Economics

Big Misses From Alphabet, Amazon, And Apple Confirm “The Web 2.0 Bubble Is Bursting”

Big Misses From Alphabet, Amazon, And Apple Confirm "The Web 2.0 Bubble Is Bursting"

By Dhaval Joshi of BCA Research

The Web 2.0 bubble is…

Big Misses From Alphabet, Amazon, And Apple Confirm “The Web 2.0 Bubble Is Bursting”

By Dhaval Joshi of BCA Research

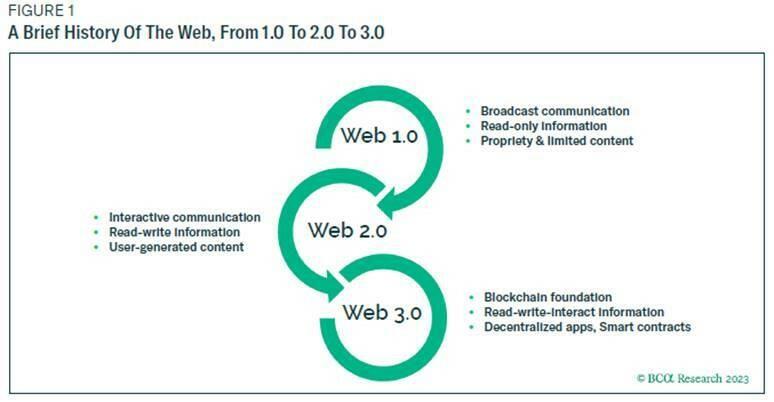

The Web 2.0 bubble is bursting, with far-reaching consequences. But to understand the consequences, let’s begin with a brief history of the web: how it evolved from the original Web 1.0 to the current Web 2.0, and how it will evolve to the coming Web 3.0.

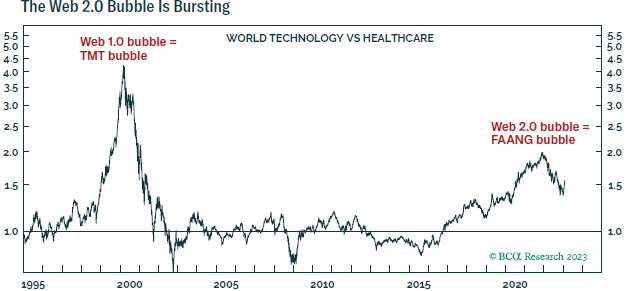

The Web 1.0 Bubble Burst In 2000, The Web 2.0 Bubble Is Bursting Now

If you are over the age of 30, you will remember the original Web 1.0 of the 1990s. Web 1.0 was dull. It was like having a massive encyclopaedia at your fingertips – with static, non-interactive, read-only content, whose ownership remained with its creators: typically, the traditional media, and publishing companies.

Nevertheless, facilitated by the telecom and tech giants of the time, Web 1.0 expanded the reach of traditional media content to a massive global audience. Thereby was born the Web 1.0 boom, otherwise known as the technology, media, and telecom (TMT) or ‘dot com’ boom. But as in all booms, hopes for a new paradigm of super-growth were shattered, and the Web 1.0 bubble burst in 2000.

Then, around 2005, came Web 2.0. The great leap forwards was user-generated content combined with interaction, which became real-time with the introduction of iPhones. First came blogs, then forums, and finally the explosion of social networks such as Facebook and YouTube.

However, Web 2.0 also became the web of big data and advertising. Most of the content – whether blogs, videos, or photos – is user-created, but the effective ownership lies with a handful of ‘Web 2.0 oligopolies’ that control or own the networks: Facebook (now Meta), Amazon, Apple, Netflix, and Google (now Alphabet), collectively called the ‘FAANG’ stocks.

The Web 2.0 oligopolies realised that web users produced vast quantities of data about their lifestyles and consumption habits, which the companies could sell to advertisers and marketers. And on that growth model was born the Web 2.0 profit boom, otherwise known as the ‘FAANG’ boom of the 2010s.

To visualise this, compare the performance of the US stock market excluding tech, Amazon and Netflix with the European stock market excluding tech, and the difference through the past decade melts away. Proving that the US market’s spectacular outperformance is almost entirely due to the Web 2.0 boom.

But now, the Web 2.0 bubble is bursting, because the scandals of privacy protection and content ownership have put paid to the 2010s growth model. Just as in 2000 for the Web 1.0 companies, hopes for a new paradigm of growth for the Web 2.0 oligopolies have been shattered.

All of which brings us to Web 3.0. This is still a work in progress, but after the scandals of Web 2.0, we know the key requirements for Web 3.0 – to protect everyone’s data as well as to reward users for content creation and network participation. This means decentralisation, with no third party imposing the rules. Hence, Web 3.0 will almost certainly be blockchain based and incorporate its technology, such as blockchain tokens and smart contracts.

The Web 3.0 boom might be imminent, or it may be some years away. But just as the Web 1.0 bubble burst several years before the Web 2.0 boom was born, the bursting of the Web 2.0 bubble is not premised on the birth of the Web 3.0 boom. To repeat, the Web 2.0 bubble is bursting because the scandals of privacy protection and disenfranchising content creators have shattered the growth model of the Web 2.0 oligopolies. And the bursting of this bubble has long-term consequences, which we will now discuss.

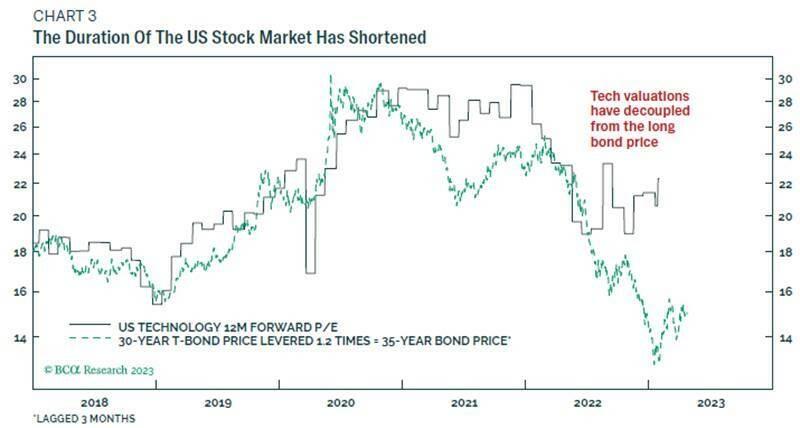

Consequence 1: The Duration Of The US Stock Market Has Shortened

The first consequence is a technical point but nonetheless of huge importance. The US stock market’s duration has shortened. The duration of an investment is simply the time to the average cashflow that the investment generates. As the growth model of the dominant FAANG stocks has shattered, their expected cashflow profile has been pulled forwards, shortening the duration of the stock market.

This is important because the duration of any investment determines its sensitivity to a change in bond yields. The shorter the duration, the smaller is its price change for a given move in the bond yield.

The US tech sector’s duration has shortened. On the way up through 2018-21, the valuation tracked the 35-year bond price. But on the way down through 2022, it has not tracked the 35-year bond price.

The good news of shortened duration is that, through 2022, the US stock market’s valuation fell far less than it would have done with longer duration. But the bad news is that the US stock market’s valuation will rise less when bond yields plunge.

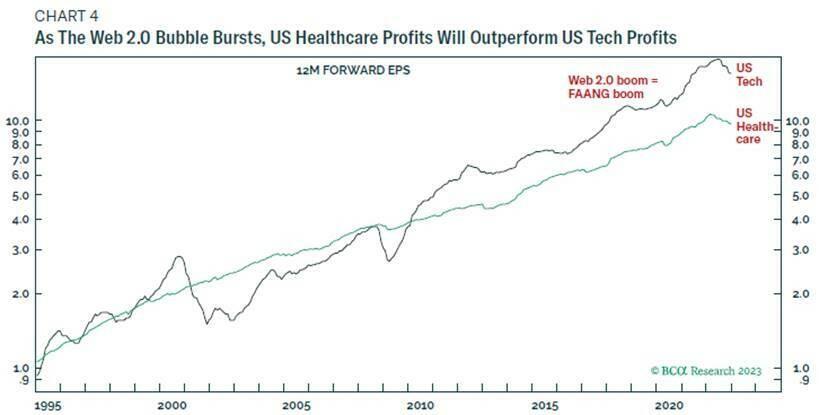

Consequence 2: Healthcare Will Outperform Technology

In the decades preceding 2010, profits in the US tech sector trended higher broadly in line with those in its fellow ‘growth sector’ US healthcare. But after 2010, US tech profits pulled away from healthcare. As already explained, this profit acceleration was almost entirely attributable to the Web 2.0 boom.

But now that the Web 2.0 bubble is bursting, the profit trends of US tech and healthcare are likely to re-converge, which means that the profits of US healthcare will outperform those of tech. Yet US healthcare is still trading at a 20 percent valuation discount to US tech.

The combination of superior profit growth and a cheaper valuation means that healthcare is likely to outperform tech massively as the Web 2.0 bubble fully bursts. Our preferred expression of this in the past year has been to overweight US biotech versus tech. This structural position is already up 30 percent, but there is a lot further to go. Stick with it.

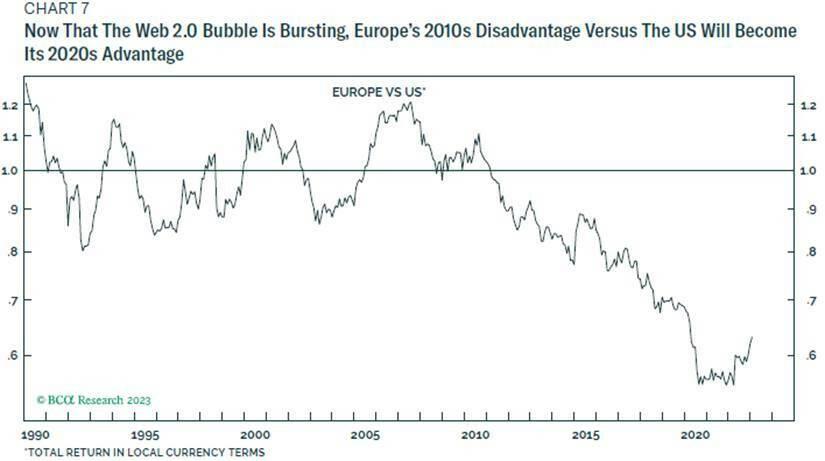

Consequence 3: Europe Will Outperform The US

Finally, to repeat, European versus US stock market underperformance through the 2010s is almost entirely attributable to the Web 2.0 boom. If we exclude tech, Amazon and Netflix from the US stock market and compare with the European stock market ex tech, Europe’s underperformance melts away.

In this regard, the Web 2.0 boom, whose benefit was focused in the US FAANG stocks, was different to the Web 1.0 boom, which had no geographical bias, at least between the US and Europe. The Web 1.0 boom boosted the European market as much as the US market.

Hence, until the 2010s there was no structural downtrend in European versus US stock market performance.

But now that the Web 2.0 bubble is bursting, Europe’s 2010s disadvantage versus the US will become its 2020s advantage. A European renaissance is about to begin, at least relative to the US. Hence, today we are opening a new position on a structural (over 2 year) time horizon:

Tyler Durden

Fri, 02/03/2023 – 15:00

bubble

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…