Uncategorized

Futures Rise On Hope China’s Deflation Will Lead To More Policy Easing

Futures Rise On Hope China’s Deflation Will Lead To More Policy Easing

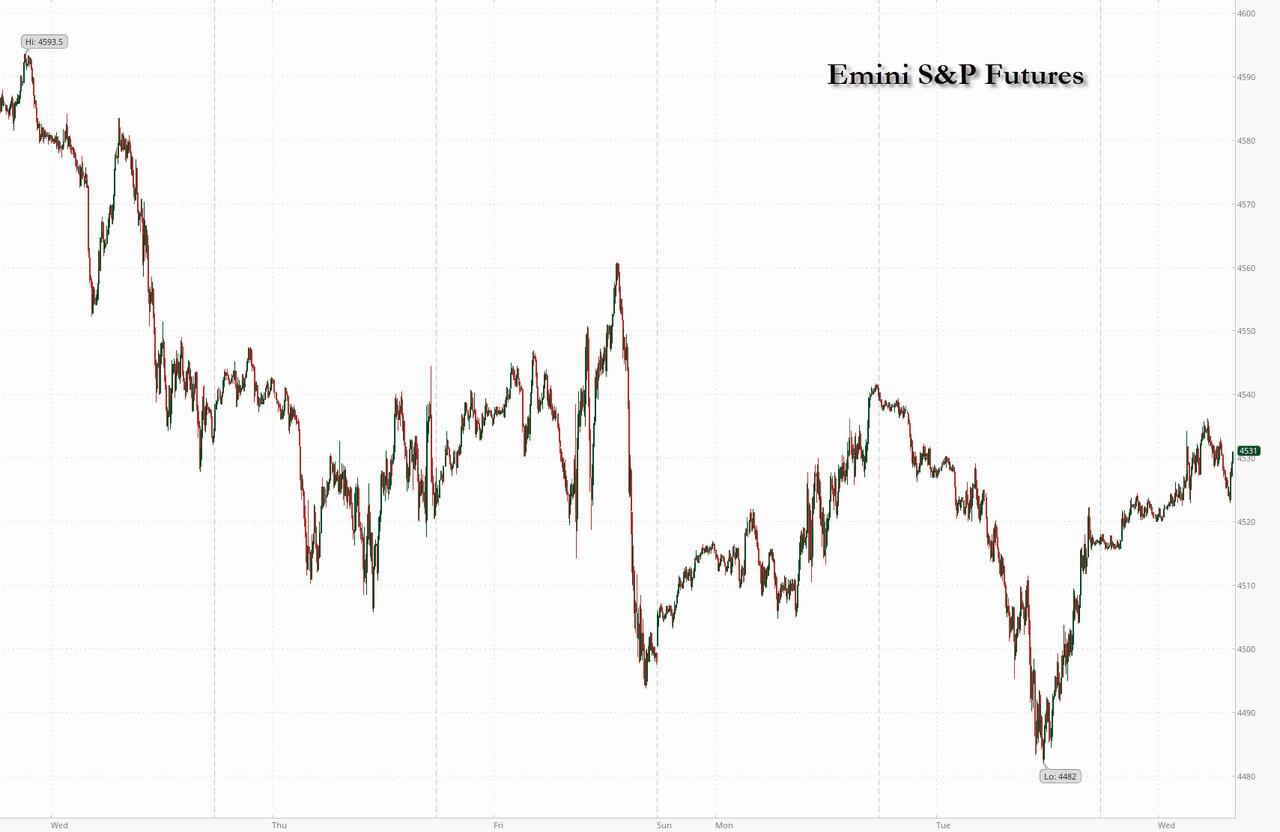

S&P futures point to a higher open after China officially entered…

Futures Rise On Hope China’s Deflation Will Lead To More Policy Easing

S&P futures point to a higher open after China officially entered into deflation with -0.4% CPI print, continuing the buying momentum from the second half of yesterday’s session while European stocks rebound sharply from yesterday’s rout led by a rebound in Italian banks after the government backtracked on part of its new windfall tax on lenders. As of 7:45am ET, both S&P and Nasdaq 100 futures are 0.2% higher with other global markets also in risk-on mode, with the euro strengthening, copper rebounding, 10Y TSY yields rising to 4.03% ahead of another closely watched bond auction later today (US government is selling $38 billion of new 10-year notes, $3 billion larger than the last 10-year note debut in May) and oil rising by $1, just inches away from 2023 highs. Rice in Asia soared to its highest level since 2008.

China’s CPI – coming one day before the US inflation number – printed negatively for the first time in two years which is likely to produce a deflationary impulse on core goods inflation, and which according to JPM’s trading desk could prove useful to the Fed (and markets) if we see the US Consumer shift back from Services demand to Goods demand this year (more in the full JPM trading desk note this morning available to pro subs). Today’s macro data and earnings focus is on mortgage applications (down 3.1% after sliding 3.0% last week) and DIS earnings. Homebuilders have outperformed the SPX by 23% YTD.

In premarket trading, all the megacap techs are higher, with both KRE and XLF indicated marginally higher. Commodities are higher led by Energy, which also saw a late day rally. WeWork shares crashed 17% after the co-working business said there is “substantial doubt” about its ability to continue operating. Here are some other notable premarket movers:

- Lyft falls as much as 8% after the ride-hailing company reported its slowest revenue growth since the pandemic.

- Penn Entertainment shares rise 9.6% after the sports-entertainment company announced a long-term exclusive partnership with Disney’s ESPN.

- DraftKings fell as much as 6.7% on concern the tie-up between Penn Entertainment and Disney’s ESPN will increase competition.

- Rivian shares rise as much as 2.2% after the electric-vehicle startup raised its full-year production forecast to 52,000 vehicles from 50,000. The company also reported better-than-expected second-quarter results.

- Twilio shares rise as much as 7.9% after the software company reported second-quarter results that beat analysts’ expectations and raised its profit outlook for the year.

- Marqeta jumps 17% after second-quarter revenue at the commerce payments platform beat analyst estimates and analysts flagged the renewal of the Cash App contract with Block (SQ US) as a positive.

- Tango Therapeutics jumps as much as 80%, on track for its biggest rise on record if gains hold, after data was published on competitor Mirati Therapeutics Inc.’s cancer drug candidate MRTX1719.

- Coupang gains 4% after the online retailer reported second-quarter earnings per share that beat estimates. Citi said the company had a “solid” beat on the top-line and Ebitda.

The tentative improvement in sentiment faces a test on Thursday when the latest US CPI data is published. It takes place as a closely watched bond-market gauge of inflation expectations is rising back toward a nine-year high, signaling elevated price pressures for years. The US five-year inflation breakeven – which basically is a proxy for oil prices – has risen to around 2.5%, just shy of the peak in April 2022, when it reached the highest since 2014.

The “inflation report will be key if today’s rally is to be sustained.” said Lewis Grant, a senior portfolio manager at Federated Hermes. “Investor risk aversion has started to wane but remains volatile and investors are anxiously searching for the next signal.”

European stocks are ahead, led by a rebound in Italian banks after the government backtracked on part of its new windfall tax on lenders. The Stoxx 600 is up 1% while the Euro Stoxx Banks Index adds 1.7% after falling 3.5% on Tuesday. UniCredit SpA and Intesa Sanpaolo SpA, at the center of Tuesday’s declines when the new tax was unveiled, became some of Wednesday’s biggest gainers, boosting the Stoxx Europe 600 as much as 1% Wednesday. Here are some of Europe’s top movers:

- Delivery Hero gains as much as 10% after the food delivery company demonstrated its path to profitability with a positive adj. Ebitda in the first half

- Vestas Wind Systems rises as much as 3.8% after it published earnings analysts said showed a stronger-than-expected performance for the firm’s Services business

- Sampo shares rise as much as 5.9%, the most since March 2022, after the insurance company owner’s second-quarter earnings came in better than feared

- Italian banks rebound from Tuesday’s slump after the government issued a clarification of its new tax on banks’ windfall profits, saying it will be capped

- Fraport rises as much as 5.2% after Morgan Stanley boosted its price target for the German airport operator as second- quarter earnings provided much-wanted relief

- E.On gain as much as 2.3% after the German energy networks operator reported first- half results in line with an earlier update

- TP ICAP surges as much as 16%, the most since 2020, after the financial services firm delivered results which Canaccord says “give comfort,” and announced a buyback

- Hill & Smith rises as much as 10% as analysts highlights good first-half results and balance sheet strength for the infrastructure and transport company

- Flutter Entertainment drops as much as 6.1% as a new partnership between Penn Entertainment and Disney’s ESPN stoked concern over rising competition

- Ahold Delhaize shares slip as much as 3.6% in early trading after revenue and adjusted operating profit in the US came in below expectations

Asian stocks were mixed after two days of declines, weighed by losses in some Chinese stocks as latest economic data showed further acceleration of deflationary pressures in the economy. The MSCI Asia Pacific Index was up 0.1% for the day. “Investors are clamoring for broad-based stimulus in China. I don’t think we are going to get that,” David Chao, strategist at Investec Asset Management, said on Bloomberg Television. Chao sees China moving ahead with piecemeal measures to support consumption and private investment that may result in “a pop in Chinese equities later this year.”

- Chinese stocks in Hong Kong erased a drop of as much as 0.9%, while the CSI-300 was down about 0.2%, as markets reflected on the mixed inflation data from China which showed CPI Y/Y slipped into deflation territory, albeit at a narrower-than-expected drop in prices, while factory gate prices continued to fall at a steeper than forecast pace. Property stocks in the mainland rebounded after a report said that tier-1 cities are discussing potential measures to ease the malaise in the sector. Property stocks have taken a beating this week over potential default at Country Garden Holdings.

- Japan’s Nikkei 225 weakened with trade initially indecisive amid an influx of earnings releases and with the biggest winners and losers all driven by corporate results including SoftBank which was near the bottom end of the spectrum after its surprise loss.

- Meanwhile, Korean stocks were set to snap a five-day selling spree, with retail and foreign investors nibbling in the market. An EV-led selloff in the market has sapped risk sentiment this week, but technology stocks are leading the rebound.

- Indian stocks reversed earlier losses and closed higher on Wednesday, helped by advances in shares of automobile and metal producers. The S&P BSE Sensex rose 0.2% to 65,995.81 in Mumbai, while the NSE Nifty 50 Index advanced 0.3% to 19,632.55. Technology stocks and Reliance Industries also helped benchmarks reverse earlier losses as they recovered in late buying by investors. The BSE IT index closed 0.3% higher.

In FX, the Bloomberg Dollar Index falls 0.1%. The Swedish krona and Norwegian krone are the best performers among the G-10 currencies. The Aussie climbed as much as 0.3% to 65.64 US cents after the People’s Bank of China set the dollar-yuan rate at 548 pips below traders’ estimate, signaling it’s in no rush to withdraw support for the currency. China’s state-owned banks were also seen selling dollars, according to Asia-based FX traders.

In rates, 10-year Treasury yields ticked up ahead of another closely watched bond auction later today, while the treasuries curve was flatter with front-end yields modestly cheaper and long-end little changed vs Tuesday’s closing levels, outperforming bunds and gilts. The US government is expected to sell $38 billion of new 10-year notes, $3 billion larger than the last 10-year note debut in May. Treasury 10-year yields around 4.03%, marginally cheaper on the day with bunds and gilts lagging by additional 2.5bp and 1.5bp in the sector; long-end outperforms ahead of 10- and 30-year supply over Wednesday and Thursday, with 2s10s and 5s30s spreads flatter by 1bp and 1.5bp on the day. Japan bonds drew support during Asia session from data showing China experiencing deflation. Focal point of US session is upsized 10-year note auction, following strong demand for Tuesday’s 3-year note sale. The Treasury auction cycle resumes with $38b 10-year new issue at 1pm New York time and concludes with $23b 30-year bond sale Thursday. WI 10-year at around 4.03% is ~17bp cheaper than July’s stop-out and above auction stops since November.

The week’s debt auctions will gauge how concerned investors are about a rising US budget deficit, a week after Fitch Ratings decided to strip the US of its top credit rating. Tuesday’s $42 billion sale of three-year notes had a lower-than-expected yield, a sign that demand was stronger than anticipated.

In crypto, the Fed announced the creation of an activities supervision program to oversee bank tech initiatives which will focus on activities related to crypto, blockchain tech and non-bank tech partnerships, while the Fed said state member banks should receive written non-objection from the Fed before issuing, holding or transacting in dollar tokens, according to Reuters.

In commodities, US crude futures advance, with WTI rising 1% to trade near $83.70. Spot gold adds 0.1%. Bitcoin is down 0.6%.

Looking ahead to today, it will be quiet in terms of data, with weekly mortgage applications in the US and Canada’s monthly building permits. Meanwhile, as the earnings season starts to wind down, we will hear from the likes of Walt Disney, Sony, Vestas and Illumina.

Market Snapshot

- S&P 500 futures up 0.3% to 4,533.75

- MXAP up 0.1% to 165.09

- MXAPJ up 0.5% to 522.35

- Nikkei down 0.5% to 32,204.33

- Topix down 0.4% to 2,282.57

- Hang Seng Index up 0.3% to 19,246.03

- Shanghai Composite down 0.5% to 3,244.49

- Sensex down 0.3% to 65,640.89

- Australia S&P/ASX 200 up 0.4% to 7,337.96

- Kospi up 1.2% to 2,605.12

- STOXX Europe 600 up 0.9% to 462.95

- German 10Y yield little changed at 2.47%

- Euro up 0.2% to $1.0975

- Brent Futures up 0.3% to $86.41/bbl

- Gold spot up 0.2% to $1,929.02

- U.S. Dollar Index down 0.12% to 102.40

Top Overnight News

- A US plan to restrict investment in China will probably only apply to companies that get at least half their revenue from sectors such as quantum computing and AI, people familiar said, allowing PE and VC firms to still put money into bigger conglomerates. The proposal, expected in coming days, will take about a year to go into force. BBG

- China’s CPI falls into deflation in Jul (it came in at -0.3% vs. flat in June but not as bad as the Street’s -0.4% forecast) while the PPI sank 4.4% (better than -5.4% in June, but worse than the Street’s -4% forecast). BBG

- Italy backtracks on its planned bank windfall tax as the gov’t looks to calm market jitters, stating that the levy would be capped at 0.1% of RWAs, much smaller than some analysts had feared (the tax will only raise about EU1.8B). FT

- Talks are ongoing to restart the deal that allowed Ukraine to export grain via a safe corridor on the Black Sea, Turkish President Recep Tayyip Erdogan said late Tuesday after speaking with Russian leader Vladimir Putin. BBG

- US banks suffered almost $19bn of losses on soured loans in the second quarter, the highest level in more than three years as lenders contend with rising defaults among credit card and commercial real estate borrowers. FT

- The CBO paints a challenging fiscal picture for the US and now expects that the total deficit for 2023 will be $1.7 trillion, or about $200 billion larger than the estimate it published in May. CBO

- New contract demands made by the United Auto Workers union would add more than $80 billion to each of the biggest US automakers’ labor costs, according to people familiar with the companies’ estimates. BBG

- WeWork on Tuesday raised doubt about its ability to stay in business as the co-working space provider faces losses and a dwindling cash pile amid major changes in the way people work. WSJ

- Amazon is in talks to join other tech companies as an anchor investor in the Arm IPO, a person familiar said. The offering is expected next month and may raise $10 billion. Amazon is already one of Arm’s biggest clients. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as participants digested a deluge of earnings releases and the latest inflation data from China which was mixed but showed consumer prices in deflationary territory for the first time in more than two years. ASX 200 was just about kept afloat by the outperformance in its top-weighted financial sector after Australia’s largest lender CBA posted a record FY profit. Nikkei 225 ultimately weakened with trade initially indecisive amid an influx of earnings releases and with the biggest winners and losers all driven by corporate results including SoftBank which was near the bottom end of the spectrum after its surprise loss. Hang Seng and Shanghai Comp were subdued as markets reflected on the mixed inflation data from China which showed CPI Y/Y slipped into deflation territory, albeit at a narrower-than-expected drop in prices, while factory gate prices continued to fall at a steeper than forecast pace.

Top Asian News

- US is set to limit the scope of the China investment ban with a revenue rule and the order limiting investments is expected in the approaching days, according to Bloomberg.

- US lawmakers asked the FCC to address potential threats from Chinese cellular Internet of Things modules in US networks.

- China’s National Bureau of Statistics said the Y/Y decline in consumer prices is only temporary.

- China government considering holding leaders with Japan on the sidelines of the ASEAN meeting in Indonesia, according to Kyodo.

European bourses are firmer across the board, Euro Stoxx 50 +1.4%, with newsflow light and the main mover being banks clawing back downside from the Italian windfall tax following an adjustment. As such, the FTSE MIB +1.9% outperforms while the OMX Copenhagen +0.4% is the relatively underperformer as Novo Nordisk pares some of Tuesday’s pronounced gains. Stateside, futures are on the front foot and making up for some of the prior session’s downside, ES +0.3%, as risk sentiment improves and was further assisted by Fed’s Harker.

Top European News

- UK government is pushing back against attempts by some members of the House of Lords for tighter corporate transparency and warned that publishing all trust data could be problematic, according to FT.

- Cap on Italy bank windfall tax halves the estimated hit on average CET1 to 30bps with Fineco (FBK IM) and Bper (BPE IM) among banks benefiting the most, according to Jefferies; elsewhere, cap at 0.1% of assets for new Italian bank tax equates into an aggregate total impact of EUR 1.9bln for banks/asset gatherers, via UBS.

- Swedish NIER Forecasts (July): economy heading for a downturn. Riksbank Rate, end-2023: 4.0% (prev. 3.75%)

FX

- DXY dips under 102.50 to a 102.29 session trough, but price action overall remains contained in quiet trade and newsflow.

- Yuan was in focus during APAC hours given Chinese inflation, with the CNH benefitting post-release and spurred further by reports China’s major state-owned banks are seen selling dollars to buy Yuan.

- Antipodeans are the relative outperformers given the week’s hefty losses thus far, as sentiment improves slightly and the USD pulls back as mentioned.

- EUR and GBP are both benefiting from the tone/broader USD action, with specifics limited and EUR perhaps deriving support from the Italian government altering its windfall tax.

- PBoC set USD/CNY mid-point at 7.1588 vs exp. 7.2198 (prev. 7.1565)

- China’s major state-owned banks were seen selling dollars to buy yuan in the onshore spot FX market.

Fixed Income

- Core benchmarks are relatively contained and yet to deviate much from the unchanged mark in limited newsflow ex-supply; though, there is a minor discrepancy between the performance of core and periphery EGBs.

- Gilts have been the relative outperformers throughout the session with specifics limited though it is worth highlighting that UK debt didn’t benefit quite as much from the week’s initial bullish price action; the 10yr DMO outing was well received and spurred a fresh session high.

- Bunds have been in-fitting but came under some pressure following a relatively tepid German sale, though it is worth caveating that summer conditions apply and desks point out the timing coincided with large volumes going through, which are likely sell orders.

- Stateside, USTs are in-fitting and given the action, there is little of note occurring across the curve where yields are under very modest pressure.

Commodities

- Energy tilts firmer after an overnight session of sideways trade, complex continuing to derive support from Saudi commentary earlier in the week.

- Crude benchmarks are currently above the USD 83.00/bbl and USD 86.50/bbl marks for WTI Sep’23 and Brent Oct’23 respectively.

- Spot gold sees marginal gains, albeit as a function of the softer USD with the yellow metal in a tight range.

- LME copper trades with modest gains but remains under the USD 8,500/t mark in a USD 8,487.50-347.50/t range.

- Iranian oil official says Iran is to produce an extra 250k BPD of oil by the end of summer, according to Tasim.

- India Food Secretary says India has adequate stocks of rice and wheat. Follows on from rice prices within Asia lifting to their highest since 2008.

Geopolitics

- Russia’s Defence Minister says Russia is to build up forces at the Western borders, according to Tass.

- Russia shot down two combat drones that were headed towards its capital, according to AFP News Agency citing the Moscow Mayor.

- Polish Deputy Interior Minister says 2k troops to be sent to the Belarus border, via PAP.

US Event Calendar

- 07:00: Aug. MBA Mortgage Applications -3.1%, prior -3.0%

DB’s Jim Reid concludes the overnight wrap

In what is proving to be a volatile August so far, with negative headlines outpacing positive ones, yesterday saw a return to risk-off leaving the S&P 500 down -0.42% on the day, and -1.95% for the month so far. This occurred on the back of weaker Chinese trade data we reported yesterday coupled with negative news on both sides of the Atlantic for the banking sector. However, sentiment improved during the US session, with S&P 500 recovering after being -1.2% down at the lows, in part following a strong 3yr Treasury auction. China has slipped into deflation this morning as expected but the data was broadly inline so there been no additional sell-off momentum so far, with fresh stimulus hopes still in the background.

In the US, the regional banking story reappeared in the headlines after Moody’s downgraded ten small and midsize banks and put a number of larger firms on review or negative outlook. 29 banks in total saw some kind of action. The US regional bank index traded more than -4% lower following the news but recovered to close at -1.38%. The broader banking sector also underperformed, with S&P 500 banks down -1.07%. The regional banking index had reached a post-SVB high the previous day, with a +34% increase since its low in mid-May, having reversed about two thirds of the post-SVB decline. Moody’s cited higher funding costs, potential regulatory capital weakness and increasing commercial real estate risks. In my mind, until we truly know where CRE will bottom its impossible to call the all clear for this cycle. This story won’t fully play out for some time though.

Over in Europe, Italian banks saw a sharp decline (-8.27%) after the Italian government announced a one-off windfall tax of banks that will amount to 40% of the excess net interest margin earned in 2023 (or 2022 if that is higher). However, in the evening the government issued a clarification that the levy would not exceed 0.1% of a firm’s assets. In an update published overnight, our European bank analysts estimate that such a cap would reduce the overall size of the tax by over 40%, though it would still take more than 10% from 2023 profits. See here for more. So this adjustment should improve sentiment today. The broader European banking index had declined -3.54% yesterday, though it is still up +13.6% year-to-date (versus + 7.93% ytd for the broader STOXX 600). The Italian FTSE-MIB (-2.12%) led the declines in Europe with the DAX and CAC -1.10% and -0.69% respectively. Beyond the immediate market impact, the story is a reminder that the burden-sharing of the costs and benefits from higher rates has a habit of becoming a political issue.

The risk-off mood led a decline in long-term yields, with 10yr treasuries down -6.7bps and 30yr -6.3bp (4-5bps up from the day’s lows though). The 2yr had seen a modest sell-off earlier in the day, but ended up closing -1.3bp lower, falling a few bps after a strong 3yr Treasury auction. This saw $42bn of 3yr notes issued at 4.398%, nearly 2bps below its pre-auction trading, with strong indirect demand and record low primary dealer take down. So a successful start to the increased refunding supply of Treasuries. This will be tested more with the 10yr auction today and 30yr auction tomorrow. Yesterday, our US rates strategists published a chart that nicely visualises the large increase in supply that’s due in the coming months – see here for more.

Back in Europe, yields saw an even stronger bull flattening rally. 2yr bund yields were down -6.9bps, while the 10yr yield declined by -13.3bps, its sharpest daily fall since mid-June as the China and banking story dominated.

As discussed earlier, it was a bad day for US equities, but better than it might have been, with the S&P 500 closing -0.42% down. Financials (-0.88%) led the decline. Tech also had a bad day, with the NASDAQ down -0.79% and tech mega caps underperforming, although Apple managed to stem its losses (+0.53%) after five days of decline. A notable outperformer was healthcare, led by a positive reaction to Eli Lilly & Co results the previous evening, which saw its shares jump up by +14.9%. Energy also gained (+0.49%), as oil moved higher during the day (WTI crude +1.20% to $82.92/bl). Comments by Ukraine’s President Zelensky warning that it could target Russian ports if Russia continues to block Ukrainian waters added to oil supply concerns.

In Fed speak, we heard from Philadelphia Fed President Harker. For someone generally perceived to be around the median on the FOMC (and a voter this year), his comments leaned dovish, noting that “we may be at the point where we can be patient and hold rates steady and let the monetary policy actions we have taken do their work”. He also spoke in favour of a soft landing path, saying that “I expect only a modest slowdown in economic activity to go along with a slow but sure disinflation”. Meanwhile, Richmond Fed President Thomas Barkin (non-voter) gave little colour on the policy front, saying he was “leaning toward waiting until September to decide” if another hike is appropriate. In terms of Fed fund expectations, the market continued to see a 34% chance of a hike across the next two meeting but moved to price slightly more cuts for 2024, with end-24 pricing down -2.6bps to 3.97%, its lowest in nearly three weeks.

Overnight, Chinese annual CPI fell in July for the first time in 28 months, slipping -0.3% y/y (v/s -0.4% expected), having flatlined in the previous month. Additionally, PPI extended its decline for the 10th straight month, down -4.4% y/y in July following a -5.4% drop in June as against a market forecast for a -4.0% fall. With CPI and the PPI both falling simultaneously for the first time since 2020, it confirms economy wide deflation which will increase the drumbeat for more stimulus.

Given the inflation data was pretty much inline, Asian equities are more playing catch down to the US move rather than starting a fresh sell-off. The Nikkei (-0.42%), Hang Seng (-0.12%), CSI (-0.19%) and the Shanghai Composite (-0.36%) are seeing losses whilst the KOSPI (+1.08%) is actually higher. S&P 500 (+0.08%) and NASDAQ 100 (+0.18%) futures are trading slightly higher. Meanwhile, yields on the 10yr USTs (-0.6bps) are broadly steady, trading at 4.02% as we go to press.

Looking back at the data yesterday, US data was sparce. The NFIB small optimism ticked up to 91.9 in July (91.3 exp, 91.0 prev.), its highest since last autumn. On the other hand, wholesale trade sales saw a larger-than-expected decline in June (-0.7% vs -0.2% exp).

Over in Europe, we had the ECB’s latest consumer expectations survey. This showed a further moderate decline in inflation expectations in June. However, our economists’ dbDIG consumer survey shows inflation expectations stabilising in July, suggesting that yesterday’s print may mark the end of the decline in the ECB survey. Elsewhere, Germany’s July CPI print was confirmed at +6.2% yoy.

Looking ahead to today, it will be quiet in terms of data, with weekly mortgage applications in the US and Canada’s monthly building permits. Meanwhile, as the earnings season starts to wind down, we will hear from the likes of Walt Disney, Sony, Vestas and Illumina.

Tyler Durden

Wed, 08/09/2023 – 08:18

nasdaq

asx

ax

gold

copper