Energy & Critical Metals

The Copper Conundrum: The “New Lithium” – Navigating the Demand Surge and Supply Shortfall

The copper mining the industry faces a daunting challenge: a looming supply shortfall that threatens to disrupt the green transition…

The global shift towards green technologies is accelerating, and with it, the demand for copper, a critical component in many of these innovations, is set to skyrocket. However, the industry faces a daunting challenge: a looming supply shortfall that threatens to disrupt the green transition.

Copper, often referred to as ‘the new lithium,’ is a vital component in a wide array of applications. From wiring and construction to electric vehicles, solar panels, and other green technologies, copper’s versatility and conductivity make it indispensable. However, the surge in demand for this red metal is outpacing the industry’s ability to supply it, leading to a potential crisis.

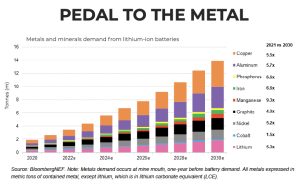

According to McKinsey & Co., a global management consulting firm, the electrification of various sectors is expected to increase annual copper demand to 36.6 million metric tons by 2031. In contrast, the supply is forecasted to be around 30.1 million tons, creating a 6.5 million ton shortfall at the start of the next decade. To put this in perspective, the International Copper Study Group reported that the refined copper demand in 2021 stood at 25.3 million tons.

Aditi Rai, an analyst at Goldman Sachs, has stated that green uses of copper accounted for 4% of copper consumption in 2020, but this is expected to rise to 17% by 2030. A “net-zero emissions” path would mean the world would need an additional 54% of copper by 2030 on top of that forecast.

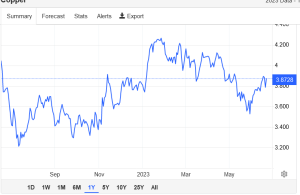

Current Copper Prices Don’t Match Reality

Robert Edwards, a copper analyst at CRU, a leading provider of analysis on the global metals, mining and fertilizer industries, has stated that the copper market is tight, and there’s a narrative around resource scarcity and the green transition with EVs and renewables, as well as the build-out of electricity grids. On paper, it’s a substantial supply gap opening up over the next 10 years. Guy Wolf, Marex’s head of market analytics, has also stated that there’s no slack in the system, no buffer. Copper is the only metal with locked-in demand growth, but prices would need to rise to $15,000 a metric ton to attract investment in new mines. Currently, futures on the London Metal Exchange are around $8,500 a ton.

South America, particularly Chile, currently dominates copper production. However, increasing mine output has proved a challenge, prompting a wave of deal-making in the industry and warnings of a serious supply shortfall over the next decade. Mined output globally in 2022 was 21.8 million tons, rising only 1 million tons over the previous three years.

Analysts forecast little output growth in Peru and Chile. Mines are operating at low staff levels and slowed operations after local protests from community groups, with reasons varying from worker safety to rising governmental control over mine assets. Fitch Solutions, a leading provider of credit and macro intelligence solutions, estimates that 2023 copper mined production in Chile will likely be about 5.7 million tons, the same volume as in 2020.

Barbara Mattos, an analyst at Moody’s Investors Service, a leading provider of credit ratings, research, and risk analysis, has stated that new projects coming online in Peru and Chile will add incremental supply, but there is not a lot in terms of pipeline in terms of the long run. The new ores being mined are of lower grades, meaning that even if mining activity stays flat, copper volumes produced are likely to be lower.

Potential new supplies could come from the rich copper seams in Congo and Zambia in central Africa. They are now being exploited. However, the largest deposits are still in South America. According to Congo’s Ministry of Mines, copper metal exports totaled 2.3 million metric tons in 2022, up from 1.8 million metric tons in 2021, less than half of Chile’s output.

Copper miners have been at the center of a recent spurt of deal-making. For instance, Glencore PLC, a major player in the mining industry, recently offered $23 billion for Teck Resources Ltd., a Canadian miner. Another significant deal was recently approved for the takeover of OZ Minerals Ltd. by BHP Group Ltd., a multinational mining, metals, and petroleum company, in a deal valued at $6.34 billion. These moves indicate the industry’s recognition of the impending supply-demand imbalance and its efforts to address it.

The Lack of New Mines

Yet, the lack of new mined resources remains the main hurdle. The industry needs to invest in new mines, but this is a capital-intensive and time-consuming process. It’s estimated that over $200 billion needs to be spent on new copper mines in the next decade to meet the rising demand. However, the question remains: where will this investment come from, and will it be enough?

The copper industry is also grappling with the increasing capital intensity and cost of running mines. The cost of producing a pound of copper has been steadily rising due to factors such as lower ore grades, deeper ore bodies, higher energy costs, and increased input costs for essentials like water and steel. These factors, coupled with the need for significant capital investment, make the task of increasing copper production a daunting one.

The copper conundrum is a complex issue that requires a multi-faceted solution. It’s clear that simply ramping up production won’t be enough. The industry needs to invest in new mining technologies and practices that can increase efficiency and reduce costs. Governments and regulatory bodies need to provide supportive policies and frameworks that encourage investment in the sector. Finally, the global community needs to invest in recycling and developing alternatives to copper where possible.

In conclusion, the world stands on the brink of a copper supply crisis that could potentially derail the green transition. However, with concerted effort and investment from all stakeholders, it’s possible to navigate this challenge and ensure a sustainable future for both the copper industry and the planet. The stakes are high, but so too are the rewards. As the world continues to electrify and move towards a greener future, the demand for copper will only grow, making it a critical issue that needs to be addressed sooner rather than later.

Uranium Exploration Company Announces Additional Staking in the Athabasca Basin

Source: Streetwise Reports 12/22/2023

Skyharbour Resources Ltd. announced an update from its Canada-based Falcon Project along with additional…

Tesla Launches New Mega Factory Project In Shanghai, Designed To Manufacture 10,000 Megapacks Per Year

Tesla Launches New Mega Factory Project In Shanghai, Designed To Manufacture 10,000 Megapacks Per Year

Tesla has launched a new mega factory…

Giving thanks and taking stock after “a remarkable year”

An end-of-year thank you to our readers, industry colleagues and advertisers before Electric Autonomy breaks from publishing until Jan. 2

The post Giving…