Economics

US Q2 GDP Nowcasts Point To Pickup In Growth

The risk of recession remains elevated, according to several indicators, but the soft-landing scenario isn’t dead. Support for the relatively upbeat…

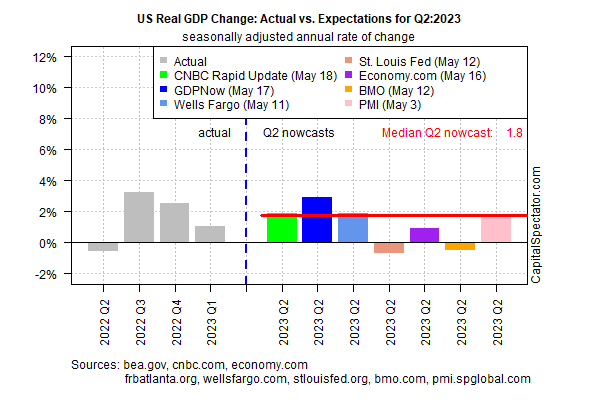

The risk of recession remains elevated, according to several indicators, but the soft-landing scenario isn’t dead. Support for the relatively upbeat outlook includes estimates for second-quarter economic activity, based on current GDP nowcasts via data compiled by CapitalSpectator.com.

The median estimate for Q2 is a 1.9% rise. That’s a modest pace, but it’s above the weak 1.1% increase reported for Q1. The caveat is that it’s still early in the quarter and so most of the Q2 numbers have yet to be published. There’s a long road ahead until the Bureau of Economic Analysis publishes its initial Q2 estimate on July 27. The main risk factor at the moment: uncertainty about the timing of legislation that sidesteps the brewing debt-ceiling crisis. Assuming that gets resolved, there’s a plausible case for expecting that economic activity will pick up in the current quarter.

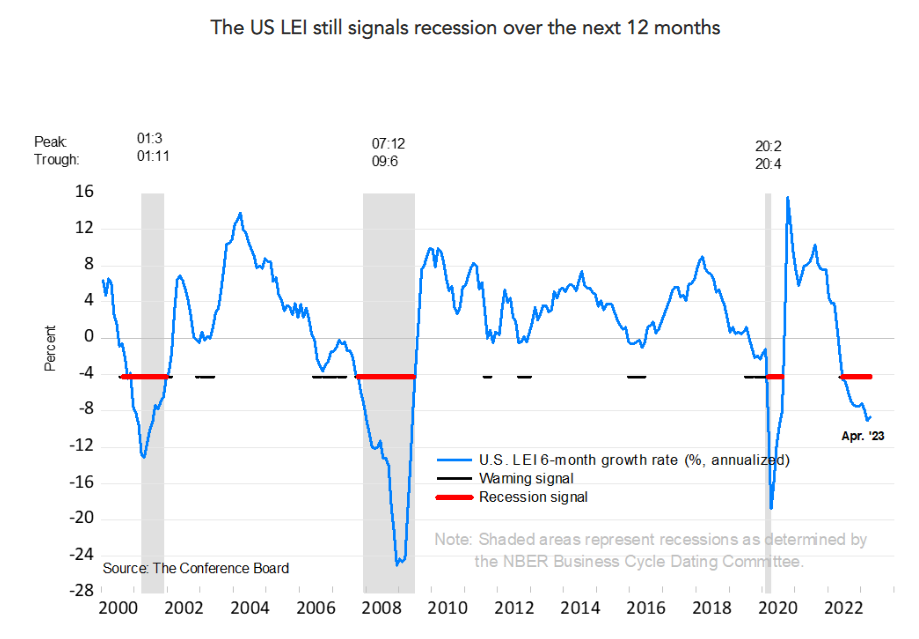

Looking further out carries more uncertainty, as always. Yesterday’s release of the Leading Economic Index (LEI) for April predicts that a US recession is a high risk as the year progresses.

“The LEI for the US declined for the thirteenth consecutive month in April, signaling a worsening economic outlook,” says Justyna Zabinska-La Monica at The Conference Board. “Weaknesses among underlying components were widespread—but less so than in March’s reading, which resulted in a smaller decline. Only stock prices and manufacturers’ new orders for both capital and consumer goods improved in April. Importantly, the LEI continues to warn of an economic downturn this year. The Conference Board forecasts a contraction of economic activity starting in Q2 leading to a mild recession by mid-2023.”

The current median Q2 nowcast suggests otherwise. The stock market seems to agree, although this is always a dicey forecasting tool. In any case, animal spirits are improving. The S&P 500 Index closed on Thursday (May 18) at a nine-month high. It’s premature to conclude that last year’s correction is over and that new highs are on the horizon, but recent trend behavior moves us closer to that view.

The challenge is that a recession of some degree is still a credible scenario in the near term. A key factor that could tip the scales one way or the other: the path of monetary policy. If the Fed is poised to end its rate hikes by pausing at the next FOMC policy meeting on June 14, which the market expects, the news will strengthen the case for a soft landing with growth muddling onward.

Even better for the bulls: the Fed starts cutting rates later in the year, which some analysts are predicting. Fed funds futures are pricing in modest odds for a pause in rate hikes starting in June, followed by a rate cut, possibly as early as September with slightly higher odds for easing i November.

The Fed’s “not going to stick to their [rate-hiking] guns,” predicts Joe LaVorgna, chief US economist for SMBC Group and formerly an economic advisor in the Trump administration. “There’s no way they’re going to be able to sit and watch [employment] come down” if job losses rise.

But there’s a feedback loop to consider. If payrolls decline more than expected, and inflation continues to ease, the Fed may be persuaded that it can pause. Bullish surprises for the labor market that support economic activity, and/or sticky inflation data, on the other hand, could push the Fed to continue raising rates, which in turn might raise the odds of a recession.

Deciding which scenario has higher odds remains challenging, but this much is clear: the early estimates via GDP nowcasts suggest that an NBER-defined recession isn’t likely to start in Q2. The rest of the year, by contrast, is still open for debate and dependent on the incoming numbers.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…