Economics

What To Do About Bonds When Inflation Is Elevated

What To Do About Bonds When Inflation Is Elevated

Authored by Simon White, Bloomberg macro strategist,

Real assets – commodities, gold…

What To Do About Bonds When Inflation Is Elevated

Authored by Simon White, Bloomberg macro strategist,

Real assets – commodities, gold and TIPS – are better positioned than bonds to act as a portfolio and a recession hedge in a regime of elevated inflation. For investors without capacity or liquidity constraints, they are an improved alternative to Treasuries in a 60/40-like portfolio.

Inflation has been making up for lost time after its last two decades of serenity. As well as prompting the fastest rate-hiking cycles from central banks, playing havoc with economic pricing signals, and deepening uncertainty, it is also turning the established rules of investment on their head.

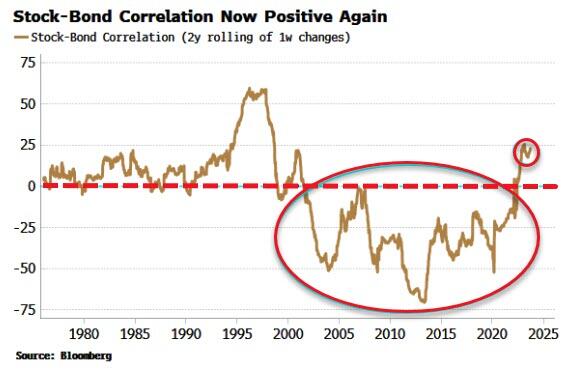

Nowhere is that more visible than the role of bonds. It has long been taken for granted that they possessed two features that made them almost indispensable to multi-asset investors:

1) they acted as a portfolio hedge for equities; and

2) they guarded against recessions.

But both of these characteristics are becoming challenged in the current regime of elevated and unstable inflation. The stock-bond correlation is now positive after years of being negative. This means that rather than bonds having a dampening effect on the volatility of a traditional 60/40-like portfolio (60% equities, 40% bonds), they are amplifying it.

Bonds typically offer lower returns than stocks, so their return-smoothing properties were a key reason why equity investors held them at all. Even better, they tended to rally in a recession, mitigating the steep losses experienced by stocks.

Yet in an inflationary regime, a growth shock can be accompanied by an inflation shock, meaning stocks and bonds fall together. That’s what’s unflatteringly known as a Texas hedge.

It’s time for a rethink. Replacing some or even all of the Treasuries one holds in a 60/40-like portfolio is beginning to look ever more prudent.

But what do you replace them with? There are liquidity, capacity and operational constraints with other assets, such as real-estate, infrastructure, corporate bonds, etc. Moreover there is a higher bar for returns as cash typically provides a better return when inflation is elevated.

In a somewhat perverse way, this could lead many investors back to TINA – there is no alternative – deciding to replace some or all of their fixed-income allocation with equities. But there is one glaring problem here – apart from the obvious “eggs-all-in-one-basket” risk: portfolios heavily tilted to stocks are uniquely exposed to recessions.

So any replacement for Treasuries that mitigates portfolio risk also needs to help cushion the fall from equities in a recession. It turns out that real assets are the optimum port in the storm for investors free from institutional or capacity limitations.

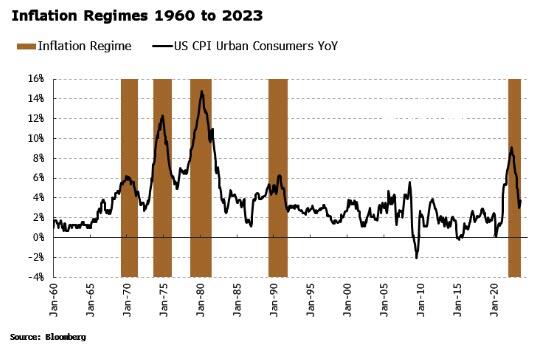

To see why, we need to look at how various assets have performed in low and high-inflation regimes. High-inflation regimes (shown in the chart below) are defined here as when inflation and inflation volatility are persistently above their long-term averages. There are five distinct regimes, including the one we’re in now.

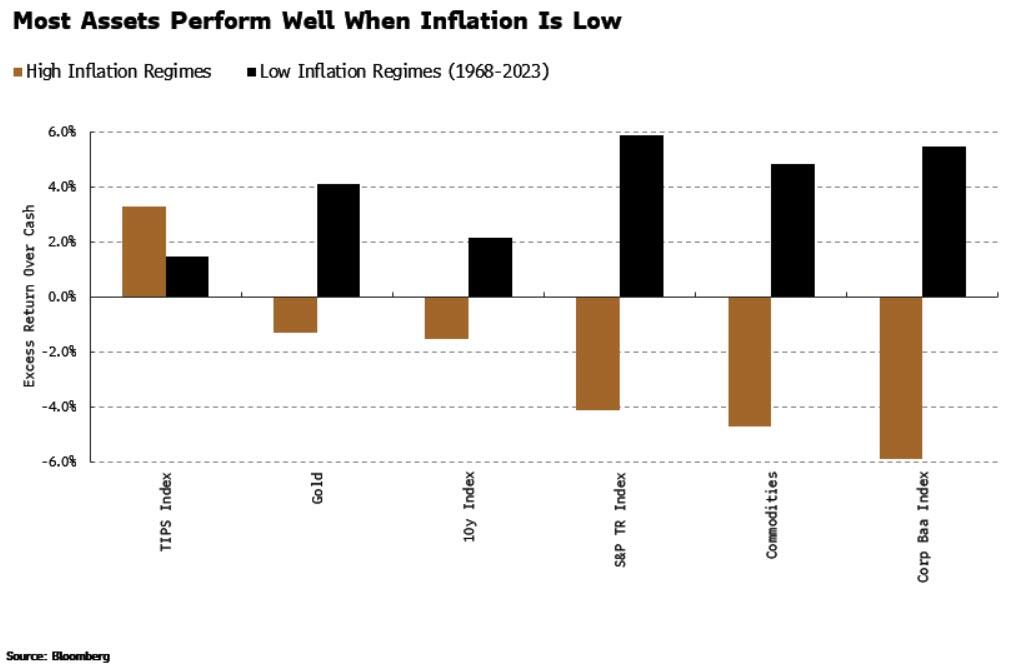

Now let’s look at how the main asset classes performed relative to cash (3-month T-bills) in and out of these high-inflation regimes. As highlighted in the chart below, almost all of the assets shown perform better in the low-inflation regime. That’s mainly down to cash being lower in these periods, making it easier to earn a higher excess return.

In high-inflation regimes, only TIPS perform better than when inflation is low. Equities, along with corporate bonds, see the steepest drop in excess returns between low and high-inflation regimes.

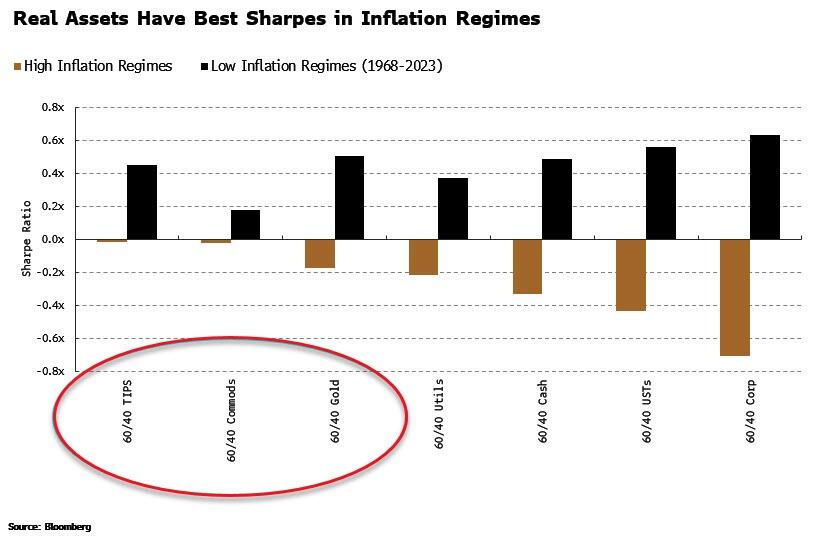

Now let’s combine these assets with 60% equities in 60/40 portfolios, and see how their Sharpe ratios change when inflation shifts from a lower to a higher regime.

The first thing to note is how every portfolio’s Sharpe ratio is worse in the high-inflation regime.

The 60% equity proportion does wonders when inflation is low, but falters when it is not. Indeed the excess return of all portfolios is negative in an inflation regime, as cash returns an lofty 7.4% annualized through such periods.

Secondly, the three portfolios with the best (i.e. least negative) Sharpe ratios all include real assets – TIPS, commodities and gold.

In challenging environments, choosing portfolios with the cleanest dirty hands is the best you can do, and replacing USTs with real assets has historically offered the best risk-adjusted returns when inflation is in an elevated regime.

But that still doesn’t help us with recessions. Stocks and corporate bonds typically see the largest selloffs in a slump. That’s why TINA or 60/40 with corporate debt are a bad idea if you want to avoid portfolio decimation in an economic slowdown.

It turns out, though, that real assets have tended to perform reasonably well in recessions, much better than stocks. Crucially, they tend to perform well in inflationary recessions, the type the next downturn is most likely to resemble.

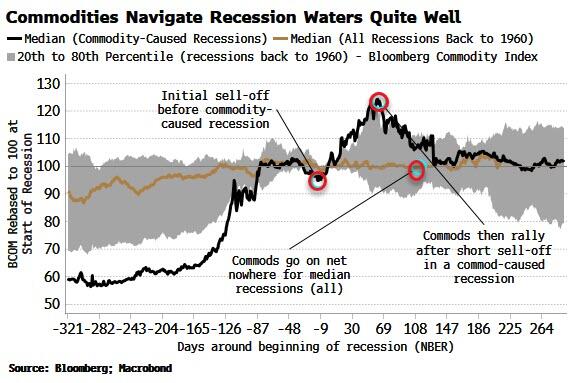

Both TIPS and gold have on average delivered positive nominal returns through recessions going back to 1969. What about commodities?

Financial “rule-of-thumbism” would tell you they do terribly in recessions. But that doesn’t bear much scrutiny. Commodities on average flat-line through economic slumps. However, if we look at commodity-induced recessions – as the next downturn is likely to have proved to have been – commodities rally after the recession has started.

In such contractions, commodities sold off on the pre-recessionary growth scare, but this in fact eased the growth shock, meaning that commodities – which are sensitive to the level of demand rather than its change – could rise through much of the recession.

Commodities, gold and TIPS are not for everyone and their market sizes are considerably smaller than nominal Treasuries. Moreover, other real assets such as infrastructure, real-estate and so-called alternatives may confer similar benefits, but these bring other potential issues such as liquidity mismatches and ease of access and management.

Real assets are typically spurned in 60/40-like portfolios, making up only a small fraction of the assets held. But there has never been a better time over the last 30 years to revisit this shibboleth of low-inflation regimes.

Tyler Durden

Thu, 10/12/2023 – 09:35

gold

inflation

commodities

commodity

correlation

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}