Uncategorized

Victory Battery Metals: Smokey lithium project moves from early-stage to advanced-stage with completion of spring drill program – Richard Mills

2023.05.13

Victory Battery Metals: Smokey lithium project moves from early-stage to advanced-stage with completion of spring drill program

Victory Battery…

2023.05.13

Victory Battery Metals: Smokey lithium project moves from early-stage to advanced-stage with completion of spring drill program

Victory Battery Metals (CSE:VR,FWB:VR61,OTC:VRCFF) is making excellent progress at its flagship Smokey claystone lithium project in Nevada, where the company has just completed a four-hole drill program totaling 1,996 feet, or 608 meters.

The program is a continuation of drilling in 2022, the assays from which clearly showed that the claystones are mineralized with lithium. Three years of geological study, surface sampling and drilling has confirmed that the property is underlain by thick sections of claystone rocks.

According to VR, the recently completed spring, 2023 drill program has significantly expanded the area and thickness of the targeted claystone sequences of the Esmeralda Formation, thus changing the project’s development status.

“Our team has reviewed the onsite findings and have determined that this drill program moved the project from an early-stage project towards an advanced stage project,” Victory Battery Metals’ President and CEO Mark Ireton remarked in a May 2 news release.

The news also said the program edges the project closer to establishing a deposit at Smokey as the company awaits the assay results.

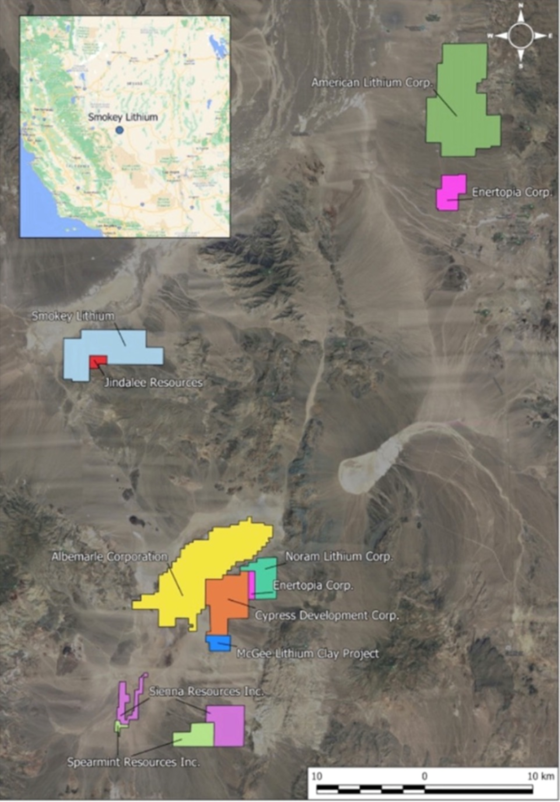

The Smokey lithium property lies approximately 35 km north of Clayton Valley, NV, and 32 km west of American Lithium’s TLC project, within the Big Smokey Valley.

It is also in Esmeralda County, a prolific region for very large-tonnage lithium clay deposits, with grades up to and exceeding 900 ppm.

These include Noram Ventures (166Mt @ 900 ppm), Century Lithium (formerly Cypress Development, 593Mt @ 1,032 ppm), American Lithium (495Mt @ 1,000 ppm), Spearmint Resources, Enertopia and Jindalee Resources.

Note that the project is in close proximity (<35 km) to North America’s only producing lithium mine, Albemarle’s Silver Peak. Smokey surrounds Jindalee’s Clayton North lithium prospect on three sides, with excellent access and relatively flat ground.

“Within those valleys there is so much near-surface lithium-rich deposits, we feel we’re in a strategic area with 350 claims and 17,000 acres (6,879 hectares),” Ireton told the Investing News Network in a recent video interview.

As previously noted, drill hole locations were selected to extend strong lithium mineralization found in hole 9 during the 2022 maiden drill program. The fourth hole was selected specifically to determine the strength of lithological correlation between holes 22-09, 23-01, 23-02 and 23-03. Victory’s exploration team determined that the most compelling place to drill hole 23-05 would be 1 km to the west-southwest of hole 23-03. Assays for all four holes are pending.

VR states: “As a result, the claystone intercepts observed in hole 23-05 have clearly shown a significant thickness of terrific looking claystones on the property. The position of the 23-05, as a spatial outlier, suggests further drilling to the southwest will be very promising for discovery of additional intercepts of a classic Clayton Valley-style claystone-hosted lithium zone.”

All four holes reached claystone at depths of between surface and 600 feet (182.8m). Thicknesses varied from 144 to 249 feet (43.8 to 75.8m). Coloration when hydrated ranged from light gray with calcite veins, to blue-gray and brown, to tan, brown, green and black.

Flush with a $1.925 million private placement cash injection, Victory Battery Metals is in good shape to deliver on its 2023 field program.

Ireton told INN that receipt of favorable assay results from the four holes drilled at Smokey would lead to a phase 3 drill program, with holes drilled to a depth of 600 feet.

“Just to continue to prove out what we have currently found. The last hole last year was the one that really assisted us in rejigging our focus to this current program, and we’re very optimistic that based on the look of the core, we may obtain some favorable lab results.”

Ireton also said between the five properties in the company’s portfolio, and the cashed-up treasury, Victory Battery Metals is “ready to go with all of these projects, which all have significant work programs either underway currently or to be commenced in late spring early summer.”

Along with Smokey, VR also holds two other lithium properties, Stingray in Quebec and Georgia Lake in Ontario.

Stingray I consists of four claims totaling 204 hectares extending directly from the south property line of Patriot Battery Metals’ Corvette project. Stingray II comprises 40 claims of 2,041 hectares situated south and southwest of Corvette.

In February, Victory announced a major expansion of the Stingray properties, acquiring 280 new claims and bringing its total claims in the area adjacent to Patriot’s Corvette to 347.

Victory says its holdings now represent a large ground position in an underexplored area within the emerging James Bay Lithium District.

Victory Battery Metals acquires 17,792 hectares in the James Bay Lithium District

Victory’s Georgia Lake project is 2 km east of Rock Tech Resources’ advanced-stage lithium project within the Georgia Lake lithium district. The company has completed an aerial survey and boots-on-the-ground prospecting is slated to start in early June, with an eye to determining the extent of pegmatites (lithium-bearing rock) on the property.

Ireton pointed to two other projects under development by Victoria Battery Metals. The Tahlo Lake property near Smithers, BC is located within the Babine Copper-gold Porphyry District, along with American Eagle’s NAK project. An aerial magnetic survey that has been completed, is currently under review to determine next steps.

The Saguenay nickel project is located about 10 km south of the Quebec town of the same name. It is made up of five claims totaling 286.3 ha. Ireton noted back in 1959 there was exploration done showing respectable nickel content. While little work has been done since then, he said VR is “currently engaging work programs to prove this out and see what next steps might be there.”

Speaking more broadly with INN, Ireton said Victory’s holdings are “in the right place at the right time,” given the amount of governmental interest in developing battery plants to service the burgeoning electrical vehicle supply chain, and further up the chain, discovering and advancing battery metal deposits.

“It’s being mandated by governments around the world to encourage development of supply, the electric vehicle itself,” he said, noting Volkswagen’s commitment to build its first battery plant outside of Europe, in St. Thomas, Ontario.

Earlier, in December, 2022, the Canadian government and General Motors announced the opening of Canada’s first electric-vehicle manufacturing plant in Ingersoll, Ontario. The plant makes electrified delivery vans and is expected to manufacture 50,000 EVs by 2025.

The next-door province of Quebec has also attracted EV investment. In March, 2021, Lion Electric announced it will build a battery pack manufacturing plant in its home province. The $185 million factory, funded by the Quebec and federal governments who each committed $50 million, will build lithium-ion battery packs capable of electrifying 14,000 medium and heavy-duty vehicles annually.

“Governments are very keen to see growth continue in this area,” says Ireton.

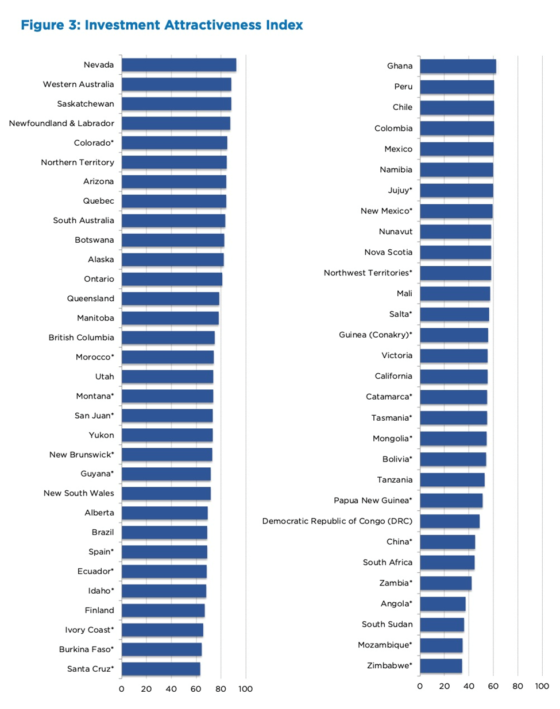

The wind is also at Victory’s back for three other reasons: the recent lithium nationalization in Chile; the even more recent announcement that Nevada has reclaimed top spot as the world’s most attractive jurisdiction for mining investment; and the bullish lithium market.

The lithium nationalization bombshell dropped in April by Chile is good news for North American lithium miners, that are likely to become more important as potential suppliers of the white metal needed for making lithium-ion batteries used in electric cars and trucks, as well as energy storage and an array of consumer electronics.

“Automakers may be more trepidatious around committing to lithium supply deals from Chile until it’s clear what nationalization will look like,” Reuters quotes Caspar Rawles, chief data officer at Benchmark Mineral Intelligence. “Most automakers will have been looking for a diversified portfolio of regional supply before this anyway, but perhaps this makes other regions more appealing.”

It only makes sense that if Chile is unable to provide the needed lithium, it could give fresh impetus to finding new sources of the metal.

One of the best places to explore for and mine lithium is Nevada.

Earlier this month, the Fraser Institute came out with this year’s version of its annual survey of the mining industry. Topping the rankings for investment attractiveness was Nevada, which reclaimed the spot it yielded last year to Western Australia. The latter now ranks second.

Among the reasons for retaining its competitive edge are Nevada’s lack of income tax, the fact that mining is governed under the federal Mining Act of 1872, which would take an act of Congress to change, and that mining taxes are set out in the state’s Constitution.

Lithium market headed for deficit

The global lithium-ion battery industry is expected to grow at a CAGR of 16.4% from 2020 to 2025, reaching USD$94.4 billion by 2025 from $44.2 billion in 2020. Growth will be driven not only by the need for plug-in electric vehicles and hybrids, but grid storage applications for which the dominant technology is lithium-ion.

Demand for lithium carbonate is expected to rise at a compound annual growth rate of 10-14% until 2027, while lithium hydroxide demand is seen climbing at a 25-29% CAGR.

A recent study by BloombergNEF shows that 5.3 times more lithium will be demanded by 2030 compared to current levels.

According to Benchmark Mineral Intelligence (BMI), to meet demand, the global lithium industry needs to invest up to $42 billion by the end of the decade. This works out to $7 billion each year from now until 2028, helping it to meet predicted demand of 2-4 million tonnes per annum by 2030, which is four times higher than the 600,000 tonnes of lithium that was expected to be produced in 2022.

Bloomberg notes the forecast, from a recent BMI report, comes as Europe and North America look to reduce their dependency on Chinese lithium imports and to try to develop their own lithium production.

The Biden administration has earmarked billions to help process key battery metals including lithium, while in Canada, 2022’s budget included CAD$3.8 billion to build a domestic critical metals supply chain.

Despite the healthy trade in batteries, looming supply shortages of battery metals including lithium and graphite could derail the global transition to clean energy, according to Trafigura CEO Jeremy Weir.

Automakers could have problems increasing electric-vehicle output unless there is significant new investment in new supply, said Weir, head of the commodities trading house. He warns higher prices are needed to incentivize miners to bring new production online, and cautions that delayed permitting process could stymie new supply even if prices do move higher (Mining Weekly, March 9, 2023).

Albemarle executives quoted by Reuters warned of the “potential for significant deficits” by the end of the decade without new mines and processing plants.

Fastmarkets previously forecast a small surplus in 2023 but this has been revised to a deficit because of increased battery demand and some expected supply disruptions. The introduction, in the United States, of the Investment Reduction Act, has resulted in Fastmarkets upgrading its forecast for battery electric vehicle (BEV) sales by 80% in 2023 and 107% in 2024.

Mine supply could increase by 35%, year on year, to 984,000 tonnes, mostly fueled by Australia and China, but Fastmarkets is predicting a 2023 deficit of about 14,000 tonnes lithium carbonate equivalent (LCE).

Reuters metals columnist Andy Home agrees that The world has been running short of lithium, with a surge of new supply failing to catch up with a still faster demand wave as the electric vehicle revolution accelerates.

Victory Battery Metals

(CSE:VR,FWB:VR61,OTC:VRCFF)

Cdn$0.06, 2023.05.12

Shares Outstanding 47.3m

Market cap Cdn$4.2m

VR website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard does not own shares of Victory Battery Metals (CSE:VR). VR is a paid advertiser on his site aheadoftheherd.com