Economics

Goldman: “No One Is Positioned For A Rally And Everyone Wants It To Roll Over, Rather Than Be Forced To Chase”

Goldman: "No One Is Positioned For A Rally And Everyone Wants It To Roll Over, Rather Than Be Forced To Chase"

By Bobby Molavi, Goldman managing…

Goldman: “No One Is Positioned For A Rally And Everyone Wants It To Roll Over, Rather Than Be Forced To Chase”

By Bobby Molavi, Goldman managing director and macro trader

Equity markets seem to have been aided by a few things: a growing belief that inflation has peaked and the ability of the fed to deliver a soft landing, a more positive tilt around the consumers ability to digest higher rates and higher cost of living, China re-opening and lower geo political tail risks; and the benefit of a mild winter offsetting the structural gas shortage issues faced by Europe.

Whilst there is definitely pain to bear as we move from the excess liquidity and ‘free’ capital environment post Covid the durability of the global economy in managing this shift has translated to the a much more constructive market reflexivity to a grind higher on terminal rates.

What is interesting is that the investor narrative has generally remained bearish through this rally….yet positioning has quietly re-grossed and is materially less conservative than it was.

With the benefit of hindsight, we expected many bad things in Q4: European power crisis, rising unemployment, slowing gdp, risk of recession, no China reopening, Corp. margin decline, credit defaults and bankruptcies rising as well as continued geopolitical tensions. None materialized and carry trades performed extremely well In Jan as most market participants sat on their hands. But now there seems to be a growing asymmetry in relation to the next move from here, and it seems to be much more skewed negative today than it was on Jan 1st. More on that later.

What have we seen beneath the surface. A pain squeeze across global markets as well as a marked shift in leadership. On one hand the ‘generals’ have fallen from grace (FAANG) and on the other the revenge of the old economy has taken hold (absolute and relative Market cap growth across Banks/Industrials/Mining). At the end of day, whether driven by shorts or by under positioning we have seen this ‘squeeze’ dynamic everywhere. GS Prime Brokerage reported the largest short covering in eight years while simultaneously we saw outperformance and near record start of year rallies in Europe and China.

But by the end of last week, things showed some signs of stalling. It felt like the tone of the market pivoted to renewed concerns around rates, growth and recession. Last week saw the biggest selling by hedge funds in seven weeks, we began to see tactical shorts being reset as well as larger index hedges being laid out and we saw a marked and sizeable turn in relation to non profitable tech, retail favorites and higher beta segments of the market.

The early start of year rally has cause angst for many reasons: firstly, no one was positioned for it, secondly no one believes in it, and now everyone wants it to roll over rather than be forced to chase.

For me, what one client said rang true: “eyes need to remain on China.” While BOC continues to stimulate and market continues to run hot and reopen…there is enough read across to sustain global markets. Less so for US, which now trades on 18.5x but for ‘cheaper’ regions like Europe….where exposure to China has hit 20 year highs…and positioning remains relatively low…there is now a growing underbid emerging.

For now, the broader market seems intent on clinging onto a more dovish ‘goldilocks’ softer landing narrative irrespective of yield behavior or Fed commentary. We saw hot CPI/PPI prints waved away on ‘January effect’ and the multitude of hawkish fedspeak last week similarly ignored:

- Barkin – “I think there is a very good case for leaving rates higher for a longer period”,

- Logan – “We must remain prepared to continue rate increases for a longer period than previously anticipated”

- Mester – “Compelling Case for Half-Point Hike.”

Time will tell how long that will last.

Range of outcomes.

It feels like we spent most of last year debating inflation and rates and what the new normal would be for yields. It feels like that corridor has narrowed with greater certainty as inflation shows increasing signs of having somewhat topped out. That corresponded with a very dovish tone to 2023 so far, and a material uptick in optimism and soft landing hopes across the markets.

Now the debate has moved on from how high…to how high for how long. No longer is it about the where rates cap out…we’re roughly there in most peoples mind…but are we going to cap out and then move back to trend (still find it hard to see cuts in early 2024 personally) or do we need to prepare for higher for longer. I think the end of last week was informative…as strong inflationary prints and hawkish commentary led to a rise in conversation around being at 5 to 5.5% not for 3 months but more likely for 3 years. At first glance, this becomes a real concern but equally the longer the market can shrug this off, the more constructive that is going to be.

Ignored tail risks.

This is a real head scratcher for me. Throughout Covid, the rebound from Covid and through 2022 and Russia/Ukraine crisis and China/US concerns the markets were extremely reflexive to any headline that prodded a tail risk bruise. 2023 dynamics are notably different. Putin aggressive commentary… market shrugs. US debt ceiling and risks of a 2011 repeat (spx sold off 17%)…market shrugs. Chinese (reputedly) balloons all over American and Canadian skies….market shrugs. Risks around European energy shortage later in the year….that is Q4’s problem. The long and short of it is that we feel like we’re in a very complacent place as evidenced by dramatic resetting of vol lower in Q1 thus far. Things are usually fine until they are not…and I thought it interesting to see rising demand for tail protection at the end of last week.

Non fundamental flows.

For me 2023 has been characterized by stalemate. The bulls didn’t get a chance to buy the market and the bears are waiting for the market to correct. Only the hedge fund community and retail community have been active vs historical levels. One participant that has not stood still has been the ‘non fundamental’ community. How to break this down into component parts?

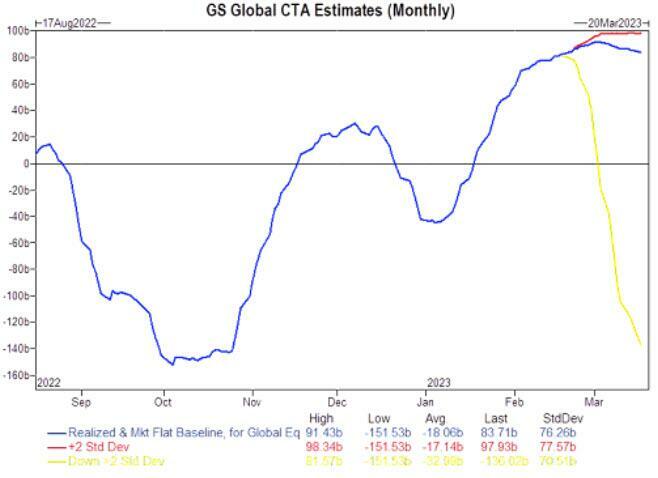

I see 2 main buckets…..Buybacks, Systematic/CTA. The buyback component has been a growing backstop and tailwind for equity markets in recent times. Authorizations have risen materially and even spread to Europe (~2% equity withdrawal annually) on the back of excess cash creation and a focus on TSR over growth and M&A. But you have to wonder with a risk free 5% for holding T-bills…when will corporates start to think money markets offer greater value than buying back their own stock? The CTA community was arguably the biggest buyer of markets in Jan 2023…as vol reset lower across all asset classes and data came through better than expected the need to unwind shorts triggered a material re-risk. That impulse is slowing and, in fact, is now, a headwind or likely supply source whatever the direction from here. Worryingly on a down tape….we can see over $217bn of supply coming over the month in certain scenarios…not sure who is there to offset that supply. $2 trillion of options rolled off last week and it will be interesting to see how the market digests the removal of that long gamma support.

Micro.

Have we past the point of where corporates can pass on rising costs to consumers? On the back of CPI and PPI there was renewed focus on corporate forward earnings and margins in light of persistent higher ( and in some cases, rising, costs). Who can absorb these pain points and who is now going to have suffer in terms of volumes, growth or margins as the end consumer begins to push back? Our Strategists’ note this morning points out that a 5% increase in wages could lower the earnings of the STOXX 600 by more than 10%. Combining labour exposure and margin sensitivity, they find that the most exposed sectors are Construction & Materials, Industrials, Travel & Leisure, Autos & Parts and Food Retailers

The case for Europe.

I know…I know….the Englishman once again trying to desperately find light in the traditionally dark tunnel of Europe. Yes we have had yet another company decide to ‘evaluate’ whether they want to be listed in UK anymore rather than shift to greener pastures of US (Flutter). That being said, there is as compelling a case for as I’ve seen in quite some time. On a relative basis ownership of UK and Europe remains very very light. As sponsorship for the market changes, UK/Europe are quietly backing back into having a lot of the companies that the market is re-rating back towards the upper tranches of the market cap waterfall (BNP vs Adyen or Glencore vs Iberdrola).

On a valuation basis, US remains stickily expensive vs history and UK/Europe remains resolutely cheap. On a global asset allocation basis…yes Europe has seen inflows…but for what is a (relative to US) shallow liquidity market…if the heavy pools of capital continue to add exposure here then the impact should be disproportionate. Finally, as a hunting ground for accretion, geographical diversity or growth…I sense that M&A will come (see Vodafone stake building and the various rumours around other UK assets in last few weeks).

End of day, the European market is up 13% ytd, vs, US at 8%….with rising interest and changing fundamentals, value outperforms growth, so Europe starts to benefit. When you add to mix that US still trading at high multiples in spite of forecasting little to no growth for 2023 while Europe trades below longer term average valuations, has greater exposure to lower rated sectors (value-oriented ones) and Cash flow yields for places like UK at highest level globally at 7.8%. In fact….. Every sector in Europe trades at discount to its peer sector in the US. As Oppy’s team points out, “European consumer staples: have de-rated in recent years, though boast similar earnings growth; Utilities: also at a big gap – US utilities more regulated, but right now European utils have better growth prospects (investment in renewables); Tech: valuations for Europe and US tech are very similar, but growth in European tech better, and more exposed to Asia – Europe tech derives 50% sales from Asia, best play at China reopening; Energy: at huge discount, cash flow yields in European energy stocks very high.” After dealing with one issue or another forever (bank recaps, oil recaps, sov credit crises, lack of tech growth), the relative value for Europe has arguably never been greater.

Tyler Durden

Tue, 02/21/2023 – 18:31

inflation

markets

mining

fed

inflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…