Economics

It’s Time To ‘Proof’ Portfolios From Looming Recession

It’s Time To ‘Proof’ Portfolios From Looming Recession

Authored by Simon White, Bloomberg macro strategist,

Markets are set for greater volatility…

It’s Time To ‘Proof’ Portfolios From Looming Recession

Authored by Simon White, Bloomberg macro strategist,

Markets are set for greater volatility as the economy soon enters a recessionary state, but portfolios with limited duration exposure and increased allocation to real assets should be protected from the worst of the downturn.

This will not be a run-of-the-mill recession, with equities potentially holding up better than in previous slumps, and fixed-income assets unlikely to offer the same degree of protection due to elevated inflation.

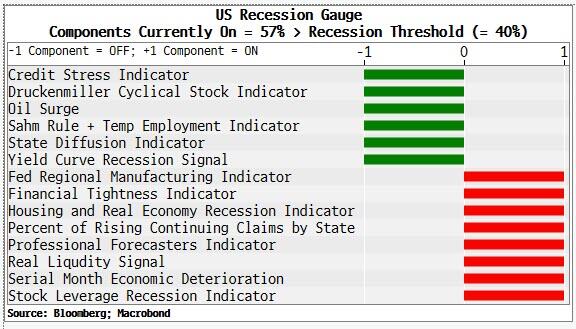

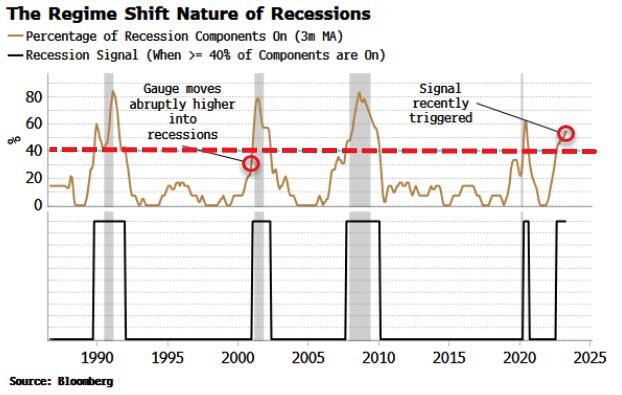

Recessions are notoriously tricky to forecast, but I have attempted to unpick the knot with the creation of a Recession Gauge. It looks at a wide range of market and economic data to signal when the US is likely to tip into recession. It recently triggered, suggesting the US is, or will very soon be, in a recession.

Recessions happen suddenly. Phase transitions in physics are when a substance changes state. When a pot of water is heated to 100C it goes through a phase transition from a liquid to a gas. At that point, the water goes through a profound and abrupt change.

Economies do likewise when they enter a recession. There is not a steady, linear change between a non-recessionary and recessionary state but a rapid and highly non-linear one. The historical series of the Recession Gauge captures their suddenness well.

Despite its likely rapid onset, the relative period of calm since the banking turmoil affords an opportunity to re-mold portfolios in preparation for the recession.

Specifically, portfolios with the following traits will be better placed to weather the coming economic turbulence and concomitant elevated inflation:

-

Low exposure to currently more overbought sectors such as tech and semis

-

Increased exposure to currently lagging, lower-duration sectors such as energy, utilities and pharmaceuticals

-

Limited in longer-duration fixed-income exposure, i.e. have lower exposure to longer-maturity bonds

-

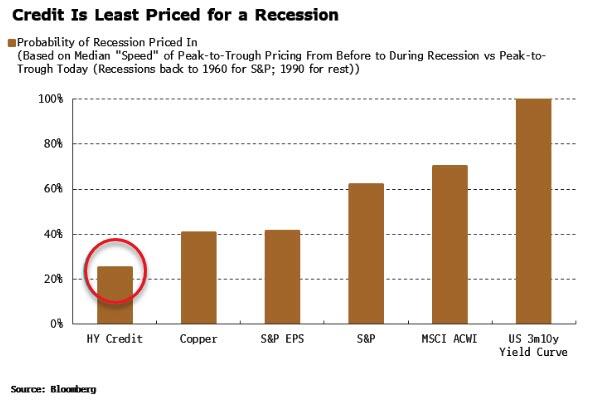

Low exposure to credit, the asset class most mis-pricing recession risk

-

An increased allocation to commodities, precious metals and other real assets

-

Overall, structured to benefit from higher volatility

In this recession, the usual playbook of buying bonds and rotating into more defensive equity-sectors is likely to be far from optimal. With the specter of inflation hovering in the background – and liable to start rising again later in the year – duration risk is a key consideration.

In a zero interest-rate, forward-guidance world, longer-term debt all the way down to cash looks more fungible, while growth stocks tend to have a material advantage over value stocks given low borrowing costs and the ability of larger companies to term out debt for longer.

But when inflation is high as it is today, growth stocks lose their comparative advantage. There are many exceptions – some growth stocks will have strong pricing power that will outweigh the downsides of having lumpy cash-flows expected far in the future – but an overarching rule of thumb is that portfolios with lower duration risk will be better placed to withstand an inflationary recession.

Similarly, bonds may not fulfill their traditional role as a recession hedge or safe haven to the same extent. Reducing fixed-income duration as much as feasibly possible is prudent when rates have more upside potential than they have had for decades. Bonds are pricing in a recession, but a garden-variety one where inflation falls and remains contained.

But even more egregiously mis-priced is credit. Of the main asset classes, it is the one least expecting a recession, based on historical pricing behavior. Credit’s riskiness is amplified when the fixed-income duration risk is factored in. Current relatively tight spreads are an opportunity to reduce credit exposure.

On the other hand, portfolios with an increased allocation to real assets stand to fare well as these outperform when inflation is heightened. In the 1970s, commodities were the best performing asset class and the only one to deliver a positive real return, with bonds, credit and equities all underperforming relative to inflation.

Commodities tend to move sideways in the first few months of a recession, but that’s as they typically tend to have most of their selloff before the recession starts. However, in this inflationary recession commodities look to be at an attractive entry point after being in a downtrend for most of the last year.

Gold also typically sells off prior to a recession and only begins to rally after it’s begun, but its rally in recent weeks suggests the precious metal, along with silver, is sending a signal that this will not be a typical slump.

Lastly, and no less importantly, implied and realised volatility are set to rise again as the economy goes through the recession phase-transition. Portfolios explicitly or implicitly short volatility will be exposed to greater downside, as all assets tend to experience a sharp increase in volatility soon after a recession begins.

The usual rules are unlikely to apply in a recession that now looks unavoidable. Stocks may hold up better than normal, if recent reliable signals are prescient, while bonds may struggle to deliver a positive real return.

That leaves many portfolios unprepared, for which the current pre-recession interlude offers the chance to remedy.

Tyler Durden

Tue, 04/18/2023 – 09:25

gold

silver

inflation

commodities

markets

metals

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…