Uncategorized

Futures, Oil Rise As China Reopens

Futures, Oil Rise As China Reopens

US futures reopened from the extended Christmas break, rising as high as 3900 and following European and…

Futures, Oil Rise As China Reopens

US futures reopened from the extended Christmas break, rising as high as 3900 and following European and Asian stocks higher as China’s reopening buoyed sentiment in the final trading week of the year. At 745am ET, S&P futures were up 0.5% at 3,890 while Nasdaq futures rose 0.2% even as Tesla tumbled again in premarket trading. Asian stocks extended gains for a second day after China moved to end quarantine for inbound visitors, effectively ending its zero-Covid regime. Futures are advancing after the underlying benchmarks slid over the last three weeks. Treasury yields were higher, 5Y-30Y at highest levels since November, with the curve steepening. The dollar declined versus most of its G-10 peers. Gold was in the green. Oil in New York traded for $80 a barrel, buoyed not only by China’s reopening but as freezing weather shut more than a third of Texas Gulf Coast refining capacity over the past few days. Trading remains thin with many markets including Australia, New Zealand, the UK and Hong Kong closed for holidays

In premarket trading, TSLA shares extended their recent losses, sliding another 3% after Reuters reported the EV carmaker would run reduced production at its Shanghai factory, shutting down output from Jan 20 to Jan 31 for the Chinese New Year. US-listed Chinese stocks rose in premarket trading on Tuesday, boosted by China’s decision to reopen its borders and set the country on track to emerge from three years of isolation under its Covid Zero policy: Alibaba and Pinduoduo rose +2.3%, JD.com was up +2.6%, and Bilibili jumped 3.8%. Here are some other notable premarket movers:

- AMC Entertainment Holdings Inc. (AMC) is down 8% in premarket trading, putting the movie theater operator on course to extend its rout from last week.

- KalVista (KALV) shares are up 12% in premarket trading after the company announced the registered direct offering. The company also sold 182k pre-funded warrants, bringing total gross proceeds to $58m.

- Nio (NIO) depositary receipts decline 6.7% after the Chinese electric-vehicle maker cut its 4Q delivery outlook to 38,500-39,500 vehicles from previously released estimates of 43,000 to 48,000 vehicles.

- Southwest Airlines (LUV) falls 4% after saying it expects the flight chaos caused by the massive winter storm that battered the US to continue for at least another few days as the government questioned whether the airline is complying with its customer service plan.

- Oil stocks are in focus after crude rose amid China’s moves to unwind its Covid Zero policy, and freezing weather across the US that prompted refinery closures in the vital Texas Gulf Coast area. Keep an eye on shares including Exxon Mobil, Chevron, Conoco.

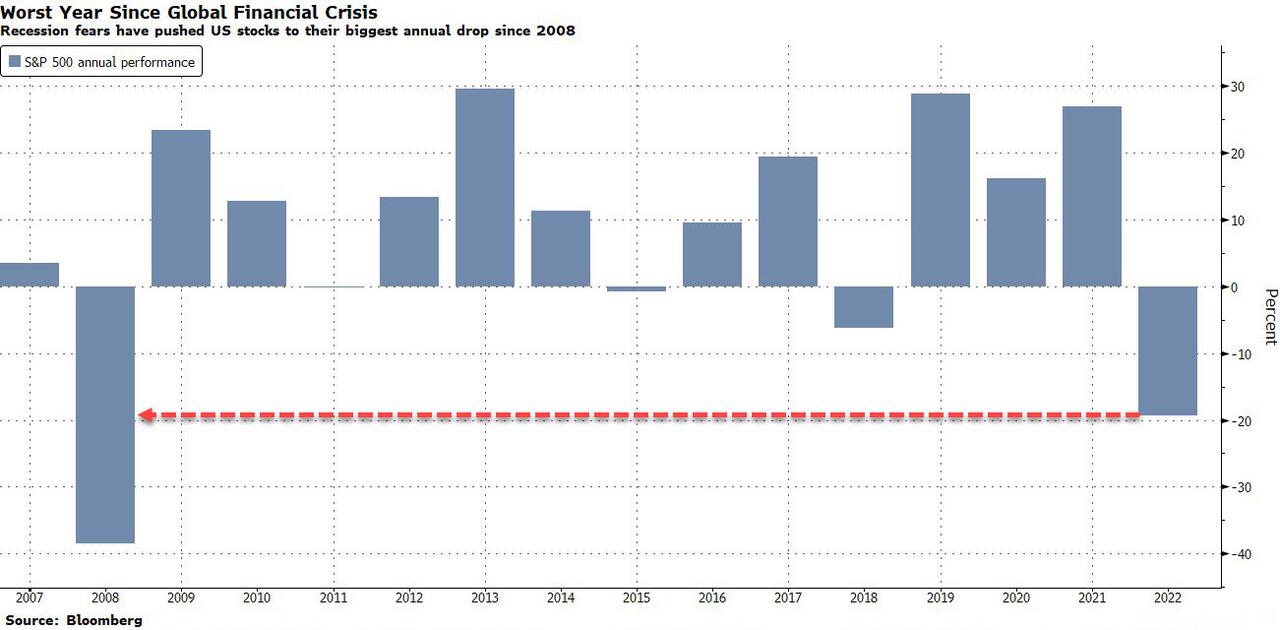

Despite Tuesday’s modest bounce, the Nasdaq 100 and S&P 500 are on track to post the worst annual decline since the global financial crisis. Stocks were roiled this year as the Federal Reserve aggressively tightened monetary policy to tame soaring inflation. Investors are concerned that higher rates will impact company earnings and lead to a recession. The S&P 500 is down almost 20%, while Asian and global stocks still remain down by a similar amount in the worst annual drop since 2008. The 10-year Treasury yield is near 3.75%, up from 1.5% at the start of the year as the Federal Reserve embarked on an aggressive battle against inflatoin. Bitcoin held below $17,000 after starting 2022 at more than $47,000.

Investors are hoping for year-end rally to help mitigate what has otherwise been a brutal run for risk assets, and putting their faith in China’s reopening, even thought a credit-led boost by China likely means even more inflation will be exported soon.

“China has clearly indicated that the country is willing to take the big leap forward in terms of reopening, which the global economy desperately needs,” said Kunal Sawhney, chief executive officer of Kalkine Group. Still, “it may be a little far-fetched to hope for too much from equities in the near to medium term, maybe until mid 2023.”

European bourses were green across the continent with the STOXX Europe 600 Index up 0.5%. Consumer discretionary and energy stocks outperformed in Europe. European oil stocks outperformed on Tuesday as the price of crude received a boost from China further easing pandemic curbs and US refinery closures due to freezing weather. Stoxx Energy sub-index rose 0.8% as of 10:33 am in Paris, while the broader European equity benchmark gained 0.3%. Among majors, TotalEnergies and Eni advanced 1.2%, while London-listed shares of BP and Shell didn’t trade. European luxury stocks were also among the biggest gainers on Tuesday after China said it will no longer subject inbound travelers to quarantine from Jan. 8, putting the country on track to emerge from three years of self-imposed global isolation. Here are the most notable European movers:

- European luxury stocks are among the biggest gainers after China said it will no longer subject inbound travelers to quarantine from Jan. 8 to end three years of self-imposed isolation

- European oil stocks outperformed on Tuesday as the price of crude received a boost from China further easing pandemic curbs and US refinery closures due to freezing weather

- Lotus Bakeries shares fell as much as 5.3% after the Belgian firm was cut to reduce by Degroof Petercam on caution over whether it can match very high sales and growth expectations

- Leonteq falls as much as 6.5% after the company warned it’s less optimistic about 2022 earnings, and after saying a settlement has been reached on UK civil proceedings

- Richter shares plunge as much as 6.8%, the largest intraday drop for the Hungarian pharmaceutical company since March, after the country’s government introduced a windfall tax

- SBB falls as much as 11% on trading ex shares in Neobo Fastigheter, previously known as Amasten, after an EGM last week opted to distribute all of the company’s shares in the subsidiary

Asian stocks gained as China’s move to end quarantine for inbound visitors boosted sentiment across the region. The MSCI Asia Pacific Index climbed as much as 0.6%, led higher by MUFJ and Shiseido. Ten out of 11 sectors were in the green with the financials sector giving the biggest boost to the benchmark. Shares of cosmetics firms, travel and duty free store operators jumped in Japan and in South Korea after Chinese health authorities said inbound travelers will no longer be subject to quarantine from Jan. 8, scrapping the current requirement of eight days isolation.

Japanese stocks rose for a second day, as China’s plan to stop subjecting inbound travelers to quarantine bolstered sentiment. The Topix Index rose 0.4% to 1,910.15 as of the market close in Tokyo, while the Nikkei 225 advanced 0.2% to 26,447.87. Mitsubishi UFJ Financial Group contributed the most to the Topix’s gain, increasing 1.9%. Out of 2,162 stocks in the index, 1,510 rose and 540 fell, while 112 were unchanged. “China is trying to get its economy back on track quickly,” said Hideyuki Ishiguro, a senior strategist at Nomura Asset Management. “Inbound demand in Japan is likely to expand further due to the removal of restrictions on the movement of people in and out of foreign countries.” China Reopens Borders to World In Removing Last Covid Zero Curbs Shares of Japanese department-store and tourism-related companies gained as investors expected these sectors to benefit from Beijing ending its quarantine for travelers

“Now market participants will focus on how much Chinese consumers will actually spend following the reopening,” Han Jiyoung, an analyst at Kiwoom Securities in Seoul, wrote in a note. Equities in mainland China, Vietnam, Indonesia and Thailand also climbed. Trading volume remained thin, down nearly 90% from the 100-day average as markets in Hong Kong, Australia and New Zealand remained closed for holidays. After a 15% surge in November driven by China’s shift away from its strict Covid policy, the main Asian stock benchmark has halted its rally in December and still is poised for its worst year since 2008. With a few trading days left, the gauge is little changed so far this month

In FX, the US dollar and Japanese yen weakened as China’s reopening curbed demand for haven assets. The two currencies dropped against all of their Group-of-10 peers after Beijing also downgraded the management of Covid from its highest level, effectively removing the legal justification for aggressive restrictions. The Bloomberg dollar index slipped as much as 0.4% as trading resumes after Christmas break. Australia’s dollar led gains in commodity currencies amid optimism the unwinding of China’s Covid rules will help speed its economic recovery.

In rates, Treasury yields higher, 5Y-30Y at highest levels since November, amid a global government bond selloff sparked by China’s decision to relax Covid curbs. US 10-year, higher by ~3bp at 3.775%, is highest since Nov. 30 but still below 50-DMA level; most euro-zone 10-year yields are at least 10bp higher on the day. Treasury curve spreads are little changed with yields across the maturity spectrum higher by ~3bp. Final coupon auction cycle of the year begins with $42BN 2-year note sale at 1pm New York time; The WI 2Y yield 4.315% is below last two auction stops; November’s 4.505% result was highest since 2007

In commodities, the outlook for demand from China as the economy reopens boosted the price of oil on Tuesday, along with freezing weather across the US, which prompted refinery closures. West Texas Intermediate crude rose 1% to $80.38 a barrel. Spot gold rose 0.6% to $1,808.46 an ounce.

Market Snapshot

- S&P 500 futures up 0.5% to 3,890

- STOXX Europe 600 up 0.4% to 429.08

- MXAP up 0.4% to 156.28

- MXAPJ up 0.6% to 507.66

- Nikkei up 0.2% to 26,447.87

- Topix up 0.4% to 1,910.15

- Hang Seng Index down 0.4% to 19,593.06

- Shanghai Composite up 1.0% to 3,095.57

- Sensex up 0.6% to 60,916.90

- Australia S&P/ASX 200 down 0.6% to 7,107.69

- Kospi up 0.7% to 2,332.79

- German 10Y yield up 8 bps to 2.48%

- Euro up 0.2% to $1.0653

- Brent futures up 0.5% to $84.38/bbl

- Gold spot up 0.6% to $1,809.12

- U.S. Dollar Index down 0.28% to 104.03

Top Overnight News from Bloomberg

- Equities climbed Tuesday while the dollar declined amid positive sentiment from China’s rollback of Covid isolation measures and the cooling of a key inflation gauge in the US

- European luxury stocks are among the biggest gainers on Tuesday after China said it will no longer subject inbound travelers to quarantine from Jan. 8, putting the country on track to emerge from three years of self-imposed global isolation

- Lower-rated won corporate notes have lagged the rebound in high-grade peers after South Korea’s credit rout, a trend that may continue on concerns about an economic slowdown

- Top executives at Japan’s biggest banks are expecting negative interest rates to linger and see little immediate earnings boost after a surprise move by the nation’s central bank pushed lenders’ shares up by 13% last week

- Profits at industrial firms in China declined in the first 11 months of the year, as production slowed and factory-gate prices fell amid Covid disruptions

US Event Calendar

- 08:30: Nov. Wholesale Inventories MoM, est. 0.3%, prior 0.5%

- 08:30: Nov. Retail Inventories MoM, est. -0.1%, prior -0.2%

- 08:30: Nov. Advance Goods Trade Balance, est. -$96.3b, prior -$99b

- 09:00: Oct. FHFA House Price Index MoM, est. -0.8%, prior 0.1%

- 09:00: Oct. Case Shiller 20 City MoM SA, est. -1.20%, prior -1.24%

- 09:00: Oct. Case Shiller Composite-20 YoY, est. 8.00%, prior 10.43%

- 10:30: Dec. Dallas Fed Manf. Activity, est. -15.0, prior -14.4

Tyler Durden

Tue, 12/27/2022 – 08:17

nasdaq

asx

ax

gold