Economics

The Fed Reduces Rate Hikes

The Fed downshifts to just 50 basis points … the higher terminal rates spooks investors … where do we go from here? … keep the spotlight on earnings

This…

The Fed downshifts to just 50 basis points … the higher terminal rates spooks investors … where do we go from here? … keep the spotlight on earnings

This afternoon, the Federal Reserve met expectations by raising rates only 50 basis points.

This was a downshift from the 75-basis-point hikes in the previous four meetings.

The Fed Funds target range is now 4.25% to 4.50%, the highest level in 15 years.

While the rate-hike size was expected, what caught Wall Street off guard was the increase in the expected “terminal rate,” or point where Fed officials expect to end rate hikes. Its upper range rose to 5.25% compared to only 4.75% in September.

As to the Fed’s plans beyond 2022, here’s CNBC:

The consensus then pointed to a full percentage point worth of rate cuts in 2024, taking the funds rate to 4.1% by the end of that year.

That is followed by another percentage point of cuts in 2025 to a rate of 3.1%, before the benchmark settles into a longer-run neutral level of 2.5%.

Beyond the higher terminal rate, what spooked Wall Street was the Fed’s lowered growth targets for 2023. It expects GDP gains of just 0.5%, barely above what would be considered a recession.

Finally, in his live press conference, Federal Reserve Chairman Jerome Powell didn’t give the bulls the dovishness they wanted.

From Powell:

The inflation data received so far for October and November show a welcome reduction in the monthly pace of price increases. But it will take substantially more evidence to give confidence that inflation is on a sustained downward path.

In response, stocks whipsawed all over the place.

Here’s a one-minute chart of the S&P 500 on the day, which ended down 0.60%.

Source: StockCharts.com

Source: StockCharts.com

So, where do we go from here?

Today’s news throws cold water on yesterday’s cooler CPI print that some interpreted as a coronation of a new bull market.

For example, yesterday, in reporting on the softer CPI number, CNBC quoted an economist whose reaction to the reading was: “Stick a fork in it, inflation is done.”

Many bulls agree and leapfrog to the idea that “good times are here again” for stocks. I doubt today’s news from the Fed will change that too much. Here’s the broad bullish narrative going forward:

- Yesterday’s CPI print means inflation has been conquered – from here on out, it will be a series of lower readings until we return to the Fed’s 2% goal in a relatively smooth fashion.

- Based on this conquered inflation, the Fed will soon be able to pause rate hikes, even though Powell didn’t expressly support that idea today.

- Also, thanks to conquered inflation, the economy will firm up and avoid a recession in 2023.

- Sometime in the second half of 2023, after inflation has fallen substantially, the Fed will begin cutting interest rates.

- Put it all together, and stocks are on the verge of a new, monster bull market.

Now, things could play out this way. But let’s evaluate this narrative in greater detail.

I bristle at the certainty of comments like “stick a fork in it, inflation is done”

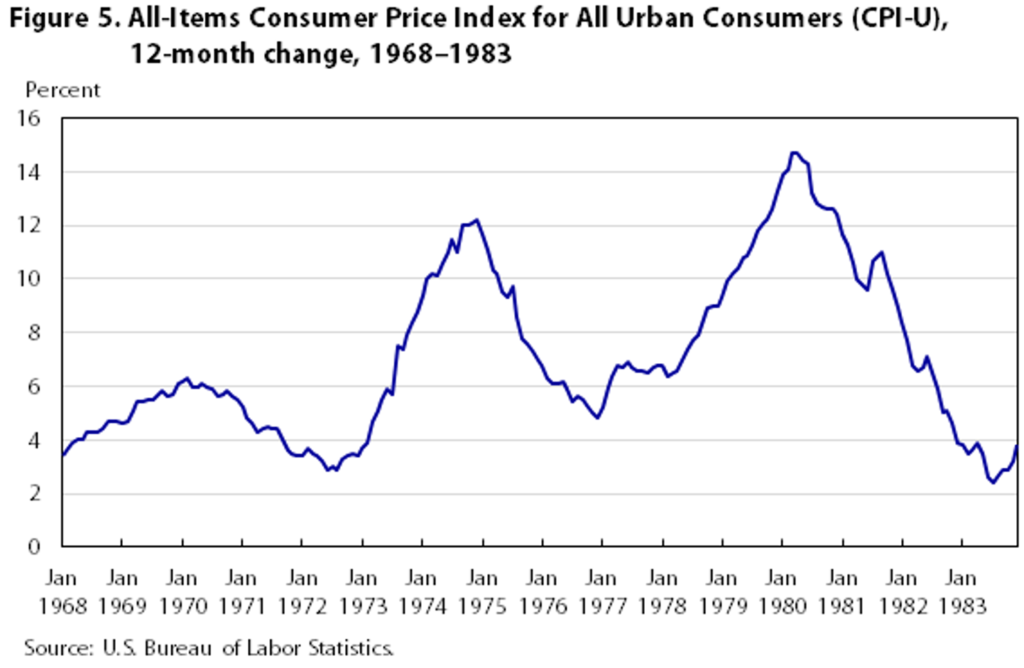

First, history has shown that inflation can return even after months of cooler readings. Look at the chart below of the CPI from 1968 through 1983 as evidence.

“Cooling inflation” doesn’t always equal “conquered inflation.”

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

But let’s ignore this fact. Instead, let’s say that we are, indeed, past peak inflation.

Two issues…

First, there’s a false binary at the heart of many bullish hopes today.

You see, “inflation is done” views this whole inflationary predicament through an either/or lens…

Either we remain in a world of nosebleed inflation in the 7% to 8% range, or we beat inflation, and quickly return to those oh-so-happy days of 2% inflation.

But it isn’t that simple

In the real world, there are more than two options.

What do we know about inflation?

Well, yes, it’s cooling – but much of that cooling is due to softer prices for gasoline and various consumer goods. But inflation is proving more stubborn when it comes to services.

From CNBC:

But inflation for “services” has proven “a bit stickier,” said [Andrew Hunter, senior U.S. economist at Capital Economics].

Labor costs are a big driver of inflation in the services sector, which might include anything from haircuts to hotel stays.

Demand for workers is near historic highs and the unemployment rate low, helping fuel competition for workers and therefore fast-rising wages — in turn feeding through to high labor costs to businesses, creating upward pressure on their cost of services.

And let’s pick up with economist and former-PIMCO-CIO Mohamed El-Erian:

Also worrisome is the morphing of the inflation process. No longer dominated by energy and food prices, the drivers of inflation are increasingly coming from the services sector.

Within that sector, the latest monthly US payrolls data showed wages gaining 0.6 per cent in November, twice the consensus forecast and taking the steadily increasing three-month moving average to 6 per cent.

This accelerating wage growth was accompanied with robust monthly job gains.

Persistently high job vacancies still outnumber the unemployed by a factor of 1.7 amid declining labor force participation.

So, if inflation continues cooling for the price of many goods, yet inflation for services continues rising, or simply doesn’t fall quickly, what happens to overall inflation?

Well, it’s certainly not a smooth return to 2%.

Back to El-Erian:

Rather than fall to 2-3 per cent by the end of next year, US core PCE inflation will probably prove rather sticky at around 4 per cent or above.

This is what happens when an inflationary moment is allowed to get embedded into the economic system.

Now, at his press conference this afternoon, Powell explicitly said that the Fed is not going to contemplate raising its 2% inflation goal.

If that’s the case, then we need to allow room for more economic pain next year as the Fed continues battling inflation.

You might say it’s now “2% or bust” – and mean it very literally.

A few moments ago, we said that even if elevated inflation is conquered, two issues remain…

The first was the false binary we discussed.

What’s the second issue?

Well, it’s no longer even about elevated inflation anymore.

Nosebleed inflation was 2022’s problem. I‘m happy to concede that this year’s super-high levels are behind us.

But the dynamic that will make or break 2023 is whether the Fed’s actions will tip the economy into a recession and drag down corporate earnings (to a level that’s far worse than what Wall Street predicts).

Part of how this plays out depends on factors the Fed can no longer control – specifically, the effect of all its prior rate-hikes that will hit the economy in 2023.

Another part of the answer depends on the Fed’s terminal rate, and how long it keeps it there in 2023. As we highlighted earlier, the news today is that the Fed has upwardly revised its expected terminal rate.

And then, part of the answer is based on Wall Street’s belief about 2023 earnings and the degree to which it’s on or off the mark.

On this last variable, in recent Digests, we’ve walked through why current earnings forecasts for 2023 are likely too high

We won’t repeat those points in today’s Digest.

Instead, let’s assume 2023 earnings are flat – no growth, but no recessionary contraction either.

Well, if that’s the case, for 2023 to bring a rip-roaring bull market, it points us toward the multiple that investors are willing to pay for earnings – this is a proxy for investor sentiment.

As I write, the S&P 500 has a price-to-earnings (P/E) multiple of 21, which is 31% higher than its long-term average of 16.

Rip-roaring bull markets tend to begin at far humbler P/E multiples, not ones that are already 31% pricier than average.

But if a new bull market is about to begin – without the help of strong 2023 earnings – this above-average P/E will have to become way, way, above average.

To be fair, the bullish path forward might happen

My cautious perspective could be wrong – I’ve been around the markets long enough to recognize that humility is critical to avoid getting your face ripped off.

But if the bull path forward we’ve considered today is going to play out, a lot of things have to go just right, and the Fed has to be bluffing about its path forward.

Bottom line: Yes, inflation is dropping… yes, we’re closer to the end of all this than the beginning… and yes, by this time next year, I believe the market will be on a true bullish ascent (though I don’t know from what market low) …

But a “stick a fork in it” attitude today feels just a bit too certain in the face of 2023 market conditions that are anything but certain.

Have a good evening,

Jeff Remsburg

The post The Fed Reduces Rate Hikes appeared first on InvestorPlace.

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…