Economics

Should The Fed Declare Defeat And Move On?

Should The Fed Declare Defeat And Move On?

Authored by Mike Shedlock via MishTalk.com,

The Wall Street Journal author Jason Furman fires…

Should The Fed Declare Defeat And Move On?

Authored by Mike Shedlock via MishTalk.com,

The Wall Street Journal author Jason Furman fires the opening salvo by mainstream media pleading for higher inflation targets…

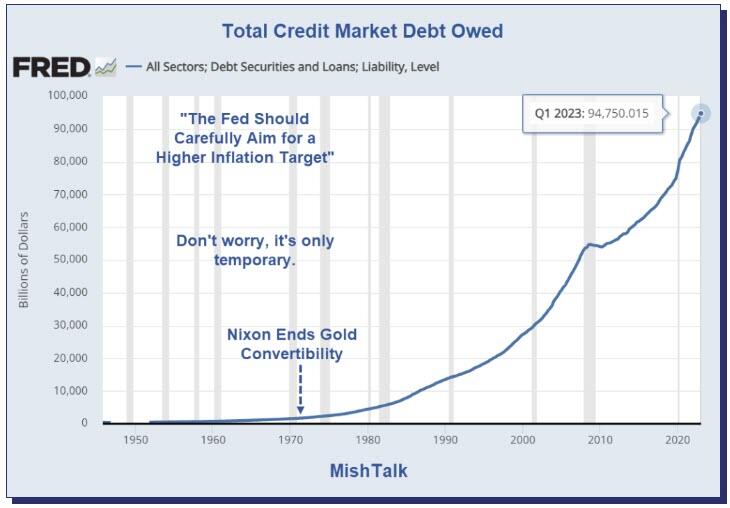

Total Credit Market Debt Owed courtesy of the Fed, annotations by Mish

The Fed Should Carefully Aim for a Higher Inflation Target

Please consider The Fed Should Carefully Aim for a Higher Inflation Target by WSJ author Jason Furman

The Federal Reserve has appropriately focused on a single objective for a year and a half: getting inflation down. While the war isn’t won, and I fear the hardest battles may be ahead, it is necessary to think about what victory would entail. In the short run, the Fed should be aiming to stabilize inflation below 3%. If it can achieve this goal, then it should shift to a higher target range for inflation when it updates its overall strategy around 2025.

If the Fed were adopting an inflation target from scratch, it would likely choose a target above 2%. A higher target inflation rate has costs, especially the time and attention people spend trying to account for how much their current dollars will be worth in a year or 10. But a higher target also has the benefit of helping cushion the economy against severe recessions.

If the Fed were adopting an inflation target from scratch, it would likely choose a target above 2%. The Fed, however, isn’t starting from scratch. The 2% inflation target, which was formalized in 2012 and has been reiterated innumerable times, has had some real benefits. People expected inflation around 2%, and for the most part that’s what they got. If inflation expectations hadn’t been so well anchored, the disinflation over the past year would have been much more painful.

There are two prerequisites for a successful transition. The first is to make clear that the Fed isn’t raising the inflation target merely to avoid the pain of getting inflation down. The second prerequisite is that if the Fed raises the inflation target, it needs to stick with it. It wouldn’t work to announce, say, a new target range for inflation of 2% to 3% and end up with 3.5% inflation. It would threaten the Fed’s credibility.

Mr. Furman, a professor of the practice of economic policy at Harvard, was chairman of the White House Council of Economic Advisers, 2013-17.

No Benefit to Inflation

There is no economic benefit to inflation. However, it does create winners and losers, with the winners being those with first access to money, especially the banks, the politically well connected, and the already wealthy.

I have discussed this many times before but it’s worth repeating again. Routine consumer price deflation is a benefit. It’s credit deflation resulting from the bursting of asset bubbles that is very damaging.

That’s not just my opinion, it’s the opinion of the Bank of International Settlements (BIS).

Historical Perspective on CPI Deflations: How Damaging are They?

For discussion, please see Historical Perspective on CPI Deflations: How Damaging are They?

Concerns about deflation – falling prices of goods and services – are rooted in the view that it is very costly. We test the historical link between output growth and deflation in a sample covering 140 years for up to 38 economies. The evidence suggests that this link is weak and derives largely from the Great Depression. But we find a stronger link between output growth and asset price deflations, particularly during postwar property price deflations. We fail to uncover evidence that high debt has so far raised the cost of goods and services price deflations, in so-called debt deflations. The most damaging interaction appears to be between property price deflations and private debt.

Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.

Once we control for persistent asset price deflations and country-specific average changes in growth rates over the sample periods, persistent goods and services (CPI ) deflations do not appear to be linked in a statistically significant way with slower growth even in the interwar period. They are uniformly statistically insignificant except for the first post-peak year during the postwar era – where, however, deflation appears to usher in stronger output growth. By contrast, the link of both property and equity price deflations with output growth is always the expected one, and is consistently statistically significant.

The exception to the general rule was the Great Depression but, that was also an asset bubble deflation coupled with consumer price deflation.

In their attempts to fight routine consumer price deflation, central bankers create very destructive asset bubbles that eventually collapse, setting off what they should fear – asset bubble deflations.

Economists fail to see that asset inflation matters, not just CPI inflation. That’s another point Furman fails to understand. The Fed has blown several assets bubbles of increasing amplitude in a foolish attempt to create more inflation while totally ignoring massive inflation in housing and other financial matters.

Most economists have no idea how to even measure inflation and/or focus only on consumer inflation. The result has been problem after problem.

Inflation Expectations

Furman’s noise about inflation expectations is also a hoot. Fed studies and common sense both show inflation expectation theory to be total nonsense.

Second Fed Study Concluded Inflation Expectations Theory is Nonsense

Also consider A Fed Economist Concludes the Widely Believed Inflations Expectations Theory is Nonsense.

Here are some excerpts from the actual study:

The direct evidence for an expected inflation channel was never very strong. Most empirical tests concerned themselves with the proposition that there was no permanent Phillips curve tradeoff, in the sense that the coefficients on lagged inflation in an inflation equation summed to one.

In addition, most standard tests of the new-Keynesian Phillips curve suffer from such severe potential misspecification issues or such profound weak identification problems as to provide no evidence one way or the other regarding the importance of expectations (much the same statement applies to empirical tests that use survey measures of expected inflation).

What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion.

It is far, far better and much safer to have a firm anchor in nonsense than to put out on the troubled seas of thought. John Kenneth Galbraith (1958).

Few things are harder to put up with than the annoyance of a good example. Mark Twain, The Tragedy of Pudd’nhead Wilson (1894)

One should not need a study to prove the obvious. And it’s obvious that inflation expectation theory is nonsensical.

The reason has to do with the way inflation is calculated.

What Can the Fed Do About the Price of Food, Medicine, Gasoline, or Rent?

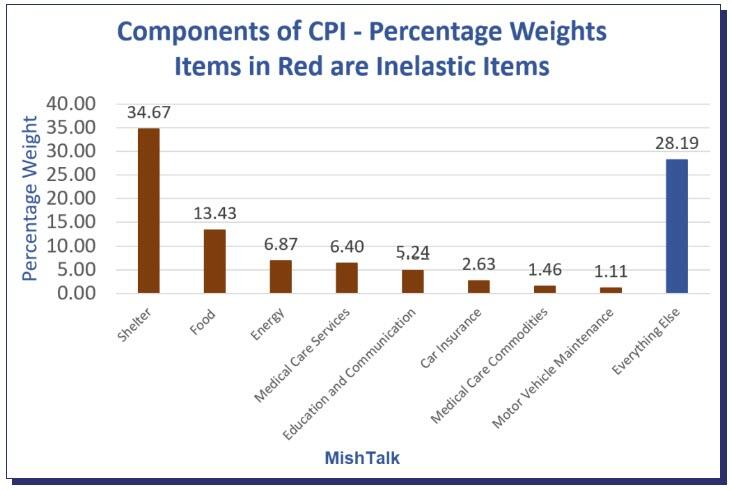

CPI Weights from BLS chart by Mish

Stupidity Well Anchored: Absurdity of Inflation Expectations in Graphic Form

I discussed the silliness of inflations expectations theory in Stupidity Well Anchored: Absurdity of Inflation Expectations in Graphic Form

Inflation Expectations Q&A

Q: If consumers think the price of food will drop, will they stop eating out?

Q: If consumers think the price of food will drop, will they stop eating at home?

Q: If consumers think the price of natural gas will drop, will they stop heating their homes and stop cooking to wait for the event.

Q: If consumers think the price of gas will drop, will they stop driving or not fill up their car if it is running on empty?

Q: If consumers think the price of gas will rise, can they do anything about it other than fill up their tank more frequently?

Q: If consumers think the price of rent will drop, will they hold off renting until that happens?

Q: If consumers think the price of rent will rise, will they rent two apartments to take advantage?

Logically speaking, since the vast majority of the CPI is inelastic, and some of “everything else” is also inelastic, how can expectations matter at all? A Fed study concluded the same thing.

Asset Irony

People will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down.

People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop.

The very things where expectations do matter are the very things the Fed ignores.

Economic Wizards and Their Targets

Furman wants the Fed to stabilize targets below 3 percent then aim for something higher later. What is magic about 2 percent, 3 percent or any other number, given the fact there is no benefit to inflation at all?

The strive for inflation in a disinflationary world created massive asset bubbles and led to global wage arbitrage, outsourcing, and just in time manufacturing.

Now, we have gale force inflationary winds blowing stiffly in our face thanks to deglobalization, decarbonization, and inane energy policies of the Biden administration.

Don’t Worry It’s Only Temporary

The push for 3 percent, 4 percent, whatever percent is of course only temporary just as Nixon’s trashing the gold standard in in 1971 was only temporary.

We still pay the costs of that temporary move. In fact, all of the boom-bust cycles and exponential increase in debt dates to that event.

It would behoove economists to understand that point.

Bottom Line is More Inflation

Not only does Biden demand more clean energy, he also demands consumers pay the maximum amount for it, despite that being counterproductive to the main goal. For discussion, please see The Cost of Soup and Solar Panels is About to Increase, Thank President Biden

And president Biden has latched on to prevailing wages as discussed in Yet Another Biden Regulation Will Increase Costs and Promote More Inflation

No one has bothered to do any analysis of how the push to EVs does not scale or the infrastructure costs to achieve the goal even if the idea did scale.

My readers are far better informed than these alleged economic wizards. For discussion, please see What Do MishTalk Readers Think About “Electric Vehicles for Everyone?”

But, “It is far, far better and much safer to have a firm anchor in nonsense than to put out on the troubled seas of thought.”

That’s what made Furman the perfect choice for President Barack Obama’s chair of the Council of Economic Advisers (CEA). And as you can see, he still has the magic touch.

At some point Fed will concede it has no control over supply. That’s when we will start getting leaks of raising the inflation target

— zerohedge (@zerohedge) June 21, 2022

* * *

Tyler Durden

Mon, 08/21/2023 – 19:00

gold

inflation

deflation

reserve

policy

fed

bubble

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…