Economics

Market Continues To Shrug Off Efforts By Fed Policymakers To Push Back On Rate Cut Expectations

Market Continues To Shrug Off Efforts By Fed Policymakers To Push Back On Rate Cut Expectations

By Jane Foley, Senior FX strategist at Rabobank

Donald…

Market Continues To Shrug Off Efforts By Fed Policymakers To Push Back On Rate Cut Expectations

By Jane Foley, Senior FX strategist at Rabobank

Donald Trump may be the front-runner for the Republican candidacy ahead of next year’s US presidential election, but his name cannot appear on the 2024 primary ballot in Colorado due to a ruling by the state’s highest court yesterday. The decision is based on a clause in the 14th Amendment which disqualifies those from public office who swore to defend the US constitution and then “engaged in insurrection or rebellion” against the US – this a reference to Trump’s part in the Capitol attack on January 6, 2020. Trump now has the opportunity to appeal. The high court is also being asked to decide whether Trump could use presidential immunity from prosecution in regard to his actions in the attack.

Meanwhile, in a rally in Iowa yesterday, Trump stepped up his verbal outbursts against immigrants accusing them of “destroying the blood of our country”. He used the rally to point out that he had not read Mein Kampt, and that Hitler has used language “in a much different way”. Trump has promised to push back against illegal immigration if elected back to the White House next year and also to restrict legal immigration. The anti-immigration stance chimes with sentiment in various countries in Europe. Far-right political parties are now reported to be in the top three most popular in almost half the EU.

Yesterday’s remarks by ECB member Villeroy were probably intended to push back on early rate cut expectations. However, since he conceded that rates should probably come lower next year the market took his remarks as having a dovish edge even though he also talked about a plateau for rates and the need for patience. Yields across the German curve shifted lower yesterday even though Villeroy’s comments coincided with those from ECB member Kazaks who indicated that rates needed to stay at current levels for some time to ensure that wage growth slows and that new risks for inflation don’t arise. The release of final November Eurozone CPI inflation data confirmed that the headline rate dropped back to 2.4% y/y from 2.9% the previous month. Although ECB officials clearly remain guarded about inflationary risks, on the back of Germany’s weak IFO survey results earlier this week and Friday’s dismal Eurozone December PMI data, the market is reluctant to embrace the central bank’s hawkishness. On a one month view the EUR is the second weakest performing G10 currency after the USD.

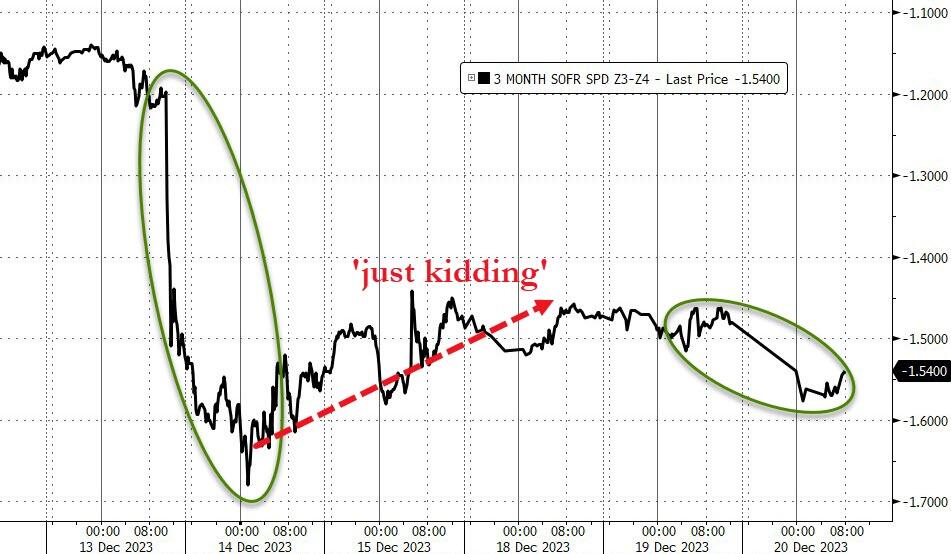

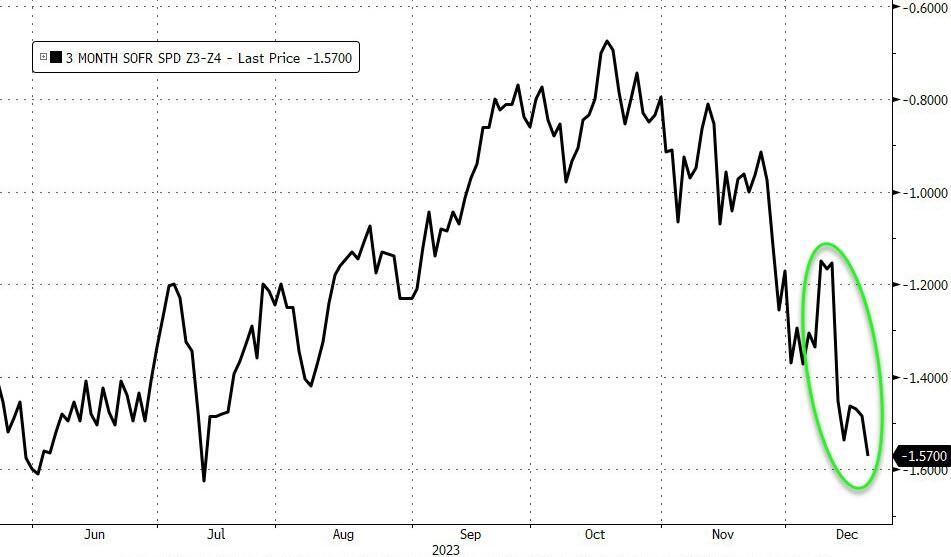

The market is also continuing to shrug off efforts by Fed policymakers to push back on market rate cut expectations. Yesterday, Atlanta Fed president Bostic said that there was no urgency to lower rates. Despite the warnings from Fed officials on policy, US stocks continued to push higher yesterday on rate cut hopes.

Since their meeting last week, Fed officials have been flummoxed that investors expect even faster and deeper cuts. The result: Confusion over when and how quickly the Fed might cut.

“The Fed shouldn’t have been surprised by the market running with it.” https://t.co/Tth5I2NzXe

— Nick Timiraos (@NickTimiraos) December 20, 2023

[ZH: Rate-cut expectations briefly declined after the initial Powell pivot plunge, but are now heading back to cycle lows, pricing in over 6 rate-cuts for next year]

Overnight, Asian stocks also pushed higher, except for China’s CSI 300. As expected, no change in benchmark lending rates was forthcoming from the PBoC overnight, though speculation is rife that further easing will be announced in the New Year.

Yesterday morning it was the JPY that was falling hardest, though it has since pulled back from its lows. The sharpness of yesterday’s move illustrates that the market was expecting more hawkish rhetoric from the BoJ’s December policy meeting. Like other central banks BoJ Governor Ueda hinted that policymakers want to see more data before being convinced that a policy move is warranted. This left the market essentially without any firm forward guidance, though surveys indicate that April is currently the favoured months for a BoJ rate hike amongst BoJ watchers. This would allow the central bank to digest the outcome of the 2024 spring wage talks.

By contrast, in Canada data is suggesting that inflation is not moving down fast enough. The November headline CPI inflation rate remained at 3.1% y/y, counter to market expectations for a fall to 2.9%. A significant contributing factor was housing, with rents rising 7.4% y/y last month. This follows separate data from Statistics Canada indicating that the population grew 1.1% in Q3, the highest rate in any quarter since 1957. Immigration may help with labor market shortages, but it also creates unintended consequences. Housing crises are now fairly commonplace in many cities across the developed world. These can be linked with voter dissatisfaction and in some cases the rise in the support for the far-right.

US data brought some comfort on this front. Housing starts grew by a stunning 14.8% m/m and looks set to expand by 25% in Q4, though this followed a 20% contraction in Q3. The bounce back suggests that confidence is returning to the sector, probably encouraged by the decline in mortgage rates.

Oil is holding is recent gains on concerns over the safety of shipping in the Red Sea. So far, the impact on oil supply appears to have been limited, though the market will continue to monitor the situation.

German and French finance ministers were due to meet in Paris yesterday in an attempt to reach a agreement on the reform of the EU fiscal rules. The two countries have differing views on how investment levels can be sustained if budget deficits move above target. As yet, there is no news on a deal, meaning that the market will continue to keep watch today.

Tyler Durden

Wed, 12/20/2023 – 12:10

inflation

policy

fed

central bank

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…