Uncategorized

Futures Slide After Tech Wreck Goes 0 For 5

Futures Slide After Tech Wreck Goes 0 For 5

With the core of tech earnings season now behind us, FAAMG goes 0 for 5 on earnings as lackluster…

Futures Slide After Tech Wreck Goes 0 For 5

With the core of tech earnings season now behind us, FAAMG goes 0 for 5 on earnings as lackluster earnings from the group this week dampened sentiment and underscored the impact of the Fed’s tightening regime. While macro data didn’t help the cause – the GDP report showed the US economy rebounded after two quarterly contractions (all driven by net exports)and briefly assuaged concerns of an imminent recession, consumer spending remains under pressure because of persistent inflation – after the bell, AMZN out with an extremely disappointing miss which sent the stock down as much as 21%, followed by AAPL with a low quality beat driven by As such, Goldman’s Michael Nocerino writes that this morning is going to be harder to compartmentalize these prints (like we have with MSFT, GOOG, META) given AMZN and AAPL make up 10% weighting of the S&P.

And sure enough, the Nasdaq 100 was poised to extend a $675 billion wipeout of the past two days as disappointing earnings prompted a liquidation spree amid the deteriorating profit outlook. Nasdaq 100 futures slumped 1% by 7:30 a.m. in New York, set to trade lower for a third day as reports from Amazon.com and Apple hurt sentiment. Contracts on the S&P 500 were down 0.4%, having dropped as much as 1% earlier. And yet, despite recent weakness, the S&P 500 is set for a second week of gains for the first time since August, amid growing speculation the Fed will be forced to pivot soon. The 10-year benchmark Treasury yield surpassed 4% as a rally in government bonds began to fizzle. Government bonds this week were buoyed by hopes that policymakers are preparing a downshift in aggressive rate hikes amid softer economic data. The dollar collapse, which defined much of this week amid speculation of coordinated intervention, has also started to crack and the dollar index is sharply higher today after the yen tumbled following the BOJ’s announcement to maintain YCC and not change monetary policy for a long time, despite some half-baked rumors to the contrary.

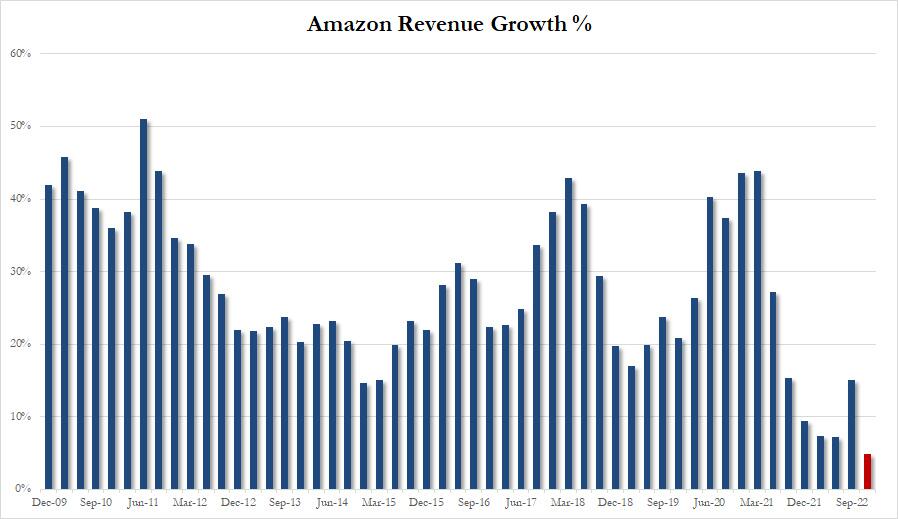

Amazon shares plunged 14% in premarket after the tech giant projected its slowest holiday quarter growth in history.

Meanwhile, Apple edged higher after posting weaker-than-expected iPhone and services sales for its latest quarter, marring an otherwise upbeat report. The combination of weaker earnings and higher interest rates is making technology stocks look increasingly unappealing to investors. The sector could face more pressure ahead as valuations continue to look elevated, Mark Haefele, chief investment officer at UBS Global Wealth Management, said in a note.

“There are now two stock markets — it’s increasingly important to look at the equal-weighted S&P as mega-cap tech (which dominates the normal SPX) enters an extended period of underperformance,” Vital Knowledge analyst Adam Crisafulli wrote in a note. “We continue to think tech is entering a period similar to the ‘99/’00 dotcom boom and bust.”

“These tech results will likely drive broader sentiment down,” said Columbia Threadneedle’s global equity portfolio manager Natasha Ebtehadj on Bloomberg TV. “Apart from tech, other earnings have held up relatively well so hopefully that will provide some support to markets.”

“We are starting to see some companies’ bleeding in terms of forecasts and unfortunately we’re starting to see the big caps in the market disappointing,” Banque Syz CIO Charles-Henry Monchau said in an interview with Bloomberg TV. “Earnings for us is still a headwind.”

Besides the tech rout, bank stocks were also lower in premarket trading Friday, putting them on track to snap a five-day winning streak. In corporate news, Binance, the world’s largest cryptocurrency exchange, confirmed that it’s an equity investor in Elon Musk’s $44 billion acquisition of Twitter. Despite – or perhaps thanks to – Marko Kolanovic’ latest ringing endorsement of all things China, Hong Kong-listed peers plummeting and on course to end a three-day winning streak. Here are some other premarket movers:

- Intel rises as much as 5.6% in premarket trading on Friday, after the chipmaker said it was aggressively addressing costs, with a target of $3 billion of reductions in 2023. The chipmaker, and fellow tech companies like Amazon and Meta, are being pressed to wind back spending after years of bulking up.

- Pinterest jumped almost 10% in US premarket trading, as the social media company’s results offered analysts respite amid the “wreckage” in the advertising sector demonstrated this week by disappointing earnings from Meta Platforms and Alphabet. Analysts raised their price targets on the stock following Pinterest’s revenue beat and outlook for the fourth-quarter, despite threats from a darkening macroeconomic environment.

- US cloud stocks could come under pressure on Friday, after Amazon reported sales for its AWS cloud unit that missed analyst estimates, stoking worries that other providers could also see weakness as enterprise customers pull back on spending.

- Core Scientific shares slide 4.9% in US premarket trading, after the bitcoin miner slumped 78% on Thursday in its worst day on record after saying it may seek bankruptcy protection. Barclays downgraded the stock to equal- weight from overweight on solvency worries.

- Gilead Sciences shares gain 4.8% in premarket trading after the biopharmaceutical company boosted its guidance for adjusted earnings per share and its 3Q earnings came ahead of analyst estimates. Analysts noted the strong performances from Gilead’s core HIV and oncology businesses, as well as the company’s Covid drug Veklury.

- Mullen Automotive drops as much 10% in US premarket trading, with shares in the electric car startup set to ease further after surging more than 40% this week amid heavy mentions on social media and positive sentiment around its I-GO electric vehicle.

In Europe, the Stoxx 50 fell 1.1% with France’s CAC 40 outperforming peers, dropping 0.7%, FTSE MIB lags, dropping 1.4%. Miners, tech and real estate are the worst performing sectors in Europe. Here are some of the biggest European movers today:

- OMV shares rise as much as 10%, hitting the highest since July as analysts say 3Q results looks robust operationally.

- Kongsberg gains as much as 7.4% after it reported Ebitda for the third quarter that beat the average analyst estimate.

- Danske Bank A/S shares rise as much as 5.5%, the most in more than a decade after the lender said it’s close to resolving its money- laundering scandal at an estimated cost of 15.5 billion kroner ($2.1 billion).

- Electrolux rises as much as 5.5%, flipping from earlier losses of as much as 5.9%, after the Swedish appliance maker published 3Q results weighed down by poor sales in North America, but offset by a new cost-savings package that includes cutting up to 5,000 staff.

- Credit Suisse shares gained as much as 4.7% in Zurich after a record one-day drop on Thursday, when it slumped 19% following the presentation of its new strategic plan including a capital raise and a carve out of its investment banking business.

- Natwest fell as much as 9.4% after reporting costs that were higher than expected in the latest hit to the sector as a mortgage crisis looms and a recession looks likely.

- Universal Music shares drop as much as 8.5%, the most since June, with analysts saying there were some “weak spots” in the record company’s results and positives around its outlook may already have been priced in.

- Valeo shares fall as much as 8% with analysts flagging underperformance for the auto-parts firm.

- STMicro shares fall as much as 6.6%, the most since May, after the chipmaker guided fourth-quarter revenue slightly below average analyst estimates.

Earlier in the session, Asian equities were poised for a third weekly drop as Chinese shares slumped, offsetting an earlier reprieve from declines in US Treasury yields and the dollar. The MSCI Asia Pacific Index fell as much as 1.8% on Friday, on track to end the week with losses. Chinese stocks traded in Hong Kong plunged again to 2008 lows, snapping a three-day rally, after the party congress dashed hopes for more market-friendly policies. Read: China Stocks in Worst Ever Post-Congress Rout as Gloom Persists President Xi Jinping’s tighter grip on China has “caused some investors to finally throw in the towel, with the most dramatic impact on the technology stocks,” saidJonathan Pines, head of Asia ex-Japan at Federated Hermes in a note. Meanwhile, Japanese stocks edged lower after the Bank of Japan stood by its ultra-low interest

rates. Singapore bucked the region’s trend to rise more than 1%. Friday marked the busiest day for Asia earnings this results season. Chinese automaker BYD Co., Industrial & Commercial Bank of China Ltd. — the world’s largest bank by assets — and Japanese electronics firm Keyence Corp. are among the 239 MSCI Asia Pacific Index members that reported earnings. Stocks have rebounded this week after a slew of dovish signals from central bankers revived hopes that the pace of policy tightening will slow. Traders will watch for more clues at the Federal Reserve’s meeting next week, where it is expected to deliver a fourth-straight 75 basis point hike.

Japanese equities closed lower after the Bank of Japan maintained its easy monetary policy. Stocks had opened lower amid concern over tech earnings at home and in the US, but were trading little changed around midday before the BOJ’s announcement. The Topix fell 0.3% to close at 1,899.05, while the Nikkei declined 0.9% to 27,105.20. The yen was trading around 146.4 per dollar, swinging between gains and losses. Volume on the Prime market jumped to 5.77 trillion yen, the highest since the market reorganization, as passive funds adjusted holdings on the latest rebalancing of the Topix. Hoya Corp. contributed the most to the Topix decline, decreasing 4.4% after disappointing earnings. Out of 2,166 stocks in the index, 641 rose and 1,448 fell, while 77 were unchanged. The BOJ again maintained its ultra-low rates even as other central banks are tightening. While this divergence had driven the yen’s weakness this year, the currency has rallied almost 4% since last week, from a three-decade low that triggered suspected intervention from Japan. “If the BOJ is lucky, the dollar will weaken from current levels, and the depreciation in the yen will remain at a reasonable level,” Ipek Ozkardeskaya, a senior analyst at Swissquote Group Holdings, wrote in a note. “Otherwise, we could see the dollar-yen spike above the 150 level despite the BOJ’s direct interventions, which do nothing more than burning money.”

Australian stocks also fell: the S&P/ASX 200 index dropped 0.9% to close at 6,785.70, ending a four-day winning streak, dragged by iron ore miners including BHP Group after the steelmaking raw material extended its rout to the lowest in more than two years. Materials, technology and healthcare sectors led the benchmark index’s drop on Friday. Still, the index made a weekly gain of 1.6%. In New Zealand, the S&P/NZX 50 index climbed 0.3% to 11,129.53

Stocks in India advanced for the second consecutive week, moving closer to their record levels seen last year, helped by a rally in financial companies amid robust earnings. The S&P BSE Sensex Index rose 0.3% to 59,959.85 in Mumbai, its highest level since Sept. 14. The NSE Nifty 50 Index advanced by an equal measure. For the week, the indexes have risen more than 1% and are about 3% short of their record levels seen a year ago. Twelve of the 19 sector sub-gauges compiled by BSE Ltd. declined, led by metal companies. For the week, auto firms were among best performers as vehicle sales picked-up during the ongoing festive season. Corporate earnings for September quarter have been supportive of the rally in Indian markets. Out of the 23 Nifty companies, which have so far reported earnings, 16 have either matched or beat the consensus view, while five missed. Top lenders including ICICI Bank and Axis Bank, have reported higher-than-expected profits, helped by rising credit demand.

In FX, the Bloomberg Dollar Spot Index extended yesterday’s bounce from a five-week low as the greenback advanced 0.4$ versus all of its Group-of-10 peers ahead of US inflation data. EUR and DKK are the strongest performers in G-10 FX, JPY and AUD underperform; yen trades at ~147 per dollar.

- The yen was the worst G-10 performer, snapping a three-day advance, as the Bank of Japan stood by its ultra-low interest rates amid fresh government support, pushing back against lingering market speculation it will adjust policy as it continues to predict inflation will cool below 2% next year

- Australia’s dollar was also among the worst performers as commodity prices slumped. The nation’s sovereign bonds rallied as it caught up with events in Europe and the US on Thursday

- The euro fell for a second day on the back of broad-based US dollar strength. European bonds extended a drop after French inflation data for October came in hotter than expected. Front-end bund yields rose by around 10bps, while the long end added around 7bps. BTPs added 10-12 bps across the curve.

In rates, the Treasury curve bear-flattened, pushing yields 2-7bps higher as yields trade near session highs after erasing late-Thursday gains that coincided with Amazon’s after-market plunge. Treasuries track bigger losses in bunds, where German curve aggressively bear-flattens as ECB hike premium is added into front-end. Economic data are focal point of US session, including personal income/spending inflation gauge and University of Michigan sentiment. US yields are cheaper by as much as 10bp in belly of the curve, flattening 5s30s by 7bp to as low as -6.2bp; 10-year yields around 4%, cheaper by 8bp on the day with bunds cheaper by additional 6bp in the sector. German curve bear-flattens as 10-year yields rise 14bps to 2.1%; 2s10s, 5s30s spreads are tighter by 2bp and 3bp on the day as front- end and belly yields are cheaper by 17bp on outright basis. Italian BTP spread widens to Germany; Italy inflation hit an all-time high of 12.8% in October.

In commodities, oil pared its weekly gain as investors shied away from risky assets on a dimming outlook for China and the wider global economy. West Texas Intermediate slid below $88 a barrel. Moving to metals, the complex is once again under USD-induced pressure with precious metals unable to derive any substantial allure from their traditional haven status; base metals hit on sentiment, particularly APAC weakness in China. Spot gold falls roughly $12 to trade near $1,651/oz.

Bitcoin is under modest pressure though resides in narrow ranges and despite the DXY reclaiming 111.00, Bitcoin still holds onto the USD 20k handle.

Looking ahead, today’s data line up in the US will include Q3 employment cost index, which as Nikileaks just informed us…

The bottom line: while the Fed isn’t data-point dependent and the decision for next week of 75 basis points seems unlikely to change, another uncomfortably high ECI reading might argue for a somewhat higher terminal rate and could muddy the debate over slowing the pace in Dec.

— Nick Timiraos (@NickTimiraos) October 28, 2022

… will be closely watched by the Fed so a big beat here and futures will tumble even more. We also get, September personal income, personal spending, PCE deflator and pending home sales. In Europe, Germany and France will release Q3 GDP and October CPI figures, with the latter also due for Italy. Other indicators will include consumer spending and PPI for France, PPI and hourly wages for Italy and economic and industrial confidence for the Eurozone. The earnings list will be lighter than in previous days but will feature key commodity companies like Exxon Mobil, Chevron, Equinor and Eni. Other notable reporters will include AbbVie, NextEra Energy, Sanofi, Porsche, Airbus, Volkswagen, Colgate-Palmolive, BBVA and LyondellBasell.

Market Snapshot

- S&P 500 futures down 0.8% to 3,790.50

- STOXX Europe 600 down 0.6% to 406.72

- MXAP down 1.7% to 135.55

- MXAPJ down 1.9% to 432.30

- Nikkei down 0.9% to 27,105.20

- Topix down 0.3% to 1,899.05

- Hang Seng Index down 3.7% to 14,863.06

- Shanghai Composite down 2.2% to 2,915.93

- Sensex little changed at 59,792.78

- Australia S&P/ASX 200 down 0.9% to 6,785.72

- Kospi down 0.9% to 2,268.40

- Brent Futures down 0.7% to $96.30/bbl

- Gold spot down 0.7% to $1,651.18

- U.S. Dollar Index up 0.31% to 110.93

- German 10Y yield up 4% to 2.04%

- Euro down 0.2% to $0.9946

Top Overnight News from Bloomberg

- As China’s hovers near the weak end of a daily 2% trading band against the dollar, the specter of extreme measures — however unlikely — is growing. Already, there are signs that China is intervening in foreign-exchange markets, like Japan has done. A one-time revaluation and restricting the yuan’s range are other major tools

- The ECB’s monetary policy will have to move into restrictive territory to get inflation under control, Governing Council member Peter Kazimir said

- The ECB is under no obligation to repeat the 75 basis-point interest-rate increases enacted at the last two meetings, Governing Council member Francois Villeroy de Galhau said

- The ECB will continue to lift borrowing costs as it steps up its battle against record euro-area inflation, and remain flexible about the magnitude of individual steps, according to Governing Council member Bostjan Vasle

- The ECB needs to deliver a “substantial” increase in interest rates at its final meeting of the year in December, despite a strong likelihood of a technical recession in the euro area, according to Governing Council member Gediminas Simkus

- Hopes that the euro zone can stave off a recession got a boost as Germany defied expectations by reporting another quarter of economic growth, though momentum slowed dramatically in France and Spain

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mostly lower but off worst levels following a mixed lead from the US. ASX 200 was pressured by its IT sector following the Meta-induced losses seen on Wall Street. Nikkei 225 drifted off worst levels heading into the BoJ announcement but saw little action on the return from lunch break after the BoJ maintained its policy unchanged whilst upping its inflation forecasts across the board. KOSPI conformed to the broader risk tone, although losses were shallower than peers. Hang Seng and Shanghai Comp opened lower with the tech sector underperforming after the downbeat sectoral lead from the US, whilst NY Times reported that the Biden administration is weighing further controls on Chinese technology. Agricultural Bank of China (1288 HK) Q3 2022 (CNY): Net 68.5bln, NIM 1.96%, NPL ration 1.40%. ICBC (1398 HK) 9M 2022 (CNY): net profit 265.82bln, NPL 1.4% at end-Sept.

Top Asian News

- China Names Beijing Mayor Chen Jining As Shanghai Party Boss

- BOJ Keeps Ultra-Low Rates as Team Japan Sticks to Policy Path

- BOJ Changes Bond Purchase Plan for First Time During a Quarter

- Russia Export Windfall Finds Sanctions Haven in Yuan, Quasi-Bank

- Iron Ore on Track for Longest Run of Weekly Losses Since 2014

European bourses are pressured across the board, Euro Stoxx 50 -0.9%, deriving direction from downbeat APAC and US after-market trade. Within the region, sectors are predominantly in the red with Tech dented amid US after-market updates while Basic Resources slips after Glencore’s downbeat production report. Stateside, the NQ -1.3% is the clear underperformer amid pressure from the below after-market earnings; ES -0.8%, pressured though magnitudes a touch more contained ahead of key US price data. Amazon.com Inc (AMZN) – Q3 2022 (USD): EPS 0.28 (exp. 0.22), Revenue 127.1bln (exp. 127.45bln); Q4 22 revenue view 140-148bln (exp. 155.150bln). AWS: 20.54bln (exp. 21.191bln). Click here for details. CFO said the Co. is preparing for what could be a slower growth period. Co. is being very careful on its hiring and is seeing weakness in Europe relative to the US. -13% in the pre-market. Apple Inc (AAPL) Q4 2022 (USD): EPS 1.29 (exp. 1.27), Revenue 90.15bln (exp. 88.90bln) Q4 product sales: iPhone: 42.63bln (exp. 43.21bln) iPad: 7.17bln (exp. 7.94bln). Mac: 11.51bln (exp. 9.36bln). Click here for details. CFO says total company revenue will decline in Q4; sees nearly 10ppt negative Y/Y impact from FX. +0.5% in the pre-market. Intel Corp (INTC) – Q3 2022 (USD): Adj. EPS 0.59 (exp. 0.32), Revenue 15.3bln (exp. 15.25bln). Click here for details. +4.5% in the pre-market

Top European News

- European Stocks Fall Amid Earnings Flurry as Tech, Miners Drop

- UK Lenders Face Biggest Mortgage Test Since Financial Crisis

- Appliance Maker Electrolux to Cut Up to 8% of 50,000 Staff

- Saab Ramping Up Capacity Ahead of Sweden’s NATO Membership

- Porsche’s Soaring Profit Can’t Drive Away Year-End Concerns

FX

- DXY extends recovery gains to probe 111.000 and this time thanks in large part to the Yen as BoJ sticks to ultra-accommodation, dovish guidance and passive role in terms of intervention; USD/JPY eyes 148.00 from around 146.00 at one stage and near 145.00 yesterday

- Aussie and Kiwi rattled by risk aversion and their US rival’s revival, AUD/USD just over 0.6400 and NZD/USD under 0.5800

- Euro cushioned by strong inflation data and some hawkish ECB rhetoric, but capped at parity vs the Buck and more hefty option expiries

- Yuan undermined by a weak PBoC fix and losses in Chinese tech stocks on reports of further US controls

- PBoC set USD/CNY mid-point at 7.1698 vs exp. 7.1638 (prev. 7.1570); weakest Yuan fix since Feb 2008.

- China’s CBIRC says those who sell the Yuan now will regret it, via Bloomberg citing a report. China has a resilient economy and its positive long-term trend will continue.

Fixed Income

- EGBs are under broad pressure as ECB speakers come out in full hawkish force alongside hotter than expected regional CPI data, ex-Spain.

- Specifically, the Bund has been pushed below 139.00 and the accompanying 10yr yield to above 2.10% while BTPs are similarly pressured though the spread vs. Germany has narrowed to around 200bps.

- Gilts are bucking the trend somewhat and retain a slight positive bias, with attention turning to next week’s BoE where the magnitude is centered around 75bp vs 100bp+ in recent weeks.

- Stateside, USTs are in-fitting with EGBs ahead of their own price metrics via PCE Price Index this afternoon, with yields elevated as such though the curve is a touch flatter.

Commodities

- The complex looks set to end the week with another session of relatively limited explicit newsflow and as such participants focus remains on broader macro developments and pricing.

- Currently, the crude benchmarks are pressured by around 1% or just shy of USD 1.00/bbl on the session though are still set to end the week with upside of just over USD 2.00/bbl, at the time of writing.

- Moving to metals, the complex is once again under USD-induced pressure with precious metals unable to derive any substantial allure from their traditional haven status; base metals hit on sentiment, particularly APAC weakness in China.

Central Banks

- BoJ maintained its policy unchanged as expected with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yield at around 0%, via a unanimous vote, whilst also maintaining dovish forward guidance, as expected.

- BoJ Quarterly Outlook Report saw Core CPI upgraded across the board, but the FY23 and FY24 forecasts were below the BoJ’s 2% target, both at 1.6% (upgraded to 1.4% and 1.3% respectively), whilst warning that the risks to prices are skewed to the upside. Real GDP growth was downgraded for FY22 and FY23 but upgraded for FY24. The BoJ said there is a need to watch FX and its impact on the economy. The central bank also said it will make changes to the way it buys ETFs from Dec 1st, the Bank will take now into account the holding cost of each ETFs and select those with the lowest trust fee ratio in making purchases.

- BoJ Governor Kuroda (post-meeting press conference) says must be vigilant to the impact of FX moves; CPI to undershoot 2% from next year; will not hesitate to ease monpol. if needed. Click here for full details.

- BoJ Quarterly Schedule of Outright Purchases of Japanese Government Bonds; to increase frequency of purchases in November.

- ECB’s Simkus says QT discussion in December should be about start dates and amounts, via Reuters.

- ECB’s Villeroy says the ECB will bring inflation back to 2% in 2-3 years; no obligation to raise rates by 75bps at the December meeting.

- ECB’s Kazmir says rates will rise in December and in early 2023, crossing neutral like a ‘runaway train’, must get rates into restrictive territory. A risk that Eurozone inflation will remain higher for longer, and remains above target. Risk of a recession in the Eurozone are growing.

- ECB’s Muller says they must decide on how to gradually cut bond holdings, via Bloomberg; rates will continue to increase in the near term, they are still now and are not restrictive.

Geopolitcs

- US will soon provide additional military assistance to Ukraine, according to the White House spokesperson, US is not seeing any signs of Russia making preparations to use a “dirty bomb”, via CNN.

- Biden administration is weighing further controls on Chinese technology, according to NYT.

- France and Germany “agreed that recent American state subsidy plans represent market-distorting measures that aim to convince companies to shift their production to the US… and that is a problem they want the EU to address.”, according to Politico sources.

- North Korea fired two short-range ballistic missiles that landed outside of Japan’s Exclusive Economic Zone, according to South Korea.

US Event Calendar

- 08:30: 3Q Employment Cost Index, est. 1.2%, prior 1.3%

- 08:30: Sept. Real Personal Spending, est. 0.2%, prior 0.1%

- Sept. Personal Income, est. 0.4%, prior 0.3%

- Sept. Personal Spending, est. 0.4%, prior 0.4%

- Sept. PCE Deflator MoM, est. 0.3%, prior 0.3%

- Sept. PCE Deflator YoY, est. 6.3%, prior 6.2%

- Sept. PCE Core Deflator YoY, est. 5.2%, prior 4.9%

- Sept. PCE Core Deflator MoM, est. 0.5%, prior 0.6%

- 10:00: Sept. Pending Home Sales (MoM), est. -4.0%, prior -2.0%

- Pending Home Sales YoY, prior -22.5%

- 10:00: Oct. U. of Mich. Sentiment, est. 59.6, prior 59.8

- Oct. U. of Mich. Current Conditions, est. 65.0, prior 65.3

- Oct. U. of Mich. Expectations, est. 56.0, prior 56.2

- Oct. U. of Mich. 1 Yr Inflation, est. 5.1%, prior 5.1%

- Oct. U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

DB’s Jim Reid concludes the overnight wrap

I think we can now officially call this the 6th pivot anticipation trade over the last 12 months. What started out as a WSJ Timiraos tweet last Friday, got momentum from weaker housing data, moved onto a dovish BoC, and then reached the ECB yesterday. Although they hiked 75bps, they signalled a more dovish tone than expected. So much so that our economists now think they will hike 50bps in December relative to their previous 75bps forecasts. They still think the terminal rate will hit 3% but the profile is much more uncertain now. Their base case is a further 50bps in February and then two successive 25bps hikes to get to 3%. The BoJ maintained the dovish flavour of the last week, as expected, keeping policy rates unchanged and its yield curve control program in place.

Back to the ECB, to quote DB’s Mark Wall from his review piece “the press conference had elements that leaned dovish”. These included the increased probability of recession, the lagged impact of rapid monetary tightening and the absence of reference to “several” more hikes. Other comments pushed back as too dovish an interpretation, such as the emphasis on uncertainty, the more inflationary wording on wages and the fact that even after this hike the Governing Council was no closer to defining the terminal rate.” There’s lots more in the piece including on all the TLTRO news.

All in all, this further amplified the dovish rates trade since Friday. If only I had a fraction of the power to move global markets as WSJ’s Nick Timiraos. In terms of the highlights yesterday, markets took around 25bps of cuts out of terminal ECB rates to now around 2.6%. This put pressure on the euro (-1.16%) which fell below parity again as 2y yields weakened across major European markets, including Germany (-17.0bps), France (-9.8bps) and Italy (-31.0bps). 10y yields fell as well, with periphery bonds (BTPs -32.1bps) outperforming the ones in Western Europe (Bunds -15.1bps and OATs -18.3bps). In their recap of the meeting (link here) our European rates strategists tied the Italian outperformance to the communications that principles around QT would be pursued in December, and that ahead of any implementation, which was more dovish than what was anticipated going into the meeting. They also note that BTPs outperformed from the generally dovish tone that defined the entire meeting.

So this sets us up very nicely for Powell and the Fed next week. What could have been a bog standard incremental 75bps now becomes a “will they or won’t they” endorse the pivot party? I’d imagine the most dovish Powell could be is to say that December’s decision between 75bps and 50bps will be data dependent. I’m not sure he can go further than that with two CPI and NFP reports in the interim.

This dovish global move this week has taken the headline pressure off a poor week for US tech earnings with Meta falling -24.56% yesterday after the prior night’s results. Last night it was the turn of Apple and Amazon. The former slightly disappointed analysts on weaker iPhone and services revenues and, after flitting between gains and losses, actually managed to finish after-hours trading +0.38% higher on offsetting strength in other business lines including Mac sales. Apple is proving a stand out, however, as the latter was a bit of a shocker with company forecasts for the lucrative holiday period much lower than expected. Shares fell a dramatic -12.98% after hours. If sustained today that would drop it to a market cap of below $1tn. In November last year we were as high as $1.9tn, so quite a fall to say the least. This has left S&P and Nasdaq futures down -0.44% and -0.69% overnight.

Another big macro event yesterday was the release of Q3 GDP in the US and the print came in at +2.6%, above the 2.4% consensus estimate and a strong rebound from -0.6% in Q2. However, the lion’s share of gains in growth came from net exports and demand-related components showed muted growth. In other data releases, a downbeat tone came from a miss on durable goods orders (+0.4% vs +0.6% expected) although initial jobless claims came in a touch lower than expected (217k v 220k). This morning, all eyes will be on GDP and inflation data from Germany and France along with Italian CPI data.

For US bonds, stronger-than-expected economic rebound didn’t fully outweigh the passthrough from the dovish ECB, with yields declining by -13.0bps on the 2y and -8.4bps on the 10y. Net net that took out -10.7bps off the peak Fed Funds futures rate priced in for next May and -27.7bps since Timiraos’ tweet when terminal pricing had breached 5%. Nevertheless, the dollar index was still up +0.81% for the day as the Fed is currently being out-pivoted by other global central banks.

Heading into big tech earnings after the close, stocks gyrated between gains and losses, but ultimately slumped into the close with the S&P 500 finishing down by -0.61%. Meta’s outsized impact on tech was seen in Nasdaq’s underperformance (-1.63%) after the stock lost -24.56% during trading hours and the share price closed at its worst level since early 2016. Sector-wise, industrials led the pack (+1.14%) on strong earnings (Caterpillar gained +7.71% and Honeywell climbed +3.27%) with financials close behind (+0.75%) on a steeper curve whilst, on the other hand, IT (-1.52%) and communications (-4.12%) weighed down on the S&P 500. It was thus unsurprising that despite a big loss on the day for the index, 55% of its members actually finished higher by the close since the two sectors together take up nearly a third of the index by weight. Along with Caterpillar and Honeywell, we got an earnings beat from McDonald’s, who’s share price climbed +3.31%.

In Europe, the Stoxx 600 (-0.03%) closed nearly flat ahead of today’s major data releases and despite the tailwinds from falling European yields. Showing growth concerns, cyclical sectors like IT (-1.76%), materials (-0.87%) and industrials (-0.47%) were a major drag on performance together with healthcare (-1.13%) and consumer discretionary stocks (-0.65%). So energy (+3.76%), real estate (+2.56%) and utilities (+1.07%) did most of the heavy lifting to keep the index afloat for the day. In data, we also had a tailwind from an upward surprise in Germany’s consumer confidence, which rose to -41.9 from -42.5 (vs consensus of -42.3). Data from Italy was more mixed, with a miss on consumer confidence (90.1 vs 93.5 expected) but a beat on the manufacturing gauge (100.4 vs 100).

Asian equity markets are mostly trading lower this morning due to weaker earnings posted by Wall Street’s tech giants. As I type, the Hang Seng (-1.91%) is the largest underperformer followed by the CSI (-1.27%), the Shanghai Composite (-0.83%) and the Nikkei (-0.35%). Elsewhere, the KOSPI (-0.09%) is swinging between gains and losses.

As mentioned, the Bank of Japan (BOJ) continued its dovish tone, keeping interest rates unchanged due to weak growth prospects, while keeping YCC in place. In its quarterly review of its projections, the BOJ mentioned that it sees core consumer inflation to hit 2.9% for FY2022 and 1.6% the following year. It projects inflation to hit 1.6% in fiscal 2024.

Ahead of the BOJ’s rate announcement, Japan’s Prime Minister Fumio Kishida unveiled a new economic stimulus package that will include 29.1 trillion yen ($199 billion) in government spending. The overall size of the package will likely reach 71.6 trillion yen, when spending by municipalities and companies is taken into account.

Staying on Japan, Tokyo CPI inflation rose sharply to +3.5% y/y in October (v/s +3.3% expected), picking up from +2.8% increase in September. At the same time, the core inflation hit +3.4%, the highest level since 1989 while sharply accelerating from September’s +2.8% gain, indicating broadening inflationary pressure. Separately, Japan’s jobless rate surprisingly rose to 2.6% in September from previous month’s 2.5% while the Job-to-applicant ratio improved for the ninth consecutive month to a 2-1/2-year high of 1.34 in September from 1.32 in August.

Looking ahead, today’s data line up in the US will include Q3 employment cost index, September personal income, personal spending, PCE deflator and pending home sales. In Europe, Germany and France will release Q3 GDP and October CPI figures, with the latter also due for Italy. Other indicators will include consumer spending and PPI for France, PPI and hourly wages for Italy and economic and industrial confidence for the Eurozone. The earnings list will be lighter than in previous days but will feature key commodity companies like Exxon Mobil, Chevron, Equinor and Eni. Other notable reporters will include AbbVie, NextEra Energy, Sanofi, Porsche, Airbus, Volkswagen, Colgate-Palmolive, BBVA and LyondellBasell.

Tyler Durden

Fri, 10/28/2022 – 08:05

aim

nasdaq

asx

gold

iron