Economics

There’s No Housing Crash Coming

The worst housing affordability in decades … but don’t expect a crash … why prices will stay high … ways to invest … watch out for the social…

The worst housing affordability in decades … but don’t expect a crash … why prices will stay high … ways to invest … watch out for the social implications … similar to The Technochasm

Housing affordability is the worst it’s been in nearly 35 years.

From Bloomberg last Friday:

The National Association of Realtors index decreased to 91.7 in August, marking the lowest level in data back to 1989, according to data out Friday.

A level below 100 means a household with a median income doesn’t earn enough to qualify for a mortgage on a median-priced home.

Now, let’s jump straight to punchline with three broad takeaways:

First, don’t expect a crash anytime soon. It’s not coming. At best, we’ll see a slow leak in prices, like air gradually escaping a small tire puncture. At worst, there’s another price melt-up on the way.

Second, given the deterioration of our government’s financial position, if you can put money into rental real estate as a portfolio diversifier, it would be a wise move.

Third, the thornier issue is how this housing unaffordability is just another manifestation of the widening division between the “haves” and “have nots” in our nation. We’re increasingly polarized politically, socially, and economically. History shows this rarely ends well.

In the meantime, if you can position your wealth to benefit from this trend – destabilizing though it may be – you’ll be in far better shape to avoid the great financial bleed-out that most Americans are going to suffer in the coming years.

Let’s look at each in more detail.

Sorry, but housing won’t be crashing

I only remember one thing from the class I took in college about Dante Alighieri’s medieval classic, Divine Comedy. It’s the command engraved above the Gate of Hell:

“Abandon all hope, ye who enter.”

This doubles as good advice for would-be homebuyers entering today’s housing market.

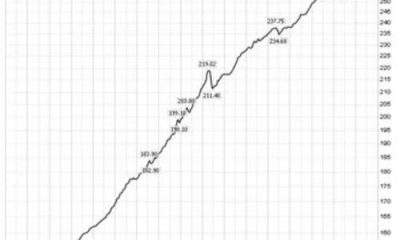

As you can see below, according to the S&P/Case-Shiller U.S. National Home Price Index, housing prices are 46% more expensive than they were in January 2020. Plus, the index recently eclipsed its prior high from June 2022.

Source: Federal Reserve data

Adding insult to injury, as of last Friday, the average 30-year fixed rate mortgage came in at 8.09%.

It’s easy to see why housing affordability is in the worst condition in decades.

Unfortunately, it won’t be improving significantly anytime soon

We no longer have a highly-liquid, dynamic national housing market. Homeowners who are mostly unwilling to sell are keeping inventories tight. So, only a handful of existing homes are on the market at any given time.

Meanwhile, though an increasing number of would-be homebuyers are now priced-out of the market, there remain enough deep-pocketed buyers to bid up the prices of these handful of homes for sale. Together, low supply and high demand are acting as a buoy to prices.

So, how does this play out?

Well, at the current trajectory, nothing changes. Rabid buyers will pounce on the slow leak of existing homes trickling out for sale. This will keep prices at existing levels, or even higher.

If the Fed cuts rates next year, it potentially makes the problem worse because the Fed isn’t going to slash rates. Perhaps we’ll get 100 basis points of cuts. Let’s guess that pushes down the 30-year fixed rate mortgage from 8% to 6.5% or 7%.

Although some additional homeowners will be prompted to list their properties, it won’t be enough to flood the market with new homes. But you know what will the flood the market? Homebuyers salivating at the prospect of slightly greater affordability.

So, this massive influx of would-be homebuyers will cause prices to remain high – or rise even higher.

In fact, until mortgage rates fall to roughly 4% – 5%, any affordability gains that would-be homebuyers would enjoy from reduced financing costs will be offset by increases in home prices themselves, as hopeful buyers out-bid each other for the scant housing inventory hitting the market.

Here’s Barbara Corcoran, real estate entrepreneur and star of ABC’s “Shark Tank”:

The minute those interest rates come down, all hell’s going to break loose, and the prices are going to go through the roof. [Right now, sellers are] staying put. But they’re not going to stay put if interest rates go down by two points.

It’s going to be a signal for everybody to come back out and buy like crazy, and the house prices [will likely] go up by 20%. We could have COVID [market] all over again.

The only way we’ll see a serious correction in home prices is if a recession forces the Fed to slash rates, which would similarly slash mortgage rates. Plus, during a recession, many homeowners would be forced to sell their homes, flooding the market with new inventory.

Barring that outcome, don’t bet on materially lower prices.

Given this forecast, coupled with the deteriorating condition of our government’s financial condition, are you able to invest in real estate?

In recent Digests, we’ve talked at length about the U.S. government’s unsustainable financial trajectory.

It owes more money to its creditors than it could ever hope to pay back… it’s promising an ever-expanding laundry list of costly entitlements and programs… and it has zero ability to pay for all these financial obligations on its current trajectory.

So, you can count on three things happening in the coming years: higher taxes, more debt (via increased bond issuances), and increased currency debasement.

Part of our recommended defense against this triple-whammy on your wealth has been to invest in hard assets – and rental real estate fits the bill.

Traditionally, investing in rental real estate was limited to high-net-worth individuals who could afford expensive down-payments on properties.

Today, a handful of online platforms are changing this. These platforms offer fractional ownerships in residential and commercial real estate either through investments in specific homes or commercial developments, or a fund with exposure to a broad portfolio of properties (similar to a private REIT).

It’s a passive way to be a rental real estate owner without having to know all the details of a specific, localized market, and without the hassle of vetting tenants or, say, getting a call to replace a broken hot water heater at 2PM on a Saturday when you’re on the golf course.

Three of the most popular platforms are CrowdStreet, RoofStock, and FundRise. They vary by required investment size, fees, type of investment property available to investors, and whether they require accreditation, among other differences.

We have no affiliation with any of these companies, so please conduct your own due diligence. And if you have personal experience with one and you’d like to recommend it to our broad readership, email us at [email protected].

Bottom line: If you can get you into quality, income-producing real estate that enables you to benefit from both capital- and rental-appreciation, it will be a powerful step toward wise portfolio diversification.

Finally, be aware of the broader societal implications

Here’s Lawrence Yun, chief economist of the National Association of Realtors:

The highest mortgage rate in two decades is detrimentally limiting the homeownership opportunity for many middle-class households.

Unintentionally, no doubt, the Federal Reserve is widening social inequality with only the high-income families — earning above $100,000 — able to comfortably buy a home.

Yun is referencing a national average. If you want to live in a big city, you’d better earn way more than $100K.

Here’s mortgage company HSH with its analysis of the minimum salary you need to own a home in the following cities:

- Washington, D.C. – $157,076.86

- Denver – $161,129.53

- Boston – $186,926.95

- Los Angeles – $192,926.74

- Seattle – $193,037.07

- San Diego – $225,646.30

- San Jose – $431,128.22

I live in Los Angeles, and I can tell you that its $192K salary requirement isn’t even in the ballpark of what you’d need to buy a home in many of the safer neighborhoods. In the neighborhood where I rent, the median listing price is $3.2 million, up 25% from one year ago.

Stepping back, what we’re watching in real time is the fracturing of our society. Those who were wealthy enough to own homes a few years ago are now sitting on significant capital gains and a marked leap in personal net worths. Those who couldn’t afford homes are now even further out of range.

As this decade brings more dollar debasement, this financial chasm will widen even further. Those Americans with financial assets will watch the nominal values of those assets race higher – their quality of life will remain as is or improve. Meanwhile, those without financial assets will slip further behind as their dollars buy less and less and their living standards decline.

History shows this doesn’t bode well for the future. Of course, there’s little you and I can do other than try to position ourselves appropriately.

If this sounds familiar, you might be recalling research from our macro investor Eric Fry on what he labeled The Technochasm

The Technochasm was Eric’s term to describe the stark — and expanding — wealth gap in the United States that’s, in large part, driven by technology.

On one hand, today’s technologies are wonderful — they make life far easier and more convenient. That’s why we’re all more than willing to open our wallets for new tech products and services.

But all these profits are flowing toward a highly-select few companies … and by extension, a highly-select group of owners, key employees, and investors.

And in doing so, it’s fueling this ever-growing, ever-widening wealth gap. This divide will only intensify with the introduction of Artificial Intelligence.

It’s beyond our scope today to dive into that topic, but everyone should recognize what’s coming. What we’re seeing in the housing market today is just another manifestation of the same core issue that’s driving The Technochasm.

So, whether it’s rental real estate or top-quality AI stocks, position yourself for the growing divide that’s already in progress. As the saying goes, let’s hope for the best but prepare for the worst.

By the way, if you missed Eric’s research video on The Technochasm, you can watch it here.

Have a good evening,

Jeff Remsburg

More From InvestorPlace

- Musk’s “Project Omega” May Be Set to Mint New Millionaires. Here’s How to Get In.

- ChatGPT IPO Could Shock the World, Make This Move Before the Announcement

- The Rich Use This Income Secret (NOT Dividends) Far More Than Regular Investors

The post Thereâs No Housing Crash Coming appeared first on InvestorPlace.

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…