Economics

Snowflake: Don’t Let The Insane Stock-Based Compensation Fool You

The stark contrast between tech stock valuations in 2022 vs 2021 has been a welcomed development for those of us in the camp that is quite sensitive to…

The stark contrast between tech stock valuations in 2022 vs 2021 has been a welcomed development for those of us in the camp that is quite sensitive to earnings multiples when making investment decisions. As share prices across the sector started to collapse I was eager to step in for long-term holding periods even though I knew the bottom would likely be below my initial entry point. Now that the shakeout has occurred, there are many bargains, but not everything is cheap.

I was struck by an interview on CNBC yesterday with Brad Gerstner, who runs a tech-focused hedge fund called Altimeter Capital. Brad has been super bullish on Snowflake (SNOW) since the IPO given the company’s strong competitive position in a fast growing market. What I found odd was that as the market shifted away from the idea that almost any price can be paid for the best growth, Altimeter didn’t shift its positioning. SNOW was the fund’s largest holding when it reached $400 in 2021 and traded for 100 times sales and it remains so today with the shares at $150 (a meager 28 times sales).

During the same interview Gerstner made the compelling argument that in a highly inflationary economic climate with rising interest rates the market will not reward companies that seek growth over profitability any longer. Oddly, he then turned right around and pounded the table on SNOW because the valuation has compressed so much (from insane, to just extremely rich, I might add).

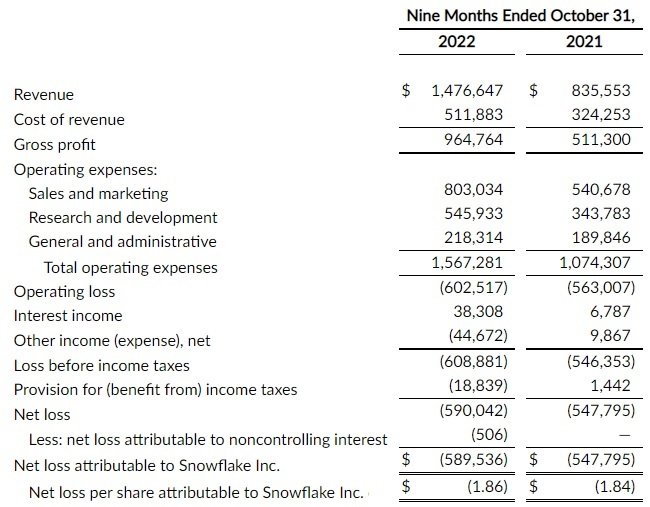

He repeatedly pointed to SNOW’s free cash flow growth, which he expects to double from $350 million in 2022 to $700 million in 2023. That would seem to imply that SNOW is indeed one of the tech firms that has pivoted from growth to profitability and thus may deserve a high sales multiple due to high profit margins. The problem is that SNOW’s income statement is littered with red ink. Take a look at their financial results from the first three quarters of 2022:

No, you are not misreading that income statement. So far this year SNOW’s revenue has grown by more than 75% and its net loss increased. Pre-tax profit margins are negative 41%.

So how on earth is SNOW reporting positive free cash flow, to the tune of hundreds of millions annually, when in reality it is bleeding red ink on the books? Well, they have learned that the key to getting their large investors to buy into crazy valuations is to generate cash even when you have accounting losses. And the only way to do that is to pay the vast majority of your compensation in stock and not cash.

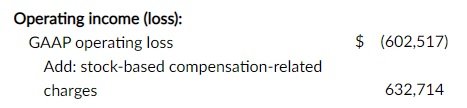

Here is SNOW’s stock-based comp figure for the first 9 months of 2022:

$633 million! That equates to 40% of total operating expenses! No wonder it’s so easy for a large investor in your company to go on television and rave about your free cash flow generation. You are excluding 40% of your expenses from the equation!

Now, let me be clear. Snowflake’s market position is very strong; nobody is refuting that. This funding strategy says nothing about the company, other than how it is doling out shares and then ignoring that fact when it discussed profitability. The company is not profitable today, which makes a near-30x sales multiple look silly.

That said, they will make money at some point. With gross margins rising and approaching 70% right now, the business could easily earn 20% net margins in the future once they get their cost base in-line with other more mature software firms. Those future margins could command a valuation above the market overall (a 30x P/E with 20% margins implies a 6x sales multiple).

Bur the reality today is that the company is growing without any regard to expenses and the only way it is worth this price is if everything goes wonderfully for the next 5-10 years. Many believe that will happen. Gerstner claimed in his interview that SNOW will grow free cash flow 50% annually for many years and that the valuation will stay where it is today – for a total stock return of 50% annually over the same period. Neither of those seem like reasonable hurdles to clear in my eyes, but we’ll have to see how it plays out.

Bottom line: don’t get fooled into thinking that in tech land “free cash flow = profitability.” Normally it does, but not when you use stock-based compensation to a degree never seen in prior economic cycles (not even in Silicon Valley). And for investment managers who don’t hesitate to make their largest position something fetching 100 times revenue, ask yourself if that’s is what history says is a wise move financially, or if more likely that was what their investor base at the time wanted – and thus they had to figure out a way to justify doing it. Why they are still sticking to their guns is a question I can’t answer.

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…