Economics

Zoltan Pozsar and George Gammon’s differing views on the next commodities super cycle

In a recent interview, Credit Suisse’s Zoltan Pozsar talked about his belief that commodities are ripe for a ‘big bull run’…

In a recent interview, Credit Suisse’s Zoltan Pozsar talked about his belief that commodities are ripe for a ‘big bull run’ and that we are now seeing the early innings of the next commodities super cycle.

Although most commodity prices are sharply down this year, this pullback has also come on the back of last year’s 40%-45% boom.

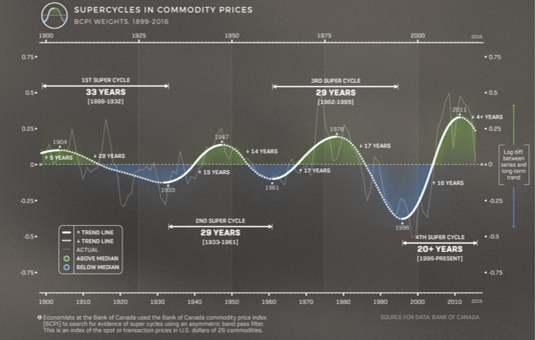

The shape of the commodities super cycle

Commodities tend to follow long price cycles, which are highly correlated with demand-supply mismatches.

With commodities being central to most economic activities, any improvement in growth can immediately lead demand to rise.

However, supplies are a very different matter and are difficult to bring online.

Most projects have long payback periods, considerable uncertainty, need heavy investments, regulatory licensure, and a succession of industry-friendly governments.

So, if demand shifts higher, supplies cannot respond in a timely fashion and prices surge.

To meet the increased demand, suppliers start searching for new reserves, expanding production, and building supply chains.

However, by the time these commodities make it to market, the demand equation which follows shorter business cycles has (often) already peaked and appetite has begun to wane.

Now, we have a situation where supply outstrips demand combined with lesser buying, which leads to lower prices.

This is the core of the commodity super cycle which has repeated over and over in the past.

Pozsar’s case

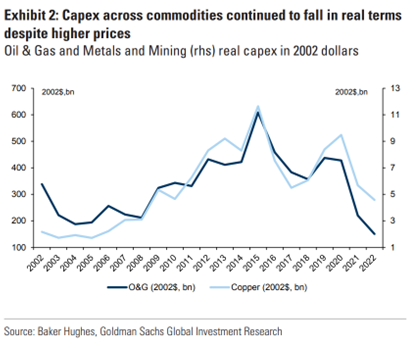

Today, nearly every commodity in the world has been ravaged by a decade of underinvestment.

Although the most recent super cycle peaked in 2011, capex has been suffering in key sectors for years.

This situation has meant that mines and wells have been falling even further behind while existing facilities have begun to suffer from creaking infrastructure and ageing resources.

Zoltan points out that capex return has been consistently weak, while alternative investment narratives such as ESG and the inter-governmental push for net zero have forced companies to turn away from expanding operations that would take years to operationalize at the best of times.

Although not for the same reasons, it is interesting to note that Aswath Damodaran has been a strong proponent of ‘retiring’ the notion of ESG altogether.

He argues that there are no common definitions of what constitutes desirable behaviour and that in the long run a constrained pool of companies cannot outperform an unconstrained one.

Back to commodities, ultra-low interest rates after the GFC have also meant that funds have flowed into financial assets and derivatives instead of real investments.

Geopolitics and trade tensions

In the past year, the world has been exposed to much greater geopolitical risk, retaliatory sanctions, acceleration in economic decoupling and global protectionism.

For instance, many previously commodity-exporting countries are now less willing to trade as they did, but more agreeable to inflows of foreign investment to develop resources at home and then export finished goods.

In its May 2023 update, the Blackrock Investment Institute noted,

We have entered a new world order. Two major geopolitical and economic blocs – one Western-led and one led by China and Russia – are firming up and are increasingly in competition with each other. The fragmentation that’s ensued has led to a dramatic reduction in geopolitical cooperation.

Accordingly, Zoltan expects an expansion of military budgets, onshoring of factories such as in the batteries space, and energy investments to supercharge demand for commodities, especially in the G7 nations.

Given the situation, he argues that if a recession hits this year, the depleted supply of commodities will prove inflationary for these goods.

Interested readers can learn about Peter Schiff’s view on the coming resurgence in inflation here.

George Gammon on the not-so-soft landing

Commenting on Zoltan’s assessment, investor and popular Youtuber, George Gammon expects that a surge in commodities this year, despite a recession, would only be likely in the case of a soft landing.

We know that the First Republic Bank is virtually in ruins, regional bank lending has tightened significantly, much stricter regulatory supervision measures are on the horizon, M2 has declined for eight consecutive months, and a full-blown corporate credit crunch is leaving small businesses particularly vulnerable.

It is worth noting that the latest core CPI data was at 5.6%, while the Fed revised its core PCE target for the year up to 3.5%, continuing to push a hawkish narrative.

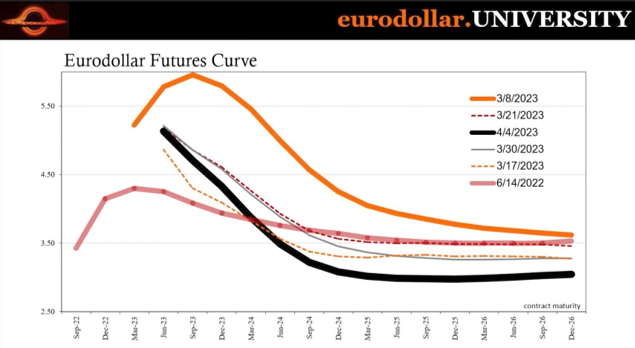

However, eurodollar markets are signalling that demand may fall much more sharply than Zoltan believes, even undercutting the prevailing supply constraints altogether.

Gammon draws attention to the black line, which is of the most recent date and indicates that markets are pricing in a sharp decline in rates in 2023.

He argues that the market is unwilling to accept the Fed’s stance,

No, no, no Jerome Powell. The market isn’t saying that you’re going to pause. The market is saying you are going to pivot and you’re going to pivot fast and you’re going to pivot harder. Those rates are going to plummet (and this would only happen in a hard landing scenario).

In a Bloomberg article, Torsten Slok, Chief Economist at Apollo Global Management stated,

We were already debating a hard landing…credit conditions continue to tighten…that increases risks of a hard landing – even more so than we thought before.

Nouriel Roubini, chairman and CEO at Roubini Macro Associates agreed,

…(we) could have a hard landing for the economy…. achieving price stability, growth stability and financial stability with…the fed funds rate to me looks like mission impossible…so either hard landing and a financial crash or de-anchoring of inflation expectations.

Global recession?

Earlier this year, a survey of chief economists by the World Economic Forum, found that two-thirds of respondents saw a high likelihood of a global recession in 2023.

Regional banks and the housing sector in the US; energy challenges in Europe as well as concerns around political fragmentation; and the state of the residential sector and government finances in China, each point to severe weaknesses that could buckle under the pressure of elevated interest rates.

Gammon concurs,

…and in my opinion, it might not just be a recession it could be a global…black swan event.

In its World Economic Outlook, the IMF projects that advanced economies could show an especially ‘pronounced growth slowdown’ from 2.7% last year to 1.3% in 2023.

If such an event were to occur, commodity prices could fall to much lower levels, at least during the year.

Final thoughts

Gammon agrees with Zoltan, in that they both see that a fresh commodity super cycle will be starting soon and could lead to a decadal bull run.

However, given the high probability that the Fed will be forced to cut rates sharply on account of economic fragilities, Gammon expects a hard landing and a delayed start to a potential bull run.

For its part, the World Bank in its latest Commodity Markets Outlook, forecasts that commodity prices could fall by 21% by the end of 2023, but expects these to stabilize starting 2024.

In my own view, gold may continue to show returns despite the environment, particularly as physical shortages become more acute and global process of de-dollarization gather support.

The post Zoltan Pozsar and George Gammon’s differing views on the next commodities super cycle appeared first on Invezz.

gold inflation derivatives commodities commodity markets interest rates fed inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…