Companies

Getchell Gold, a case study of “gold in the ground” – Richard Mills

2023.02.15

Historically, all junior resource companies can be evaluated and ranked utilizing four criteria: share structure, people, project and working…

2023.02.15

Historically, all junior resource companies can be evaluated and ranked utilizing four criteria: share structure, people, project and working capital.

None however, is more accurate for evaluation purposes, than “insitu metal value”.

That’s because an early-stage explorer has no tangible value, it isn’t until a junior has established a resource that an informed evaluation can be assigned to what has become an advanced exploration/ development company with a deposit.

One way to determine the value of a junior is comparing the price of the metal(s) in the deposit to the value of the company’s metal in the ground, whether its copper, gold or silver etc. Doing so can sometimes reveal huge discounts.

For example in 2019, Wall Street firms Cantor Fitzgerald and GMP Research spotted Euro Sun Mining, owner of the biggest undeveloped gold mine in Europe. Cantor Fitzgerald placed a short term price target of $2.10 a share, implying an upside of 406%, while GMP’s $3.00 target implied a 641% increase.

Why the huge upside? Because the gold in the ground was cheap. Euro Sun Mining reportedly had over $10 billion of gold equivalent on its books, but the modest market capitalization of $30 million valued each ounce of gold at just $3. The huge delta made for a compelling investment case: why buy gold at the 2019 price of $1,342 an ounce, when you can purchase a tiny gold junior for pennies on the dollar, with $10 billion in gold equivalent (gold + other metals) and the potential for a 6-bagger?

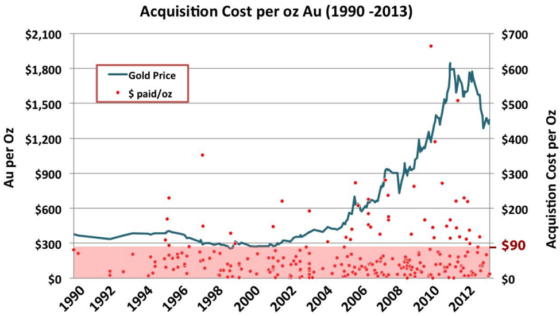

A Cipher Research Report published in 2015 examined a 24-year history of mergers and acquisitions to determine the real value of gold in the ground and to incorporate that value into their project and company valuation models.

Cipher determined that in the most basic terms, the value of a gold mineral project is equal to the number of ounces in the ground that will be potentially extracted times the value or price of an ounce in the ground.

Value = Quantity x Price

Cipher examined 253 transactions involving gold projects or companies owning a gold project, which were acquired in the period 1990-2013.

The conclusions drawn from their statistical analysis include:

- 80% of all transaction occur at $90/oz or less, over half (56%) occurred below $45/oz

- With the exception of a few outliers, there is little or no correlation to the price of gold

- The average price paid for gold in the ground was $63/oz

- The median price was $39/oz

- Slightly higher premiums were paid for projects in development or production versus resource definition stage. Average price is 33% higher ($52 vs $69/oz), Median is 18% higher ($34 vs $40/oz)

- There was surprisingly little difference in prices based on geographical location

- The size of the resource was not positively correlated to the price paid (In other words miners pay for the quality of the project not the quantity of oz)

Getchell Gold

Time to move from the theoretical to the practical. One of my favorite gold companies right now is Getchell Gold (CSE:GTCH, OTCQB:GGLDF). The Nevada-based junior’s flagship gold property is Fondaway Canyon, located a short drive from Reno, with a number of prominent mines and deposits to the north.

Getchell carried out three drill programs, in 2020, 2021 and 2022. The aim was to significantly upgrade the 2017 resource estimate into a new resource, that combined the drill results from all three drill programs.

The new resource estimate, released in November, nearly doubled the previous one, of 1.1 million ounces. It is 2 million ounces, including 550,000 ounces in the indicated category grading 1.56 grams per tonne, and 1.5Moz inferred, grading 1.23 g/t. There are nine holes that haven’t been included in the resource estimate because they missed the cut-off date, and Getchell plans to do a lot more drilling on it’s wide open deposit in 2023.

GTCH’s resource estimate is 2,058,900 ozs gold. Cipher’s’s average price paid for an oz of gold in the ground, between the years 1990-2013, was US$63.00.

$63.00 x 2,058,900 = $129m / 122 osfd = $1.06 per share.

Cipher’s brilliant report is out-dated in two areas. First resource nationalism is now much much worse then in the years, 1990-2013, covered in their report. Imo, an oz of gold in Nevada is worth more than say in Burkino Faso. Second, again over the years this report was concerned about, gold’s average price was not, for the most part, anywhere near what it’s been trading for the past 10 years.

Baby gold bull

In January gold surged to a six-month high, and analysts expect the precious metal to scale new heights in 2023.

Bullish outlook for metals in 2023

After suffering for much of 2022 due to an elevated US dollar and higher bonds yields, gold has trended up since the beginning of November, fueled by expectations of less Fed tightening, a lower US dollar, and gold purchases from central banks underpinning demand.

“In general, we are looking for a price-friendly 2023 supported by recession and stock market valuation risks — an eventual peak in central bank rates combined with the prospect of a weaker dollar and inflation not returning to the expected sub-3% level by year-end — all adding support,” CNBC quotes Ole Hansen, head of commodity strategy at Saxo Bank.

“In addition, the de-dollarization seen by several central banks last year when a record amount of gold was bought look set to continue, thereby providing a soft floor under the market.”

The news outlet has two more analysts sounding even more bullish on gold. Eric Strand, manager of the AuAg ESG Gold Mining ETF, predicts that 2023 will see an all-time high and the start of a “new secular bull market,” based on the fact that central banks are adding more gold to their reserves.

Adam Hamilton has commented on the relative “youth” of the current gold upleg which started in late September. While at time of writing in mid-December, Hamilton observed gold climbing 12.8% over 2.8 months, he noted the previous four uplegs averaged much bigger, 28.8% gains over longer periods of 7.9 months. “This current upleg is likely only getting started, with a lot to prove,” Hamilton wrote.

He also said major gold uplegs are three-stage events, with each having distinct drivers. “The first and smallest stage isn’t even finished yet, which bodes very well for gold and its miners’ stocks.”

Peter Grandich says he’s bullish on gold because two “detrimentals” that were prevalent in the 1980s and 1990s, are no longer present: central bank selling; and widespread manipulation in the so-called gold paper markets (gold ETFs).

The veteran gold analyst told Palisades Gold Video “I think this is the best gold bull market we’ve ever seen. Not only do [central banks] not sell now, but they’re purchasing in record levels… they’re not buying it for speculation, they’re not looking to trade it, they’re buying it for a particular reason(s) that they see… whether it’s a coming gold-backed currency, a move away from the dollar, whatever it is, that is happening for a reason, and when they’re like that, it’s like ‘don’t bet against the Fed.’ Don’t bet against the central banks when it comes to gold.”

Rise of the gold-backed e-yuan

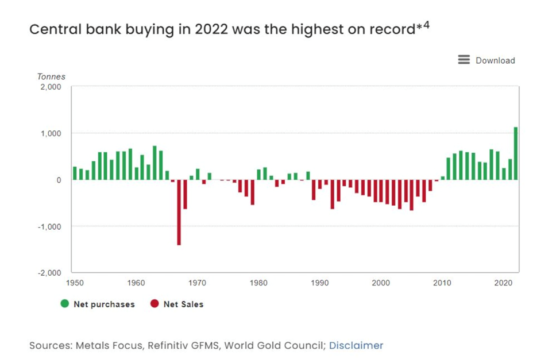

His comments are supported by recent figures from the World Gold Council, indicating that central banks last year bought the most gold on record. Reuters states:

Central banks added a whopping 1,136 tonnes of gold worth some $70 billion to their stockpiles in 2022, by far the most of any year in records going back to 1950, the World Gold Council (WGC) said on Tuesday.

The data underline a shift in attitudes to gold since the 1990s and 2000s, when central banks, particularly those in Western Europe that own a lot of bullion, sold hundreds of tonnes a year.

Since the financial crisis of 2008-09, European banks stopped selling and a growing number of emerging economies such as Russia, Turkey and India have bought.

Central banks like gold because it is expected to hold its value through turbulent times and, unlike currencies and bonds, it does not rely on any issuer or government.

Also benefiting gold, said Grandich, is the shift in ETF buying, from the two main Western markets, London and New York (the Comex) to the Far East. “I’m not saying [manipulation] has gone, but clearly, because of convictions with spoofing, and other reasons, that’s not a detrimental. You take those two used-to-be negative factors out of the equation, gold has bullish implications. And that’s why I’m confident that we’re going to make a not-just-nominal high, but adjusted for inflation, which will be $2,300-2,400.”

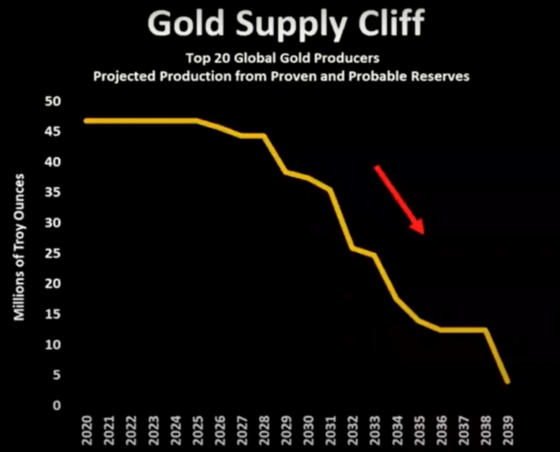

Peak gold

In a world of resource depletion, it falls to gold exploration companies to fill the gap with new deposits that can deliver the kind of production required to meet gold demand, which is currently out-running supply.

In 2021, 4,021 tonnes of gold demand minus 3,560.7t of gold mine production left a deficit of 460.3t. Only by recycling 1,150t of gold jewelry could the demand be met.

The gold market continues to experience tightness due to difficulties expanding existing deposits, and a pronounced lack of large discoveries in recent years.

The chart below by Crescat Capital predicts the proven and probable reserves of the top 20 gold producers will start to fall in 2028, and continue their downward slide to 2039. If the forecast is correct, the top 20’s total gold reserves will go from 45-46Moz in 2028, to zero in the following 10 years.

“Gold companies are actively out searching for new projects, but really because of the lack of resources in the next few years, we need companies that can provide a lot of ounces to the market,” says Rob Kientz from GoldSilver Pros.

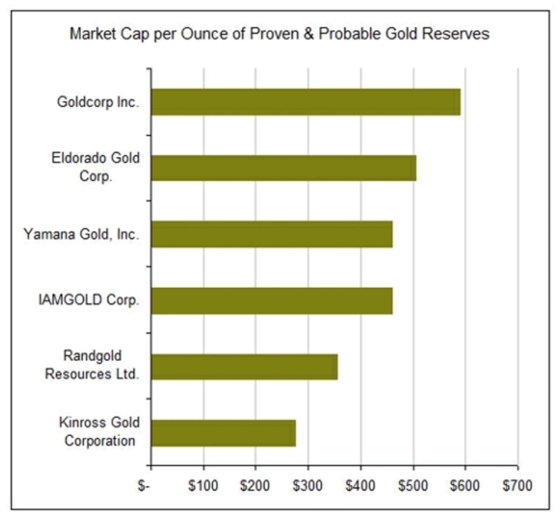

Back in 2011, Seeking Alpha noticed that many gold companies own the rights to millions of ounces of in-the-ground proven and probable gold (the P&P category is the highest level of certainty). A shareholder in one of these companies indirectly owns a portion of this gold.

The chart below shows the cost, based on market capitalization, to acquire each ounce of proven and probable gold reserves held by Goldcorp, Eldorado Gold Corp., Yamana Gold, IAMGOLD, Randgold Resources and Kinross Gold.

Notice that the gold could be purchased for as little as $277 per ounce, compared to the gold price at the time of $1,640/oz.

As Seeking Alpha commented, I believe mining companies see the same value. Why would a gold miner spend millions of dollars exploring, fighting environmental issues and building a mine when millions of in-the-ground ounces can be bought at a steep discount to the spot price?

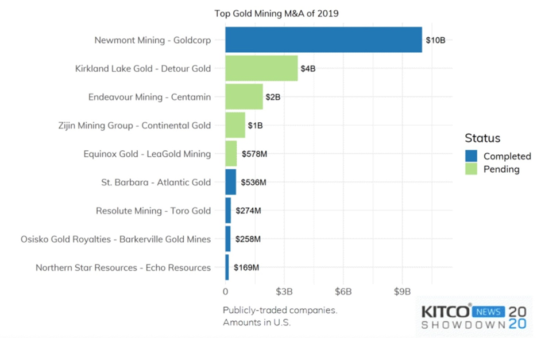

A 2019 column by Sprott, while three years old, is useful in that it points out the ignition that year, of a new gold mining mergers and acquisitions (M&A) cycle. Readers will recall some of 2019’s blockbuster gold deals, including the $10-billion merger of Goldcorp with Newmont Mining, Kirkland Lake Gold’s acquisition of Detour Gold, and Zijin Mining’s $2B purchase of Continental Gold.

The column notes the tepid gold price environment since 2011 — though remember gold hit an all-time high of $2,034 in the fall of 2020, and a six-month high in January 2023 — forced many gold producers to decrease their exploration focus, therefore there was a drop in new discoveries just as global gold reserves were, and are, being depleted.

Sprott states:

The challenging environment is forcing miners to strategically combine to reduce expenses and improve their operations. We expect these mergers will create a cascading effect in the industry as the combined entities shed non-core assets and prompt other companies to rethink their strategic priorities. Within the sector, we also see meaningful gradations of valuation between larger- and small-cap companies which could further fuel the cycle.

Our new investment strategy, Sprott Hathaway Special Situations Strategy, pays attention to many likely takeover targets and we believe it has the potential to produce positive returns even in the absence of rising gold prices.

Conclusion

As for Getchell Gold, the question becomes, how do you acquire cheap gold ounces in the ground, while we teeter on the edge of what Adam Hamilton, Peter Grandich, myself and others, are calling the next gold bull market?

Gold has corrected from a six-month high in January but the fundamentals are clearly supportive of the precious metal.

Getchell’s resource estimate is already out of date. The company has released nine fantastic holes that missed the cut-off date for inclusion in the RE. Preparations for a much larger 2023 drill program than the 3 previous drill programs are underway.

We therefore see Getchell Gold as an excellent value play, and highly investable in a rising gold price environment characterized by central bank buying and tighter supplies due to depleted gold reserves and a lack of new discoveries. Gold majors wanting to grow their reserves without incurring large capital expenditures are hunting for cheap gold in the ground. Getchell Gold has 2 million ounces in Nevada and the outer limits of the deposit have yet to be encountered by drilling.

Getchell Gold Corp.

CSE:GTCH, OTCQB:GGLDF

Cdn$0.33, 2023.02.14

Shares Outstanding 105m

Market cap Cdn$34.6m

GTCH website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard owns shares of Getchell Gold Corp. (CSE:GTCH). GTCH is a paid advertiser on his site aheadoftheherd.com

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…

GoldTalks: Going big on ASX-listed gold stocks

Aussie investors are spoiled for choice when it comes to listed goldies, says Kyle Rodda. Here are 3 blue chips … Read More

The post GoldTalks: Going…

Gold Digger: ‘Assured growth’ – central bank buying spree set to drive gold higher in 2024

Central banks will drive the price of gold higher in 2024, believe various analysts Spot gold prices seem stable to … Read More

The post Gold Digger:…