Economics

US Stocks Lead Global Markets In 2023 As Various Risks Simmer

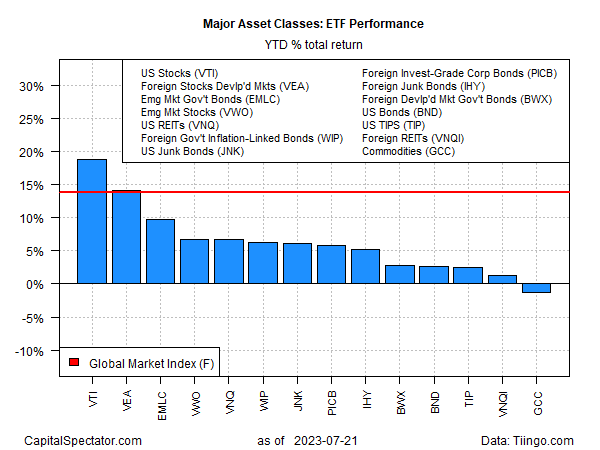

American shares remain firmly in the lead for the major asset classes year to date, based on a set of ETF proxies through Friday’s close (July 21). Markets…

American shares remain firmly in the lead for the major asset classes year to date, based on a set of ETF proxies through Friday’s close (July 21). Markets generally are posting solid gains in 2023 but various risk factors will pose a stress test for the bull run in the second half.

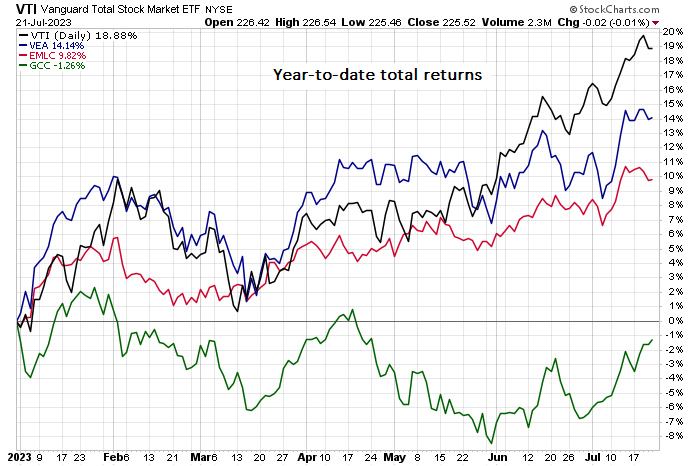

Year to date, however, the trend certainly looks rosy. All the major slices of global markets — except commodities – are enjoying positive returns. US stocks continue to hold the commanding height via Vanguard Total US Stock Market Index Fund (VTI), which is ahead nearly 19% in 2023.

In second place: stocks in developed markets ex-US (VEA). A surprise third-place performer to date in 2023: government bonds issued in emerging markets. VanEck JP Morgan EM Local Currency Bond ETF (EMLC) is up nearly 10% this year, in part due to a flat/weaker US dollar, which translates into higher prices for foreign assets after converting from various currencies into greenbacks.

A broad measure of commodities (GCC) remains the only downside outlier with a modest 1.3% year-to-date loss.

The Global Market Index (GMI.F) is posting a robust year to date increase of 13.8%. This unmanaged benchmark holds all the major asset classes (except cash) in market-value weights via ETFs and represents a competitive measure for multi-asset-class-portfolio strategies.

The rallies to date paint an upbeat profile from a momentum perspective, but various macro threats are lurking that could create new headwinds for the bulls. First up is another interest rate hike that’s expected at Wednesday’s Federal Reserve policy announcement (July 26). Although inflation continues to show signs of easing, some economists warn that the end game for policy tightening still isn’t imminent. In turn, it’s not clear that markets have priced in the possibility that interest rates could continue to rise beyond the Fed’s expected hike on Wednesday.

“While things seem to be heading in the right direction with inflation, we are only at the start of a long process,” says Karen Dynan, an economist at Harvard University.

Markets are arguably pricing in high odds for a so-called soft landing. Although there’s support for this view, it’s hardly overwhelming. This Thursday’s release (July 27) of the government’s first estimate of second quarter US GDP could be a key number for tilting the calculus one way or the other. The consensus forecast sees output easing to a 1.5% increase, down from 2.0% in Q1 (seasonally adjusted annual rate), according to Econoday.com.

The disappointing rebound in China’s recovery this year after reopening from its Covid lockdown is a headwind for the US and the global economy. “Slow growth in China can have some negative spillovers for the United States,” warns Treasury Secretary Janet Yellen.

There’s also the slow grind of Russia’s war on Ukraine, which continues to reverberate around the world. Markets have generally learned to live with the chaos and blowback, but the potential for negative surprises endures as both sides become increasingly incentivized for a breakthrough from the attrition war that currently prevails.

To date, markets are climbing a wall of worry and appear to be looking through the various risks that swirl. There’s a case for assuming that the second half of the year will bring more of the same and prices will be flat to modestly higher. But with many markets now well above their 2022 lows, the margin for negative surprises has faded by more than a trivial degree. In turn, the odds may be higher that we’ll see markets consolidate recent gains in the months ahead with some backing and filling.

The bigger question is whether the resilience of US and global economic activity is weaker and less robust than it seems? The incoming July numbers will serve as a stress test. Meantime, it seems plausible that markets will be more inclined to stay cautious before deciding that it’s timely to extend the recent bull run. The economic numbers, in short, will likely play a more decisive role in market sentiment going forward.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

dollar

inflation

commodities

markets

reserve

policy

interest rates

fed

us dollar

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…