Economics

Nikkei 225: Short-term positive momentum emerged ahead of BoJ

Recent decline in the Nikkei 225 has managed to stall again at the key 200-day moving average with positive momentum seen in the hourly RSI indicator….

- Recent decline in the Nikkei 225 has managed to stall again at the key 200-day moving average with positive momentum seen in the hourly RSI indicator.

- Bank of Japan’s (BoJ) latest quarterly outlook report will be closely watched; upbeat inflationary forecasts for FY 2023/2024 may signal a faster pace of monetary policy normalization.

- The TOPIX Banks and Financials sectors have started to price in such a “quickened pace” of policy normalization scenario in the past week.

- Watch the 30,490/30,320 key short-term pivotal support on the Nikkei 225

Since the start of Q3 2023, the Nikkei 225, Japan’s benchmark stock index has wobbled and recorded a 2nd half-year-to-date return of -7.83% as of 30 October 2023 at this time of the writing, in stark contrast to a positive performance of +27.19% seen in the 1st half of 2023.

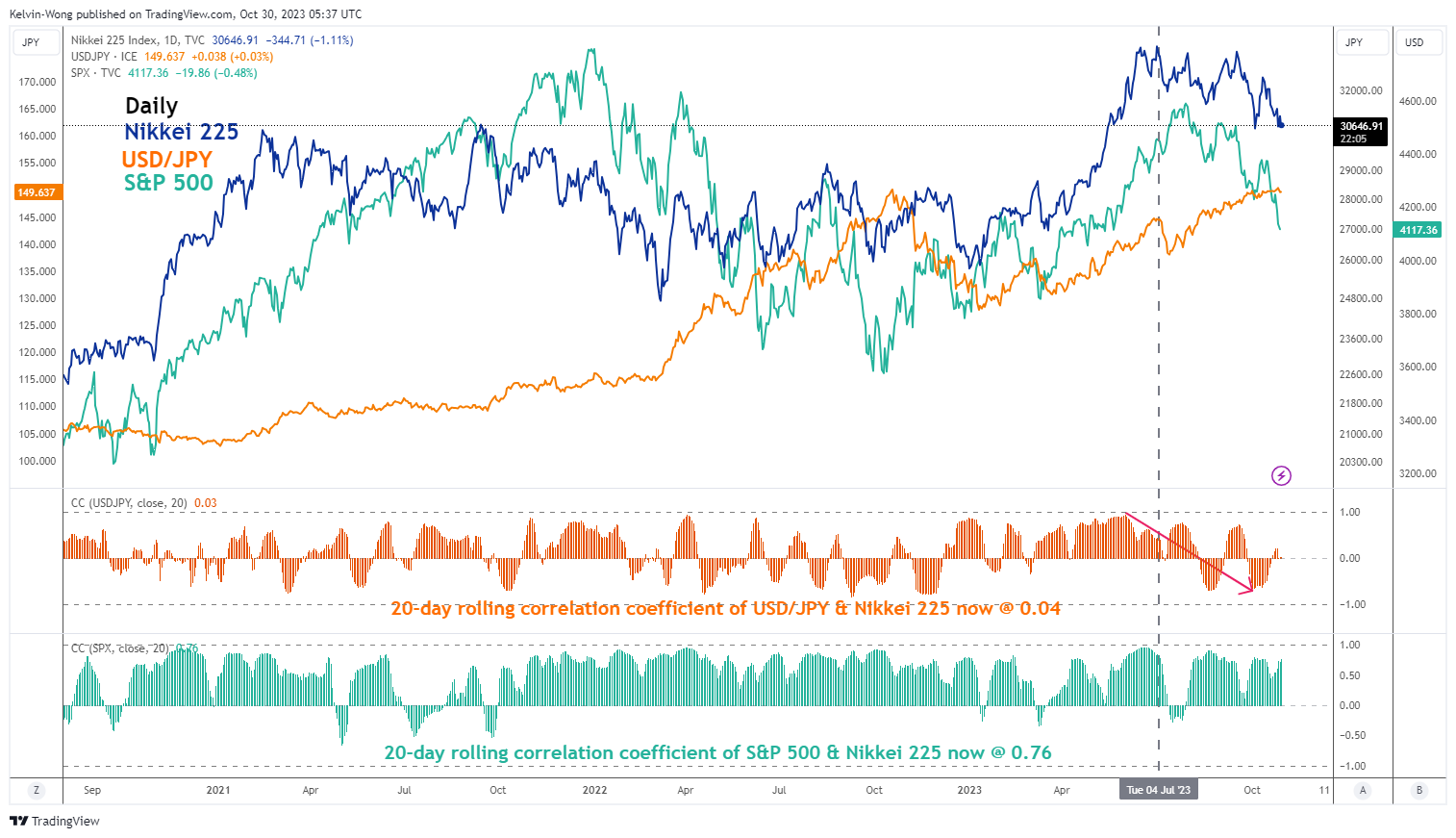

The primary driver that caused the ongoing weakness in the Nikkei 225 has been external rather than internal (see Figure 1). The movement of the Nikkei 225 has moved in direct lockstep with the medium-term bearish trend of the US S&P 500 benchmark index since the start of Q3 with a high 20-day rolling correlation coefficient of +0.76 while almost zero correlation with the USD/JPY (see Figure 1).

Fig 1: Nikkei 225’s 20-day rolling correlation with USD/JPY & S&P 500 as of 30 Oct 2023 (Source: TradingView, click to enlarge chart)

The upcoming Bank of Japan (BoJ) monetary policy meeting outcome together with the release of its latest quarterly outlook on Tuesday, 31 October may shift the dial back to more “localized” factors that are likely to have more influence on the Nikkei 225’s price movements at least in the short to medium-term.

The expectations have risen for BoJ to make changes to its forward guidance with the possibility of increasing the 1% upper limit of the flexible yield curve control programme on the 10-year Japanese government bond (JGB) yield due to the persistent upward movement of the US 10-year Treasury yield in the past month.

Also, all eyes will be on the latest inflation and growth forecast figures in the quarterly outlook report. Given that the latest leading Tokyo area’s CPI data for October that was released last Friday, 27 October has indicated the resurgence of sticky inflationary pressures as growth in the core-core inflation rate (excluding food and energy) came in at 2.7% y/y that surged above August and September’s prints as well as above expectations of 2.3% y/y.

Hence, BoJ may upgrade its forecast for FY 2023 core CPI (excluding fresh food) to around 2.7% to 2.9% versus 2.5% in the July report) as well as FY 2024 core CPI forecast to around 2% to 2.1% from 1.9% in July.

On the growth side, BoJ has upgraded its economic assessment for six of Japan’s nine regional economies in the latest regional economic report released on 19 October. Therefore, it is likely that the FY 2023 real GDP growth outlook may be upgraded as well to 1.8% annualized from 1.3% in the July report while FY 2024/2025’s GDP forecasts are likely to be unchanged at 1.2% and 1% due to the rising risk of a global stagflation environment.

If the upbeat inflationary forecasts turn out as expected, it is likely to give a clearer signal to market participants that BoJ is moving towards monetary policy normalization at a faster pace away from sticky short-term negative interest rates. Such guidance may trigger a short to medium-term positive feedback loop into the Japanese stock market as market participants view that BoJ is formulating imminent policy changes in the pipeline to address the negative effects of the weakening JPY that put upside pressure on imported inflation which in turn will eventually dampen internal demand.

Japanese banks and financials equities have started to price in a more hawkish BoJ

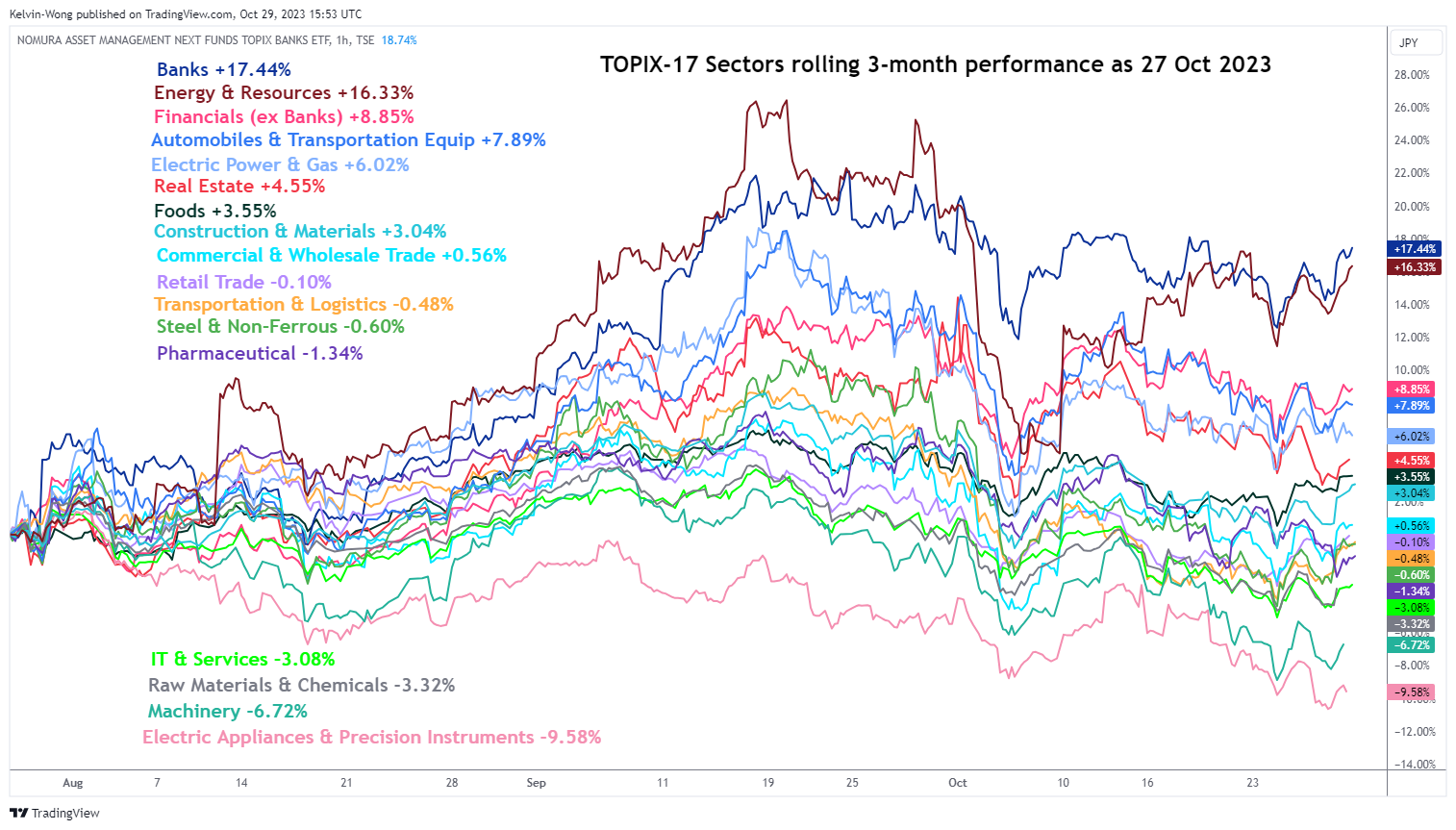

Interestingly, two internal demand-sensitive TOPIX sectors have started to price in such a “faster pace of monetary policy normalization expectations”in the past week. The Banks and Financials sectors have recorded rolling three-month returns of +17.44% and 8.85% respectively as of last Friday, 27 October that outperformed the broader TOPIX stock index over the same period (see Figure 2)

Fig 2: 3-month rolling performances of TOPIX sectors as of 27 Oct 2023 (Source: TradingView, click to enlarge chart)

Watch the key 200-day moving average support on the Nikkei 225

Fig 3: Japan 225 minor short-term trend as of 30 Oct 2023 (Source: TradingView, click to enlarge chart)

The recent decline of -6.75% seen in the Japan 225 Index (a proxy for the Nikkei 225 futures) from its 12 October 2023 minor high of 32,662 has managed to stall at the key 200-day moving average (price actions have traded above it since 24 March 2023) which also confluences with the key short-term pivotal support zone of 30,490/30,320.

In addition, short-term momentum has also turned positive as indicated by the hourly RSI indicator which flashed a prior bullish divergence condition last Thursday, 26 October, and continued to shape a series of higher lows thereafter.

A break above the 31,040 near-term resistance sees a further potential push-up towards the next intermediate resistance zone of 31,430/31,630 (also the 20-day moving average) in the first step.

On the other hand, a failure to hold at the 30,320 key support invalidates the recovery scenario to expose the next intermediate support at 29,900 (a major ascending trendline from the January 2023 low).

inflation

stagflation

monetary

policy

interest rates

correlation

negative interest rates

monetary policy

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…

{kind=link}

{kind=link}

{kind=link}