumes with zero R&D for the next 40 years, I can maintain the current revenue run rate for 40 years.

Now, having done that, do you really want to buy my stock at 40X-revenues?

Do you realize how ridiculous those basic assumptions are?

What are you thinking?

Well, people weren’t thinking, they were feeling. And the dominant emotion was greed.

But if you think Nvidia’s stock price was about to crash, think again.

Between late-May and mid-July, Nvidia’s stock continued rising

That stratospheric price-to-sales ratio climbed from 40 to nearly 46.

Meanwhile, was Wall Street recognizing the absurdity of this valuation?

Not really. Analysts were upping their price targets.

For example, in July, Citi boosted its estimate for Nvidia shares to $520 from $420. The Citi analyst behind the new target even suggested Nvidia could surge as high as $600.

Larry McDonald, editor of The Bear Traps Report, had an opinion that mirrors our in the Digest…

“The clown show rolls on.”

Here’s his full tweet in response to Citi’s higher price target:

Source: @Convertbond

Source: @Convertbond

The problem is that when a stock is priced for perfection, there’s nowhere to go but down when the illusion of perfection inevitably disappoints

Since the beginning of September, Nvidia is down 11%, having dropped as much as 17%.

And that price-to-sales ratio? It’s fallen from a high of 46 down to 33.

But if our hypergrowth expert Luke Lango is correct, what we’re seeing today is just a prelude to something far worse.

Here’s Luke:

The most popular AI stock on Wall Street is about to crash and burn. [Nvidia] could be just a bearish footnote in the history books.

This likely raises eyebrows for some Digest readers. After all, Luke is incredibly bullish on top-tier AI stocks. And isn’t Nvidia the poster child for top-tier AI stocks? Taken one step further, wasn’t Nvidia a holding in Luke’s Innovation Investor portfolio?

It was – until Tuesday when he recommended subscribers sell it for a 1,000% gain.

Let’s go to Luke for the story:

Nvidia has morphed into the poster boy for the AI boom in 2023. Burgeoning demand for the firm’s next-generation GPUs, which are used to make AI models, has made NVDA the hottest AI stock on the Street.

And deservedly so.

Nvidia’s revenues have surged, along with its profits and share price…

But the AI Boom is shifting out of Nvidia’s favor.

NVDA stock was the No. 1 AI stock to buy in 2023. Now we think it could turn into the No. 1 AI stock to sell.

The story here is pretty simple.

Nvidia has benefitted from a huge demand surge in 2023, primarily because Big Tech firms were looking to build new AI models with its GPUs. But that surge will prove temporary because those same Big Tech firms that have been fueling the surge are now moving away from Nvidia to develop their own chips.

I won’t go into all the details here in the Digest due to space limitations, but Luke’s analysis is fantastic, revealing the dangerous position in which Nvidia now finds itself. I encourage you to read it for free right here.

We’re moving beyond Nvidia because the broader AI sector is at risk as well

To be clear, we remain overwhelmingly bullish about AI, its impact on our world, and its ability to generate transformative investment wealth. However, that doesn’t give the AI sector a free pass to let its valuation go to the moon without earnings eventually backing the hype.

In the meantime, the stock price of even a great AI company can become so egregiously inflated that the stock is no longer a wise investment – even though the business itself remains top-tier.

We’re not the only ones who feel this way.

As one illustration, in late-August, Morgan Stanley downgraded a wonderful AI company – Palantir. The analyst, Keith Weiss, suggested the data analytics leader could crash 45%.

From Weiss’ note to investors:

Going forward, we believe the onus for stock outperformance shifts towards investors now looking for tangible revenue contribution from these Generative AI initiatives in the months ahead.

[That’s] an expectation which may be disappointed given Palantir’s lack of a monetization strategy for AIP, [meaning “AI platform”] and the early stage of development of enterprise Generative AI solutions.

Even if you disagree with Weiss about Palantir, his challenge rings true for the broader AI sector…

We’re now moving beyond the initial hype phase of “hey, we’re an AI company! Buy our stock at any price!” Instead, investors are beginning to demand more evidence that AI initiatives are worth inflated stock prices.

If that evidence is slow in materializing, things will get bumpy.

I’ll note that while Palantir has been climbing over the last few sessions, the stock has fallen as much as 30% since early-August, when its price-to-sales ratio was over 21. It’s still down 19% as I write.

Source: StockCharts.com

Source: StockCharts.com

AI investors would be wise to remember that a study of stock market history shows, time and again, that when it comes to valuations, gravity always wins.

But how do you know if it’s time to sell Palantir, or any other AI stock?

Well, it would help if you could discern between “normal volatility” that might drag down a stock’s price temporarily, even though a broader bullish trend is still in place… versus irregular volatility that suggests “this time it’s different,” meaning an exit is the wiser move.

But that knowledge requires a familiarity with every stock’s unique volatility fingerprint. How is anyone supposed to know that?

Earlier this week, our macro expert Eric Fry sat down with Keith Kaplan, the CEO of our corporate partner TradeSmith. During this 11X Accelerator Event , they discussed the answer – it has to do with something Keith calls a “VQ” or “Volatility Quotient.

From Keith:

The VQ measures the inherent movement in a stock, “the single most important number in investing.”

You can use this number to know exactly when to buy, how much to buy, and when to sell any stock, fund, or crypto. It’s really powerful.

Knowing a stock’s VQ helps investors avoid selling too early (missing gains that can make all the difference in a portfolio) while also helping them not hold too long (preventing reasonable losses from becoming catastrophic losses).

If you missed their live presentation, Eric and Keith are making a free replay available right here. If you have lots of lofty-valuation AI stocks in your portfolio today, I’d encourage you to check this out.

Stepping back, if Luke is right, Nvidia is about to face serious headwinds for its chip demand. At the same time, its valuation remains at a very rich 33.

If you own it, make sure you have a plan for all types of market environments going forward.

Have a good evening,

Jeff Remsburg

More From InvestorPlace

- Musk’s “Project Omega” May Be Set to Mint New Millionaires. Here’s How to Get In.

- ChatGPT IPO Could Shock the World, Make This Move Before the Announcement

- The Rich Use This Income Secret (NOT Dividends) Far More Than Regular Investors

The post Luke Lango Just Sold an AI Darling appeared first on InvestorPlace.

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…