Economics

Watch Live: Fed Chair Powell Testifies To House Financial Services Committee

Watch Live: Fed Chair Powell Testifies To House Financial Services Committee

Following his hawkish testimony yesterday before the Senate Banking…

Watch Live: Fed Chair Powell Testifies To House Financial Services Committee

Following his hawkish testimony yesterday before the Senate Banking Committee, Fed Chair Powell will fulfill the second part of his semiannual ‘Humphrey-Hawkins’ appearance before Congress by meeting with the House Financial Services Committee today.

The question on everyone’s lips is – after yesterday’s market chaos, will Powell try to walk back some of the hawkishness?

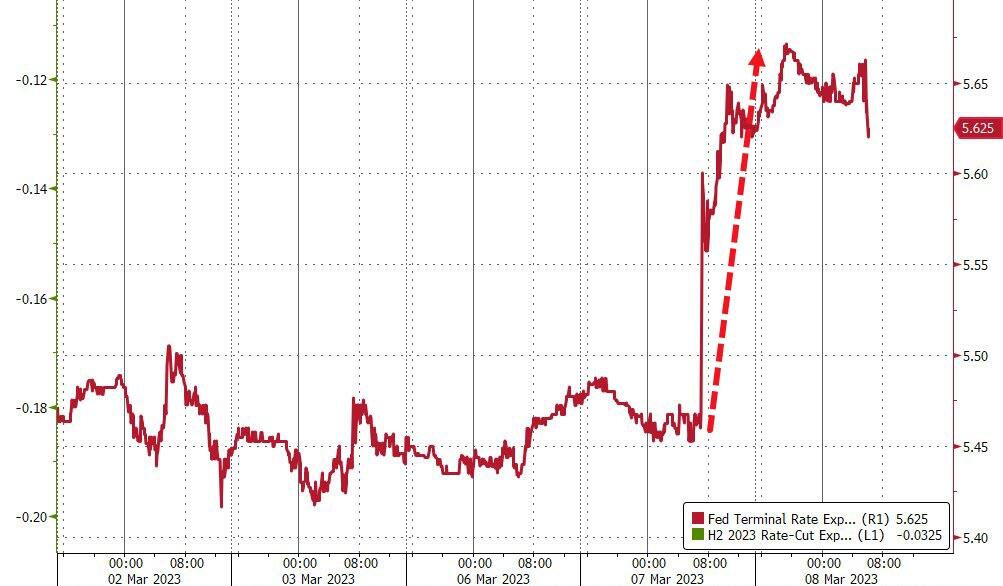

The simple answer is ‘no’ since the great majority of what spooked the market was in his prepared remarks (see below).

For now we note the market’s terminal rate is about 5.65% (up from 5.47% before the hearing began)…

Interestingly, the 10Y yield has given back all of yesterday’s spike… and then some…

Finally, this is Patrick McHenry’s first hearing as Chair of the committee and we have to say we are going to miss Maxine Waters running the show (she is still Ranking Member on the committee, so don’t be too sad).

Watch Powell’s tight-rope-walking testimony live here (due to start at 1000ET):

Read Powell’s prepared remarks (the same as yesterday’s) here: (emphasis ours)

Chairman Brown, Ranking Member Scott, and other members of the Committee, I appreciate the opportunity to present the Federal Reserve’s semiannual Monetary Policy Report.

My colleagues and I are acutely aware that high inflation is causing significant hardship, and we are strongly committed to returning inflation to our 2 percent goal. Over the past year, we have taken forceful actions to tighten the stance of monetary policy. We have covered a lot of ground, and the full effects of our tightening so far are yet to be felt. Even so, we have more work to do. Our policy actions are guided by our dual mandate to promote maximum employment and stable prices. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of labor market conditions that benefit all.

I will review the current economic situation before turning to monetary policy.

Current Economic Situation and Outlook

The data from January on employment, consumer spending, manufacturing production, and inflation have partly reversed the softening trends that we had seen in the data just a month ago. Some of this reversal likely reflects the unseasonably warm weather in January in much of the country. Still, the breadth of the reversal along with revisions to the previous quarter suggests that inflationary pressures are running higher than expected at the time of our previous Federal Open Market Committee (FOMC) meeting.

From a broader perspective, inflation has moderated somewhat since the middle of last year but remains well above the FOMC’s longer-run objective of 2 percent. The 12-month change in total personal consumption expenditures (PCE) prices has slowed from its peak of 7 percent in June to 5.4 percent in January as energy prices have declined and supply chain bottlenecks have eased.

Over the past 12 months, core PCE inflation, which excludes the volatile food and energy prices, was 4.7 percent. As supply chain bottlenecks have eased and tighter policy has restrained demand, inflation in the core goods sector has fallen. And while housing services inflation remains too high, the flattening out in rents evident in recently signed leases points to a deceleration in this component of inflation over the year ahead.

That said, there is little sign of disinflation thus far in the category of core services excluding housing, which accounts for more than half of core consumer expenditures. To restore price stability, we will need to see lower inflation in this sector, and there will very likely be some softening in labor market conditions. Although nominal wage gains have slowed somewhat in recent months, they remain above what is consistent with 2 percent inflation and current trends in productivity. Strong wage growth is good for workers but only if it is not eroded by inflation.

Turning to growth, the U.S. economy slowed significantly last year, with real gross domestic product rising at a below-trend pace of 0.9 percent. Although consumer spending appears to be expanding at a solid pace this quarter, other recent indicators point to subdued growth of spending and production. Activity in the housing sector continues to weaken, largely reflecting higher mortgage rates. Higher interest rates and slower output growth also appear to be weighing on business fixed investment.

Despite the slowdown in growth, the labor market remains extremely tight. The unemployment rate was 3.4 percent in January, its lowest level since 1969. Job gains remained very strong in January, while the supply of labor has continued to lag.1 As of the end of December, there were 1.9 job openings for each unemployed individual, close to the all-time peak recorded last March, while unemployment insurance claims have remained near historical lows.

Monetary Policy

With inflation well above our longer-run goal of 2 percent and with the labor market remaining extremely tight, the FOMC has continued to tighten the stance of monetary policy, raising interest rates by 4-1/2 percentage points over the past year. We continue to anticipate that ongoing increases in the target range for the federal funds rate will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In addition, we are continuing the process of significantly reducing the size of our balance sheet.

We are seeing the effects of our policy actions on demand in the most interest-sensitive sectors of the economy. It will take time, however, for the full effects of monetary restraint to be realized, especially on inflation. In light of the cumulative tightening of monetary policy and the lags with which monetary policy affects economic activity and inflation, the Committee slowed the pace of interest rate increases over its past two meetings. We will continue to make our decisions meeting by meeting, taking into account the totality of incoming data and their implications for the outlook for economic activity and inflation.

Although inflation has been moderating in recent months, the process of getting inflation back down to 2 percent has a long way to go and is likely to be bumpy. As I mentioned, the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes. Restoring price stability will likely require that we maintain a restrictive stance of monetary policy for some time.

Our overarching focus is using our tools to bring inflation back down to our 2 percent goal and to keep longer-term inflation expectations well anchored. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run. The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

To conclude, we understand that our actions affect communities, families, and businesses across the country. Everything we do is in service to our public mission. We at the Federal Reserve will do everything we can to achieve our maximum-employment and price-stability goals.

Thank you. I am happy to take your questions.

* * *

As we detailed earlier, it’s not just a very busy week for markets and economic releases: it is also a busy week is on tap for policy events. Fed Chairman Powell will testify before Congress regarding monetary policy but is likely to face numerous questions on economic policy as well as financial regulation.

Also, as Stifel’s Chief Washington Policy strategist Brian Gardner notes, financial regulators will speak publicly this week on digital assets. Elsewhere, the White House will release President Biden’s FY2024 budget on Thursday. Investors should discount headlines following the budget’s release. Presidents’ budgets are typically DOA and this one is likely to be no different. Lastly, President Biden indicated that he will sign legislation to block changes to Washington DC’s criminal code. This provides a clue regarding future prospects for action on China tariffs.

Below we look at these in sequence:

Powell on Capitol Hill

Federal Reserve Chairman Jerome Powell will testify before Congress twice this week. First, Powell will appear before the Senate Banking Committee on Tuesday and before the House Financial Services Committee on Wednesday. While the stated purpose of his appearances is to deliver the Fed’s semi-annual monetary policy report, numerous questions will be asked about bank regulatory issues.

In her preview, Bloomberg chief economist Anna Wong says she expects Powell to signal the Fed is ready to push rates higher than December’s dot plot indicated if inflation prints continue to exceed expectations, underscoring the FOMC’s resolve to get inflation under control. At the same time, he’ll acknowledge that the Fed’s dual mandate includes full employment, and that he retains hopes of achieving a soft landing for the economy.

Here is what else Bloomberg expects:

-

Powell will provide his read on the latest, confusing trove of economic data. Recent labor-market data have been strong, but the signal has been clouded by weather-related volatility.

-

Powell will emphasize that the most important takeaway from recent data is that taming inflation requires a sustained effort. Whether the peak rate ultimately will be 5.25% or 5.5% won’t make a major difference for the economy. What matters more is that inflation is proving sticky and isn’t likely to disappear unless the Fed keeps monetary policy restrictive well into next year.

-

Bloomberg Economics’ Fed spectrometer rates Powell as one of the more hawkish individuals on the FOMC. It’s possible he may endorse the recent upward shift in market pricing of the terminal rate to 5.5% – higher than the 5.25% indicated in the December dot.

-

More likely is that Powell will say policymakers still haven’t determined the ultimate destination of rates – consistent with what other Fed officials have said in recent speeches. That decision will depend on incoming data – and February’s nonfarm payrolls report (March 10) and CPI data (March 14) will be critical.

-

Regarding speculation of a 50-basis-point hike at the March meeting, Powell is likely to say everything is on the table, but will hint that the bar to re-accelerate the rate-hike pace is high. BBG’s baseline is that the Fed will hike by 25 bps in March, followed by another 25 bps in May, and then pause.

-

Republican lawmakers may question whether the Fed is behind the curve again, citing the easing in financial conditions since October 2022. Powell will likely push back on the idea that financial conditions have loosened. He may argue that, as in the Monetary Policy Report he submitted ahead of the testimony, “financial conditions have tightened further since June and are significantly tighter than a year ago.”

-

The Monetary Policy Report cited various metrics showing tightened financial conditions: Bond yields have risen across maturities; issuance of leveraged loans and speculative-grade corporate bonds slowed substantially in 2H22; business loans at banks decelerated in the fourth quarter; indicators of future business defaults are elevated; delinquency rates of credit cards and auto loans rose.

-

That explains why Powell said in his press conference after the February FOMC that financial conditions had tightened — even as indexes of financial conditions that markets watch had loosened at the time.

Stifel’s Gardner adds several secondary things to keep an eye for:

-

in a recent speech, Federal Reserve Vice Chairman for Supervision Michael Barr cited academic studies which found that bank capital requirements are too low. Committee members could ask Powell about whether he agrees with this assessment.

-

In the past, Chairman Powell has said that he would look for political support from Congress and the administration about whether the Fed should create a Central Bank Digital Currency (CBDC). Committee members are likely to revisit the topic of a CBDC as well as the regulation of digital assets, particularly Stablecoins and bank liquidity requirements. U.S. banking regulators recently issued a “Joint Statement on Liquidity Risks to Banking Organizations Resulting from Crypto-Asset Market Vulnerabilities” and Powell is likely to be asked about the statement.

-

Committee members could also ask Powell about bank mergers. Questions will likely not mention specific transactions but there could be questions about a review of bank merger rules as well as why there has been an increase in the time to dispose of bank merger applications.

-

Federal Reserve Chair Jerome Powell provides his semi-annual testimony to the Senate Banking Committee on March 7, and addresses the House Financial Services Committee the following day.

* * *

Besides Powell’s testimony, there will be several other political events to keep an eye on:

Crypto Events

In addition to Chairman Powell’s appearance on Capitol Hill, which will probably include Q&A on cryptocurrencies, several other regulators will speak in public this week on digital assets.

- Wednesday

- CFTC Chairman Rostin Behnam testifies at a CFTC oversight hearing in Senate Agriculture Committee.

- Thursday

- Fed Vice Chairman for Supervision Barr will give remarks on crypto activities to the Peterson Institute.

Biden Budget

On Thursday, the White House will release President Biden’s FY2024 budget. As a reminder to investors, budgets are loaded with policy proposals, most of which will never see the light of day. This budget will likely be no different.

The President’s State of the Union address previewed several tax proposals that are likely to be included in the budget including taxes on unrealized capital gains and an increase in the stock buyback tax. The proposal to tax unrealized capital gains will be DOA. Although an increasing number of Republicans have criticized the use to stock buybacks, GOP critics of buybacks are still a minority within the party. There seems to be insufficient support among Republicans to raise the buyback tax, so chances of the House even voting on the Biden proposal appear to be remote.

Vote on DC Crime Bill and Read Through to China Tariffs

Last week, President Joe Biden announced that he would not veto congressional legislation to overturn the changes to Washington DC’s criminal code which would reduce penalties for some violent crimes. (The City Council has subsequently announced it will withdraw the planned revisions). President Biden’s decision reflects a political strategy to not allow Republicans to paint him as soft on crime ahead of the 2024 election. Although there are no direct market implications from the president’s decision, this move will likely be repeated regarding policies towards China, including the extension of the Trump administration’s tariffs on Chinese imports.

As we have previously written, the two political parties are engaged in a competition on which party can be seen as toughest on China. Just as Biden does not want to be painted as “soft on crime”, he also does not want to be painted as “soft on China”. The announcement on the DC crime bill reinforces the view that the administration will likely extend most, if not all, of the 2018 tariffs on Chinese imports.

Tyler Durden

Wed, 03/08/2023 – 09:50

inflation

monetary

markets

reserve

policy

interest rates

fed

central bank

monetary policy

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…