Economics

Rising Treasury Yields Can’t Substitute For Fed Rate-Hikes

Rising Treasury Yields Can’t Substitute For Fed Rate-Hikes

Authored by Alexander William Salter via The American Institute for Economic Research,

The…

Rising Treasury Yields Can’t Substitute For Fed Rate-Hikes

Authored by Alexander William Salter via The American Institute for Economic Research,

The US economy grew at a remarkable annualized rate of 4.9 percent this quarter, the Bureau of Economic Analysis reports. This was significantly faster than most analysts expected. Strong growth is good, but there’s some less-welcome news, too: Nominal (current-dollar) GDP grew at an 8.5 percent annualized rate. The implied inflation rate, 3.6 percent, suggests the Federal Reserve still has some work to do to tame inflation.

Remember the most recent CPI release showed core inflation, which excludes volatile food and energy prices, running at 3.87 percent. I argued the FOMC should hold rates steady when it meets at the end of the month. While I still think that’s right, I’m less confident than I used to be.

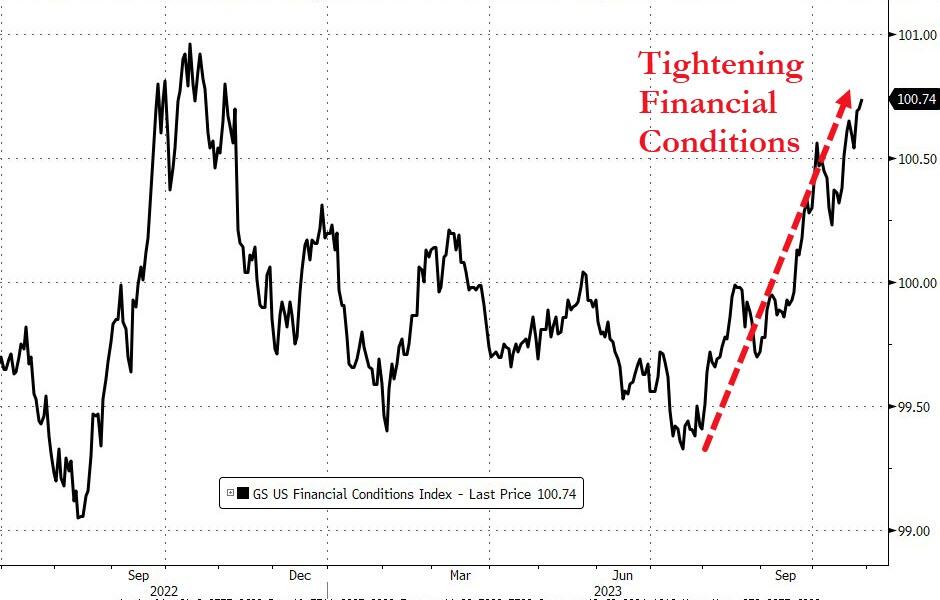

There’s another factor we have to consider: the turbulence in bond markets.

It’s no secret that bond yields have shot up in recent weeks. The current yield on a 10-year Treasury is approximately 4.90 percent.

Many commentators, and some Fed officials, think rising interest rates elsewhere in the economy can substitute for a Fed target-rate increase. But I don’t think this claim withstands scrutiny.

Greg Ip provided a good overview of the argument in his recent column:

Normally, a bigger deficit stimulates growth and causes the Fed to tighten monetary policy. But the latest run-up in yields doesn’t reflect higher expected growth, but a higher term premium — the added return investors demand to hold long-term bonds instead of shorter-term Treasury bills.

That higher term premium is a restraint on borrowing and spending now. As Richard Clarida, a former vice chair, put it, ‘Your past fiscal excesses show up as a headwind today.’ In other words, the bond selloff is giving the Fed an added reason not to raise interest rates, not exactly an incentive for Washington to quit borrowing.

This line of thinking seems plausible.

But it violates one of the most important rules of economic analysis: never reason from a price change.

We need to know why bond prices are falling, and hence yields rising, before we can discuss the implications for Fed policy.

Ip’s column suggests falling Treasury prices are explained by an unusually large supply of new Treasuries, driven by record peacetime deficits. Last fiscal year’s deficit was $2 trillion, or 7.5 percent of GDP. The Treasury Department had to offer large amounts of bonds to cover that fiscal gap.

What does this indicate about the natural rate of interest, which Fed policy is supposed to track? You offer a bond when you want to borrow money. Hence, an increased supply of bonds means an increased demand for loanable funds. All else being equal, when the demand for loanable funds rises, its price—the interest rate—must rise, too. Increased competition for scarce financial resources between the private and public sectors should drive up borrowing costs, and with it the natural rate of interest.

To keep monetary policy sufficiently tight in the face of a higher natural rate of interest, the Fed will need to target a higher nominal interest rate than would have been necessary had the natural rate of interest not risen. Hence, the market data imply nearly the opposite of what many commentators and policymakers recommend. Of course, it’s possible that the natural rate for longer-term borrowing contracts is rising while that of short-term contracts remains the same, i.e., that the term structure of interest rates is changing.

But if the yield curve is the explanation, then market forces aren’t “substituting” for Fed policy.

They’re simply reflecting an economic transition from one microeconomic equilibrium in the market for loanable funds to another.

I’m not sure which story is correct. But I’m confident that the narrative of rising bond yields standing in for Fed rate-target hikes doesn’t hold up. We’ll get a better picture of the path forward as additional data become available. Until then, hedge your bets.

Tyler Durden

Mon, 10/30/2023 – 12:40

dollar

inflation

monetary

markets

reserve

policy

interest rates

fed

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…

{kind=link}

{kind=link}

{kind=link}