Uncategorized

Markets On Edge As Global Yields Hit 15 Year High, China Woes Mount

Markets On Edge As Global Yields Hit 15 Year High, China Woes Mount

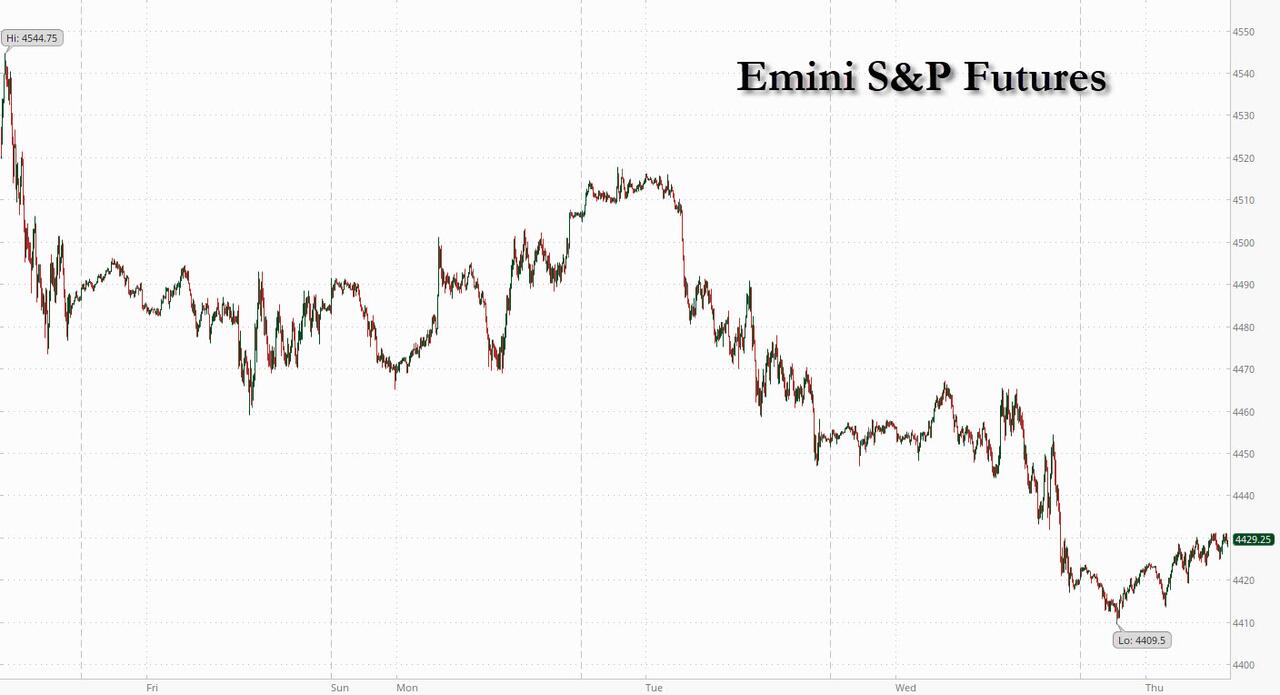

S&P futures reversed earlier losses that brought them perilously close…

Markets On Edge As Global Yields Hit 15 Year High, China Woes Mount

S&P futures reversed earlier losses that brought them perilously close to the 4400 support level, as global govt bond yields extended their recent surge to the highest levels since the financial crisis after Fed minutes showed the central bank remains worried about persistent inflation and signaled the possibility of further rate hikes while stubbornly resilient US economic data – one might say purposefully manipulated for political purposes and boosted by massive deficit spending – challenges the view that central banks rates are peaking.

As of 7:30am ET, S&P futures were up 0.2%, reversing a similar drop earlier in the session. Nasdaq 100 futures also rose 0.2% The USD reversed an earlier gain and trade near session lows, helping commodities catch a bid. Sentiment was hammered around the globe: European stocks slumped for a third day with Spain outperforming on the move lower (UKX -0.3%, SX5E -0.5%, SXXP -0.4%, DAX -0.2%.) while Asian stocks dropped to their lowest level since March amid further signs of weakness in China and mounting concerns over elevated interest rates in the US. Today’s macro/micro focus is on jobless claims, the Leading Index, and AMAT/WMT earnings.

In premarket trading, BAE Systems Plc fell as much as 4.8% in London, its biggest drop in nine months, after it agreed to buy the aerospace division of soda-can giant Ball Corp. for $5.6 billion. Ball climbed as much as 5.5% in US premarket trading. Cisco Systems rose as much as 2.9% in the US premarket, after the maker of networking equipment gave a forecast that helped ease concerns about a sales slowdown. Here are some other notable premarket movers:

- Adobe rose 1.7% in premarket trading on Thursday after BofA Global Research raised the recommendation on the software company’s stock to buy from neutral, saying the company is “emerging as an AI leader.”

- Hawaiian Electric Industries fell as much as 26%, putting shares on track to decline for an eighth straight session amid Wall Street concern over the company’s potential liabilities following the Maui wildfires.

- Walmart gains 1.0% in premarket trading after boosting its net sales and adjusted earnings per share projections for the fiscal year. The retailer also posted stronger-than-expected second-quarter US comparable sales and profit.

In early trading on Thursday, the 30-year Treasury yield rose as much as seven basis points to 4.42%, slightly exceeding last year’s high, and the highest level since 2011. It was below 4% as recently as July 31. The US 10-year yield approached 4.31%; if it closes here it would be the highest since 2008. The equivalent UK yield jumped to a 15-year high, while its German counterpart approached the highest since 2011.

Bond market woes were precipitated after a surprisingly weak 20-year bond sale in Japan priced with the longest yield tail since 1987, reflecting mounting bets the Bank of Japan’s YCC will soon be loosened. It’s also a significant warning sign for global government debt at a time when yields are already at 15-year highs. Soaring JGB yields would put further upward pressure on the rest of the world, and also mean tougher fiscal budget challenges.

The yield on a Bloomberg index for total returns on global sovereign debt rose to 3.3% Wednesday, the highest since August 2008 as sovereign bonds worldwide have handed investors a loss of 1.2% this year, making the asset class the worst performer across Bloomberg’s major debt indexes. Treasuries have been a key driver of the global debt selloff as resilience in the US economy defies expectations that more than five percentage points of Federal Reserve interest-rate hikes would bring on a recession. Officials at the last policy meeting remained concerned that inflation would fail to recede and that further rate increases would be needed, minutes of the meeting showed.

“Recent data has been firmer, fueling expectations that central banks have a little more work to do,” said Prashant Newnaha, a macro strategist at TD Securities Inc. in Singapore. “The current selloff is being led by the longer end, underscoring concerns about supply and liquidity.”

Indeed, while many investors had believed that the Federal Reserve was done raising interest rates, that’s no longer a sure thing after minutes from last meeting suggested officials are considering tighter policy.

As a result, moves across bond markets have been sharp and swift this week. The 10-year Treasury yield rose four basis points to 4.29% on Thursday, approaching the highest level since 2007. In the UK, equivalent maturity gilts touched 4.71%, the highest since the financial crisis of 2008. Japan’s 20-year bond yield surged after a debt auction drew tepid investor demand.

“Markets are taking the prospect of another hike from the Fed increasingly seriously, with futures now pricing in a 45% chance of a further hike by the November meeting,” Deutsche Bank AG strategist Jim Reid wrote. “Investors are adjusting to the fact that rates could remain at a higher level for some time.”

Meanwhile, China also continued to weigh on sentiment. According to Bloomberg, the picture emerging from property agents and private data providers suggest the slump in the real estate market may be worse than official reports show. These figures show existing-home prices falling at least 15% in prime neighborhoods of major metropolitan areas like Shanghai and Shenzhen. China also ramped up its efforts to stem losses in its currency on Thursday by offering the most forceful guidance since October through its daily reference rate for the managed currency. The offshore yuan slipped against the greenback.

“Equity markets are currently faced with two headwinds — first, real rates are surging again, as the US economy is showing numbers consistent with an economic recovery,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “Second, China is starting to emit dire signals that must remind investors of the awful summer 2015, with a troubled housing market and shadow banking system.”

European stocks were set to fall for the third straight session: the Stoxx 600 is down 0.4% with the industrial, construction and travel sectors leading declines while banks and energy were the bright spots. Here are the biggest European movers Thursday:

- Adyen plunges a record 27% after the payment firm’s processing volume, revenue growth and profitability all came in lower than estimates. The misses fueled analyst concerns over competition

- BAE Systems declines as much as 4.9% after the London-based defense giant agreed to buy Ball Corp.’s aerospace division for $5.6 billion. Analysts said the deal is strategic but expensive

- Nibe falls as much as 12% after the Swedish heat-pump manufacturer said demand for its products is faltering in Europe as governments discuss subsidies for the energy-efficient heating solution

- Coloplast declines as much as 6.9% after the Danish wound and continence care firm reported a disappointing 3Q earnings, with analysts attributing the miss to inflationary effects in its Wound care division

- GN Store Nord shares drop as much as 14% and erasing YTD gains after cutting guidance for its Audio division. The new outlook will lead to high single-digit downgrades to consensus estimates

- Geberit drops as much as 5.4% after the building materials firm reported Ebitda and sales below estimates. The results represent a “sizeable” miss and there’ll be “heavy scrutiny,” Jefferies says

- Aegon falls as much as 5.2% on the back of earnings. First half-year headline group solvency ratio missed consensus expectations, even as the Dutch insurer posted better operating capital generation

- Tremor International falls as much as 34% in their biggest one-day drop in more than four years after the advertising technology firm reported lower-than-expected 2Q Ebitda and cut its full-year revenue

- Calliditas Therapeutics falls as much as 14%, the most since May, after the Swedish pharmaceutical firm published 1H earnings, which included a trimmed outlook for net sales for its key drug Tarpeyo

- Philips gains as much as 5.1% in Amsterdam after Dutch financial daily Het Financieele Dagblad reports details of Goldman Sachs’ involvement in a stake purchase by Exor

- FLSmidth gains as much as 7.6% after investment firm Altor announced it would be increasing its stake in the Danish cement-and-mining services firm to 14.9% by buying 2.21m at an 11% premium

- ITM Power rises as much as 5.8% after the clean-fuel company reported FY results and said it’s making good strategic progress. Its simplified electrolyser product offering is encouraging, Morgan Stanley said

Asian stocks dropped to their lowest level since March amid further signs of weakness in China and mounting concerns over elevated interest rates in the US. The MSCI Asia Pacific Index fell as much as 1.6% on Thursday, set for a fifth day of declines, led by health-care and industrial shares. Pessimism is deepening as investors see no easy fix to the Chinese economy’s ailments given a drumbeat of dour corporate and macro news. Meanwhile, steps taken by policymakers so far have failed to boost sentiment as traders call for more forceful measures.

Most regional markets were down, led by Japan, while Chinese and Hong Kong shares pared earlier losses on dip buying.

- Hang Seng and Shanghai Comp were pressured at the open which saw the Hong Kong benchmark enter bear market territory after declining more than 20% from its January high amid earnings-related disappointment following results from Tencent and JD.com, although Chinese markets then recovered most of the earlier losses following another firm liquidity injection by the central bank and recent economic pledges by Premier Li.

- Nikkei 225 declined after soft data releases including the miss on machinery orders and although the declines in exports and imports weren’t as bad as feared, exports printed in contraction territory for the first time in 29 months.

- ASX 200 retreated as participants digested a slew of earnings releases and disappointing jobs data which showed a surprise contraction in the headline employment change and a larger-than-expected uptick in the unemployment rate.

In FX, the Bloomberg Dollar Index was up 0.1%. The Aussie is the weakest of the G-10 currencies, falling 0.4% versus the greenback after unemployment rose more than expected. The krone rose briefly before fading after the Norges Bank raised rates and pointed to another increase in September.

As noted above, Treasuries are lower, with US 10-year yields rising another 4bps to 4.30% as yields across the long-end of the curve continue to cheapen, with the 30-year rising through 4.42% and onto highest since 2011. Subsequently the curve continues to steepen with 5s30s spread back to re-testing positive. US yields cheaper by 3bp to 7bp from belly out to long-end of the curve with front-end outperforming and marginally richer on the day; spreads steeper with 2s10s, 5s30s widening 5.7bp and 4.5bp on the day with 2s10s steepest since May 25. Similar bear steepening moves seen across core European rates. Bunds and gilts are also in the red with 10-year borrowing costs in Germany and the UK rising by 4bps and 3bps respectively.

In commodities, crude futures advance, with WTI rising 0.2%. Spot gold adds 0.1%.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, the Philadelphia Fed’s business outlook for August, and the Conference Board’s Leading Index for July. Otherwise, earnings releases include Walmart and Applied Materials.

Market Snapshot

- S&P 500 futures up 0.2% to 4,427.75

- MXAP down 0.4% to 158.71

- MXAPJ down 0.4% to 501.02

- Nikkei down 0.4% to 31,626.00

- Topix down 0.3% to 2,253.06

- Hang Seng Index little changed at 18,326.63

- Shanghai Composite up 0.4% to 3,163.74

- Sensex down 0.6% to 65,156.28

- Australia S&P/ASX 200 down 0.7% to 7,146.00

- Kospi down 0.2% to 2,519.85

- STOXX Europe 600 down 0.3% to 453.96

- German 10Y yield little changed at 2.68%

- Euro little changed at $1.0876

- Brent Futures up 0.3% to $83.74/bbl

- Brent Futures up 0.3% to $83.74/bbl

- Gold spot up 0.2% to $1,895.65

- U.S. Dollar Index little changed at 103.44

Top Overnight News from Bloomberg

- Global yields for government bonds extended their climb to the highest levels since 2008 as resilient economic data dashed investor optimism that central banks will soon halt or start reversing interest-rate hikes.

- China ramped up its efforts to stem losses in the yuan by offering the most forceful guidance since October through its daily reference rate for the managed currency.

- China’s top leaders pledged to expand domestic consumption and support the private sector without detailing any new stimulus measures, the latest in a series of rhetorical attempts to boost confidence in the economy as markets sink and growth disappoints.

- Norway’s central bank raised borrowing costs to the highest level since the 2008 financial crisis and signaled it still plans another quarter-point hike in the current tightening cycle.

- UK government bonds slid to send benchmark yields to the highest since the financial crisis, on concerns major central banks will continue to raise interest rates to quell inflation.

- Australia’s unemployment rate rose more than expected in July as the economy surprisingly shed jobs, signaling the labor market may be approaching a turning point and sending the currency lower.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly suffered another day of selling and followed suit to the losses on Wall St as yields continued to edge higher after the FOMC Minutes noted most officials saw significant upside risks to inflation which could require further tightening, while participants also reflected on several weak data releases from the region. ASX 200 retreated as participants digested a slew of earnings releases and disappointing jobs data which showed a surprise contraction in the headline employment change and a larger-than-expected uptick in the unemployment rate. Nikkei 225 declined after soft data releases including the miss on machinery orders and although the declines in exports and imports weren’t as bad as feared, exports printed in contraction territory for the first time in 29 months. Hang Seng and Shanghai Comp were pressured at the open which saw the Hong Kong benchmark enter bear market territory after declining more than 20% from its January high amid earnings-related disappointment following results from Tencent and JD.com, although Chinese markets then recovered most of the earlier losses following another firm liquidity injection by the central bank and recent economic pledges by Premier Li.

Top Asian News

- China reportedly told state banks to escalate Yuan intervention this week, according to Bloomberg sources.

- PBoC said it will keep the Yuan rate basically stable, will keep liquidity reasonably ample, prudent policy will be precise and forceful, and will resolutely prevent over-adjustment risks of CNY exchange rate.

- China shadow banking Co. Zhongzhi plans a debt restructuring and hired KPMG, while it is seeking strategic investors, according to sources cited by Reuters.

European bourses trade on the backfoot after succumbing to the selling pressure seen Stateside and during APAC trade, while macro newsflow has been light. Sectors are mostly lower with Industrial Goods & Services names bottom of the pile amid losses in BAE Systems (BA/ LN) after the Co. confirmed the acquisition of the Ball Aerospace business from Ball Corporation (BALL) for USD 5.55bln in cash. Elsewhere, other laggards include Travel & Leisure and Construction & Materials, whilst to the upside. Stateside, equity futures are flat/modestly firmer following risk-off trade seen at yesterday’s close with the FOMC Minutes unable to cap the negativity.

Top European News

- Norges Bank hiked its Key Policy Rate by 25bps as expected to 4.00%, and sees another hike in September. The future policy rate path will depend on economic developments. If the economy evolves as currently anticipated, the policy rate will be raised further in September. Activity in the Norwegian economy remains high, and the labour market is tight. Consumer price inflation has edged down but remains high and markedly above the target. Underlying inflation has remained elevated. If the NOK proves to be weaker than previously projected or pressures in the economy persist, a higher policy rate than signalled in June may be needed to bring down inflation. If there is a more pronounced slowdown in the Norwegian economy or inflation declines more rapidly, the policy rate may be lower than envisaged in June.

- ECB’s Kazaks said it is good news that inflation is coming down, needs to see the new ECB forecasts before deciding on hikes; any additional hikes would be small, according to Bloomberg.

- Spain’s Socialist Party reaches agreement in principle with Catalan Separatist party Junts to elect lower House Speaker, via ABC Newspaper.

FX

- DXY faded from best levels after extending gains on the back of broad risk aversion and further weakness in EM currencies rather than independent factors.

- AUD and NOK are at opposite ends of the G10 spectrum, the Aussie suffered a double whammy as the labour market report revealed an unexpected fall in employment and firmer than forecast unemployment rate. Conversely, the Norwegian Krona saw enough in the Norges Bank’s accompanying statement to test bids/support around 11.5000 vs the Euro.

- PBoC set USD/CNY mid-point at 7.2076 vs exp. 7.3047 (prev. 7.1986)

- China’s major state-owned banks’ branches were seen selling dollars to buy yuan in the offshore FX market during London and New York trading hours this week and were also seen selling dollars to buy yuan in the onshore FX market, according to sources cited by Reuters.

- RBI was likely selling dollars via state-run banks, according to traders cited by Reuters.

Fixed Income

- Debt futures have been choppy in the aftermath of a risk-off APAC session and with some follow-through from the FOMC minutes that featured a hawkish line, but in the context of recent sessions price action has been somewhat restrained.

- Bunds, Gilts and the T-note all remain in negative territory between 130.89-40, 92.00-91.61 and 109.20+/109-05+ respective bounds, though inside current w-t-d ranges awaiting the next major market-mover or catalyst.

- France sold EUR 8.44bln vs. Exp. EUR 7.5-8.5bln 2.50% 2026, 2.75% 2029, 1.50% 2031 OAT.

Commodities

- WTI and Brent front-month futures tilted higher this morning following APAC consolidation, with little in the way of fresh newsflow to drive price action.

- Spot gold is flat intraday under the USD 1,900/oz mark after relinquishing the level amid the recent Dollar strength, with the yellow metal pulling further away from its 200 DMA (1,905.86/oz).

- Base metals are holding modest gains with some impetus seen from the aforementioned revivals of Chinese sentiment towards the end of their trading day.

- Woodside Energy (WDS AT) workers will reportedly vote tonight on industrial action at LNG platforms, according to CNBC TV citing sources.

- US reportedly plans to escalate its dispute with Mexico over genetically modified corn, according to Bloomberg sources.

- NHC said Hilary forecast to rapidly intensify and become a Hurricane very soon, according to Reuters.

Geopolitics

- US plan new tariffs on food-can metal from China, Germany and Canada, according to WSJ; Levies announced in response to dumping allegations could raise canned food prices, industry group saysChinese products would be subject to the highest tariffs of the three countries, a levy of 122.52% o their import value.

- Russian Ambassador to the US said issues of prisoner swaps are being solved by relevant bodies of Russia and the US, while he added that this channel has proved to be effective, according to Reuter.

- South Korean lawmaker said there is a possibility for another spy satellite launch in North Korea between the end of August and early September, while there are signs that North Korea is preparing an ICBM launch, citing the spy agency.

- North Korea and Russia agreed to military cooperation during a recent meeting between North Korean leader Kim and Russia’s Defence Minister, according to Yonhap.

US Event Calendar

- 08:30: Aug. Initial Jobless Claims, est. 240,000, prior 248,000

- 08:30: Aug. Continuing Claims, est. 1.7m, prior 1.68m

- 08:30: Aug. Philadelphia Fed Business Outl, est. -10.2, prior -13.5

- 10:00: July Leading Index, est. -0.4%, prior -0.7%

DB’s Jim Reid concludes the overnight wrap

Markets have witnessed some big milestones over the last 24 hours, as robust US data and fresh signs of inflationary pressures sent global yields up to new highs. Most notably, yesterday saw the 10yr US Treasury yield rise another +3.9bps to 4.25%, which is its highest closing level since 2008, and this morning it’s up a further +3.6bps to 4.29%. That comes as markets are taking the prospect of another hike from the Fed increasingly seriously, with futures now pricing in a 45% chance of a further hike by the November meeting. But as well as the upcoming decisions, it’s clear that investors are adjusting to the fact that rates could remain at a higher level for some time. Indeed, futures for the rate at the Fed’s December 2024 meeting are now at their highest level so far this cycle, at 4.34%.

There were several catalysts behind the latest moves, but an important one was some further upside surprises in US data that led to growing optimism about the state of the economy. In particular, July’s industrial production grew by +1.0% (vs. +0.3% expected), and there was a very strong monthly growth rate of +5.2% for motor vehicles and parts. As a result, the Atlanta Fed’s GDPNow model moved to forecast that Q3 growth would come in at an annualised pace of +5.8%, and our own US economists have upgraded their Q3 growth forecast to an annualised +3.1% (link here). But all the good news on the economy wasn’t entirely positive for markets, as it helped cement investors’ conviction that tight monetary policy was likely to persist for some time.

That view was then given added support by the latest Fed minutes from the July meeting, which confirmed that the FOMC still had a tightening bias. For instance, it said that most participants “continued to see significant upside risks to inflation, which could require further tightening of monetary policy”. The minutes also echoed Chair Powell’s focus on growth and labour markets, and whether “product and labour markets were reaching a better balance between demand and supply”. So while inflation has been more encouraging of late, activity data that’s still strong ought to keep the Fed’s hawkish bias as we move towards the September meeting. According to the minutes, a “couple” of members favoured keeping rates unchanged in July, which is effectively in line with the June dot plot that had two dots for no further hikes in 2023.

The Fed minutes added some impetus to the Treasury sell-off, with several new milestones across the curve. As mentioned at the top, the 10yr Treasury yield (+3.9bps) moved higher for a 5th consecutive session to close at 4.25%, its highest level since 2008. And it was real yields that led the increase, with the 10yr real yield (+4.9bps) closing at a post-2009 high of 1.93%, whilst the 2yr real yield (+5.5bps) hit its own post-2009 high of 3.15%. There were also growing signs that higher yields were filtering through to the real economy, as MBA data showed that the average 30yr fixed rate mortgage reached 7.16% last week, in line with its previous peak last October.

With the prospect of higher rates for longer continuing to loom ahead of Jackson Hole next week, equities put in another downbeat performance. The S&P 500 shed another -0.76% to hit a 5-week low, and the NASDAQ (-1.15x%) saw an even larger decline as it hit a 7-week low. The megacap tech stocks were among the worst performers yesterday, with the FANG+ index (-1.69%) posting a sizeable decline. Over in Europe, the equity decline was more modest, with the STOXX 600 down -0.06% to its own 5-week low.

That tone has continued overnight as well, with the major equity indices in Asia posting modest losses for the most part. That includes the KOSPI (-0.39%), the Nikkei (-0.32%), the Hang Seng (-0.12%) and the CSI 300 (-0.05%), although the Shanghai Comp is up +0.01%. Indeed at one point earlier in the session this morning, the Hang Seng was on track for bear market territory, having shed more than 20% since its recent peak in January, although it’s since pared back those losses. The offshore Yuan has also continued to weaken overnight, and now stands at 7.340 per US dollar, which is almost at its recent low from early November when it closed at 7.343.

Elsewhere in markets yesterday, UK gilts were the biggest underperformer after the latest CPI print for July pointed to resilient price pressures. It’s true that the headline CPI print fell to +6.8%, but it was still a tenth above expectations and the core CPI rate also remained at +6.9% (vs. +6.8% expected). In addition, even as the headline measure has been coming down, the latest print still leaves the UK with the highest inflation rate in the G7, whilst the closely-watched services CPI rate actually moved up two-tenths to +7.4%.

That UK release follows some very strong wage growth data earlier in the week, and meant that investors continued to price in a more aggressive path of rate hikes from the BoE over the months ahead. For instance, overnight index swaps are now pricing in a 30% likelihood of a larger 50bps move at the next meeting, as well as a terminal policy rate above 6%. Gilt yields also moved higher across the curve, with the 10yr yield up +5.7bps to 4.64%, whilst the 10yr real yield (+3.9bps) hit its highest level since last year’s mini-budget turmoil at 0.86%. However, there was a stronger performance elsewhere in Europe, with yields on 10yr bunds (-2.5bps), OATs (-2.3bps) and BTPs (-0.4bps) all moving lower.

Yesterday’s risk-off tone was also evident among commodities. For instance, oil prices fell by more than 1% for the second day in a row, with Brent down -1.70% to $83.45/bl and WTI down -1.99% to $79.38/bl. Meanwhile, Bloomberg’s industrials metals index fell to its lowest since February 2021, having declined by -8.59% since the end of July.

Lastly, we had a few other data releases yesterday, including on US housing. That showed housing starts up to an annualised pace of 1.452m in July (vs. 1.450m expected), and building permits up to an annualised 1.442m (vs. 1.463m expected). Meanwhile in the Euro Area, industrial production grew by +0.5% in June (vs. unch expected), though our economists note that this outperformance versus expectations came due to the distorted data from Ireland.

To the day ahead now, and data releases from the US include the weekly initial jobless claims, the Philadelphia Fed’s business outlook for August, and the Conference Board’s Leading Index for July. Otherwise, earnings releases include Walmart and Applied Materials.

Tyler Durden

Thu, 08/17/2023 – 08:05

nasdaq

asx

ax

gold