Economics

Full CPI And Market Reaction Preview: Everyone Expects A Hotter Print

Full CPI And Market Reaction Preview: Everyone Expects A Hotter Print

While some will be secretly asking chat GPT to write a poem for their…

Full CPI And Market Reaction Preview: Everyone Expects A Hotter Print

While some will be secretly asking chat GPT to write a poem for their loved ones tomorrow (“Violets are blue, roses are red, humans are stupid and will soon all be dead”), those following markets will only care about one thing: the January CPI report (especially after the BLS just revised its seasonal adjustments and weight factors). Here’s what to expect tomorrow, and how the market may react.

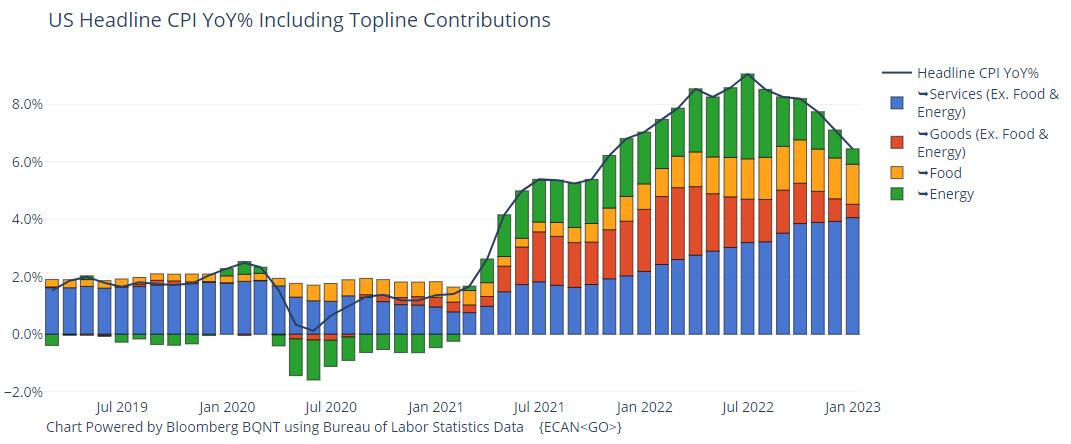

We start off with the big picture, courtesy of Newsquawk which writes that headline consumer prices are expected to rise 0.5% M/M in January (prev. +0.1%, a number which was -0.1% until last Friday’s change in seasonal adjustment and weighting components, see here and here), with the annual rate paring to 6.2% Y/Y from 6.5% in December due to base effects.

The CPI will be underpinned by a small rise in energy prices and persistent strength in food inflation, Credit Suisse says, though the sharp fall in used vehicle prices seen in recent months is unlikely to persist. For the core measure, inflation is likely to have risen by 0.4% M/M, matching the pace seen in December; though the annual rate is seen slowing to 5.5% Y/Y in January from 5.7% previously.

What is perhaps most remarkable, is that at a time when many in the market had decided the time has come to shift attention away from inflation and to jobs, we are again obsessing with CPI, or as DB’s Jim Reid wrote this morning, “it only feels like yesterday that US inflation prints were seen as last year’s news given the recent falls. In addition, forecasts and breakevens suggested we were on a glide path to normality over the next few months and quarters.” However, as Reid observed, that view has received a bit of a jolt in the last 10 days for the following four reasons:

- First we had payrolls print which raised the prospect that core services ex-shelter could stay stronger for longer.

- Then we had lots of hawkish central bank speak that the market had previously ignored but was now slowly waking up to.

- Then Manheim suggested US used cars (+2.5% mom in January) climbed at their fastest rate for 14-months, and…

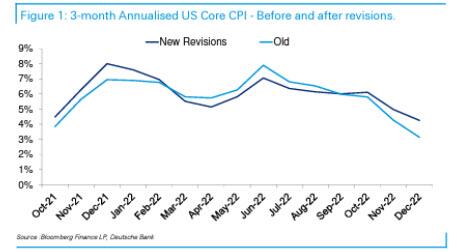

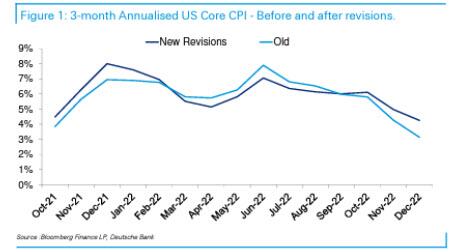

- Finally, we had US CPI revisions on Friday that have rewritten the last year of history and in turn reduced core inflation by around a tenth each month leading up to June and have increased it by an average of around a tenth in each month since August. As such the trend in core CPI hasn’t fallen as much as expected and we now haven’t seen any month less than +0.3% MoM. In addition 3m annualised core CPI ran at 4.3% in December rather than the 3.1% reported at the January 12th release. So although year on year hasn’t changed the momentum is notably different.

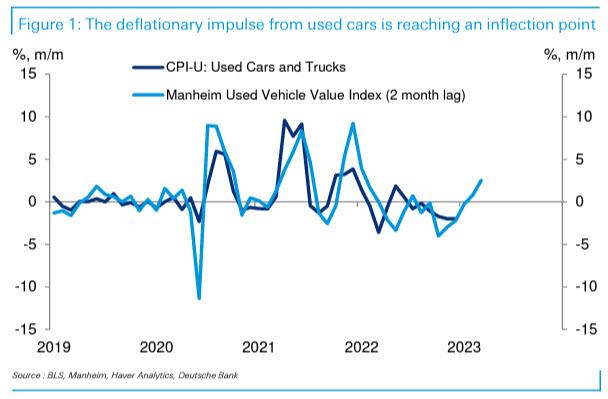

At the component level, DB’s Justin Weidner writes that one main focus will be on used cars and other durable goods as this has been where recent disinflationary pressure has been focused. Indeed, the three-month annualized inflation rate for core goods registered -2% in December. As such, if goods prices were to fall at slower rates going forward or even rise slightly, this would add some to overall inflation. However, recent comments by Chair Powell and Vice Chair Brainard suggest that Fed officials already expect a short-term boost to core inflation from core goods.

Case in point is used cars, for which prices fell 7.6% over the second half of 2022. After three months of large monthly price drops from August to October, wholesale used car prices only posted a minor decline (-0.3%) in November and have since risen by 0.8% in December and 2.5% in January. Given the typical two-to-three month lag from wholesale prices to retail prices, used car prices will still have declined some in January, but there is some upside risk that the wholesale price gains are reflected earlier.

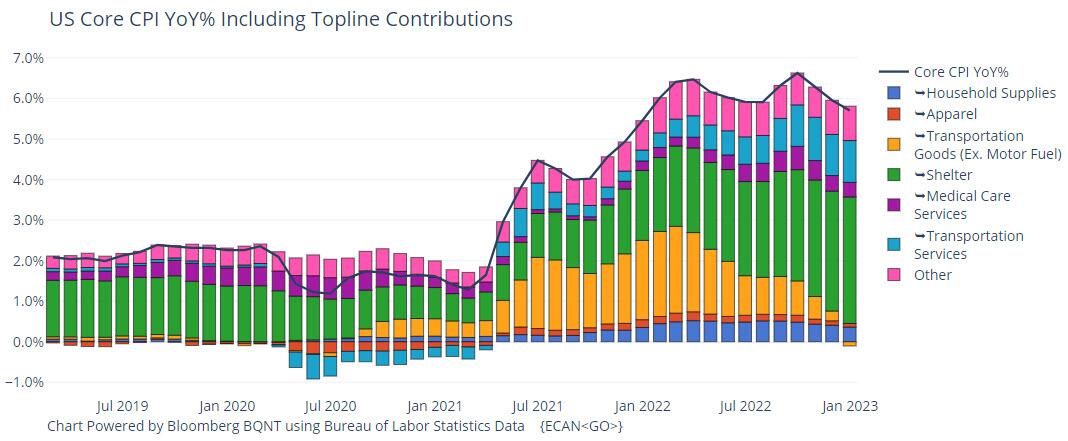

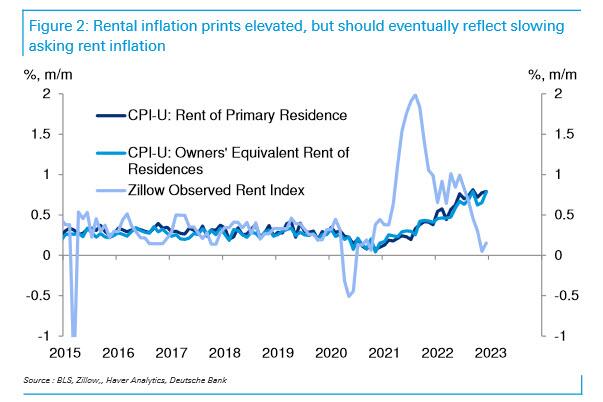

As to services, rents comprise the largest share. The December prints for primary and owners’ equivalent rent remained near their recent highs and notably reaccelerated relative to November, though they are still just off of their recent September peak. Given the CPI methodology for these indices, it will take another couple of quarters before the recent softening in private estimates of asking rents fully percolates through into the CPI. However, the Fed (finally) understands this lag structure and would only be concerned if the monthly run rate in these categories accelerates much further from current levels.

Regarding other major categories, medical care services are again very likely to weigh on the CPI, with health insurance posting something similar in magnitude to the roughly 4% plunges seen in each of the last three months. Similarly-sized monthly declines in health insurance should persist through September and continue to subtract roughly 4bp per month on the headline and core CPI prints. However, it is important to note that this will not impact core PCE, the Fed’s preferred inflation measure. This is one reason why the wedge between core CPI and PCE, which ran at about 10bps on the monthly print in 2022, to invert in 2023. Indeed, diverging trajectories for health care inflation between the CPI and PCE measures argue for greater focus on core services ex shelter and health care in the former.

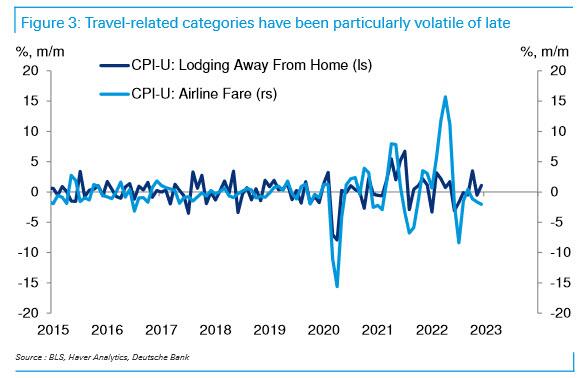

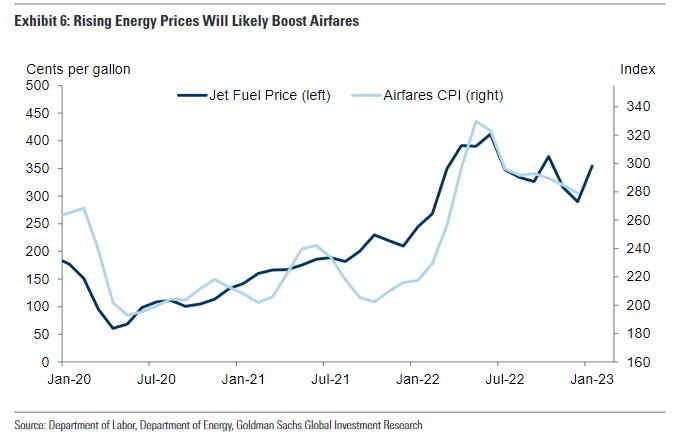

Finally, swing factors like the travel-related industries have been particularly volatile of late, with the monthly changes in lodging away fluctuating between -3.g3% and +3.5% and airfares between -8.4% and +15.7% in 2022. The former rose 4.1% over the final three months of 2022 while the latter fell 4.8%. As such, there is some scope for payback in both of these categories, which given the relative weights (1.1% in lodging away and 0.6% in airfares), would likely offset one another.

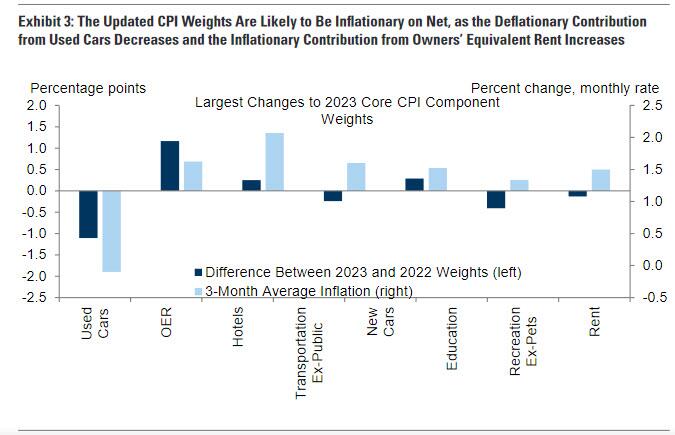

Here, DB’s take a detour into the recently revised seasonal adjustment factors and CPI basket component weights; it notes that the BLS has updated the expenditure weights to be based off of 2021 spending patterns and will be moving to an annual updating schedule going forward (compared to the previous schedule of updating every other year). In general, the largest impact was the increase to the weight of owner’s equivalent rent (OER) from 24.3% of the expenditure basket to 25.4%. Given that OER grew by 0.8% in December and is likely to post similar rates over the next couple months, this should put some upward pressure on headline and core in the near term. However, once CPI rents begin to roll over later in the year, this tailwind should fade and begin to put downward pressure on inflation.

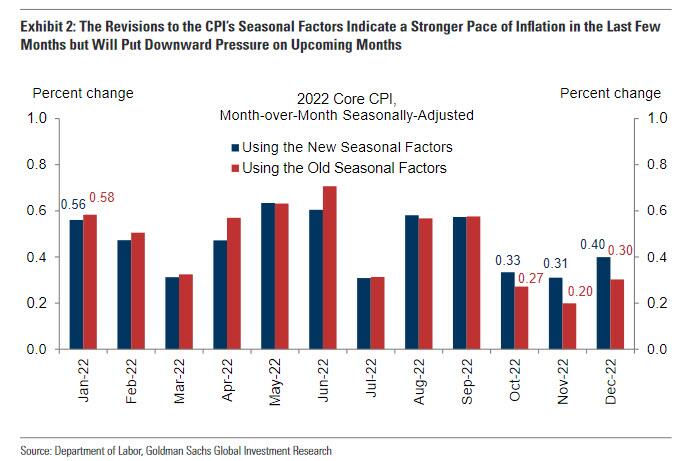

Additionally, while normally revisions to the seasonal factors are not particularly meaningful, this year’s update did meaningfully change the recent trajectory for inflation, namely a meaningful upward revision to the recent three- and six-month annualized core CPI prints. Importantly, none of the recent core CPI prints touched 0.2% m/m. Goods categories, particularly vehicles, were the epicenter of the revisions, with much of their recent disinflationary pressure being revised away.

For the Fed, the revised data (dark blue line above) means that there is less evidence that inflation is on a clear downtrend in the near term, which should add to their conviction on having to deliver at least a 5.1% terminal rate. With the market already fully pricing that for the middle of the year, this sets up the January CPI report as being an important one for determining whether and how much terminal may need to rise. For example, a stronger core CPI print would look less like a one-off and more part of a trend, which could lead to a more pronounced impact on the market’s view of terminal.

* * *

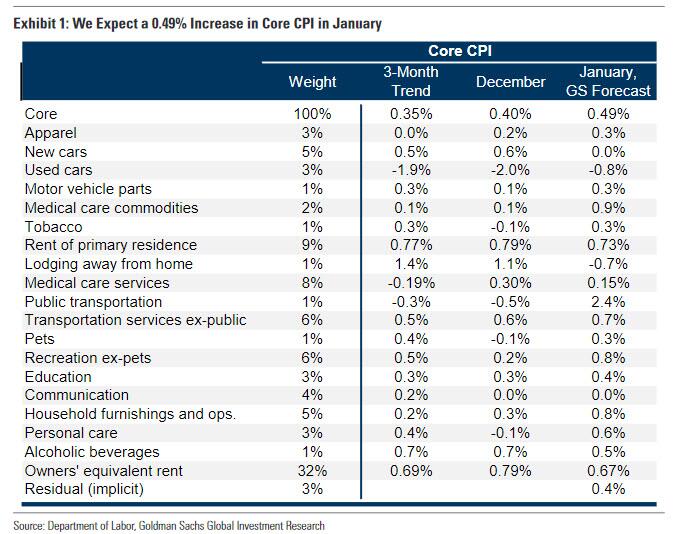

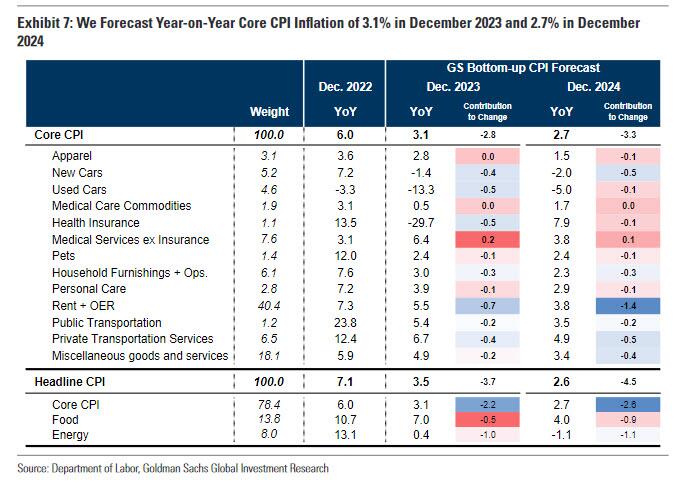

While Deutsche Bank is generally in line with consensus expectations, Goldman’s economists are hotter. In their preview, economists from Jan Hatzius’ team write that they expect a 0.49% increase in January core CPI (higher than the 0.4% consensus) which would reduce the year-over-year rate to 5.63% (also higher than 5.5% consensus). Goldman is also higher in its expectations of a 0.55% increase in January headline CPI (vs. 0.5% consensus), which would reduce the year-over-year rate to 6.39% (some 0.2% above the 6.2% consensus). Exhibit 1 provides a component-level summary of the bank’s forecast.

Like all other banks, Goldman also directs attention to the two annual methodological changes to the CPI. First, the CPI will feature updated seasonal factors, which the BLS revised last week. The revisions were somewhat larger than usual and resulted in a 9bp upward revision to the monthly pace of core CPI inflation over the last 3 months. Nevertheless, the revisions lowered month-over-month core CPI inflation by 2bp in January and by 5bp on average in February through April 2022, which will partly offset upward pressure from the stronger near-term pace on core CPI in 2023Q1.

Second, this month’s CPI will be calculated using updated weights that incorporate data from the 2021 Consumer Expenditure survey and reflect only one year of consumer spending data, rather than two years under the old methodology. Here Goldman agrees with Deutsche Bank and JPMorgan that the new weights will likely be somewhat inflationary, as the weight on owners’ equivalent rent—which remains inflationary—will increase by 1.2pp, while the weight on used cars—which is now deflationary—will decrease by 1.1pp

With that in mind, Goldman highlights three key component-level trends for the January report:

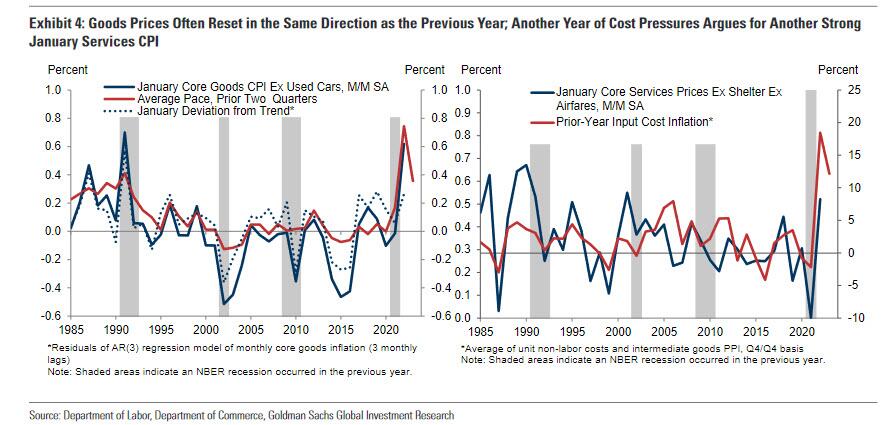

1. Start-of-year price increases, aka the “January effect.” GS expects an 8bp boost to core CPI from start-of-year price increases that have been termed the “January effect.” In today’s higher-inflation environment, firms are likely to implement larger price increases when they reset their prices than they normally would when inflation was low and stable, leading the seasonal factors to underestimate inflation at the start of the year when price resetting is more common.

Goldman expects start-of-year price effects to be most pronounced in prescription drugs, medical services, car fees, and alcohol prices.

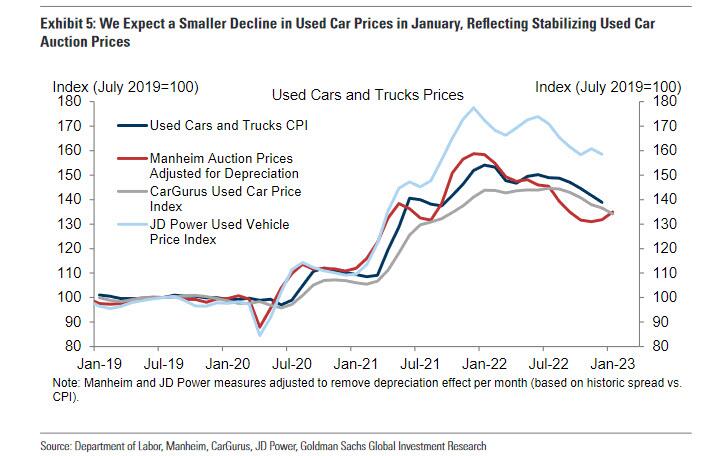

2. Used cars. Goldman expects a smaller decline in used car prices this month (-0.75%, vs. -2.0% in December). Used-car auction prices stabilized on net in January, and “positive residual seasonality” will further boost this month’s print. Combined with the new CPI weights, the bank’s forecast implies a smaller drag from used cars on this month’s core CPI (3bp, vs. 8bp in December).

3. Airfares. Higher fuel prices have put upward pressure on airfares in January and Goldman economists have observed an increase in the bank’s airline team’s real-time measure of airfares. As such, they expect a 3% increase in airfares in the January report, which would boost core CPI by 2bp, following an 2% decline in December.

Elsewhere, Goldman is also forecasting a sequentially-slower pace of shelter inflation (rent +0.73%, OER +0.67%) as weakness in rent growth for new-tenant leases offsets continued upward pressure on existing-tenant leases; the bank also expects apparel prices to increase 0.3%, reflecting a boost from residual seasonality in January.

Going forward, Goldman expects monthly core CPI inflation to come down to around 0.3% as the start-of-year effect fades, and to continue declining to around 0.2% in the second quarter of 2023. It forecasts year-over-year core CPI inflation of 3.1% in December 2023 and 2.7% in December 2024. The deceleration in 2023 is driven more by goods than by services categories.

Turning our attention to another bank (which may not be around for a long time), Credit Suisse says goods prices continue to face headwinds, but the pace of decline is likely to moderate; services inflation will continue to be supported by shelter, which the bank sees remaining elevated for at least a few months before decelerating in H2. CS forecasts are in line with the market consensus, and says that if this is realized, it would be consistent with inflation eventually returning to 2%, “but any reacceleration in the monthly run rate for core CPI would be an unwelcome development for the FOMC,” adding that “combined with January’s strong employment report, this would likely keep Fed rhetoric hawkish, emphasizing the need for ongoing rate hikes and a low probability of a pivot toward easing this year.”

Finally, a quick look at JPMorgan’s forecast, the bank’s chief economist Mike Feroli similarly expects inflation to come in hot relative to estimates, and sees headline CPI easing from 6.5% YoY in December to 6.4% (6.2% survey) in Jan and core CPI to move from 5.7% in December to 5.6% (in line with the 5.6% consensus). Some notable assumptions include: (i) used vehicle prices growing 0.5% in January after three 2% per month declines. (ii) strong but moderate gain of 0.68% in rent.

Market reaction

First, a look at how the market has reacted to CPI prints in the past 2 years. Not surprisingly, with inflation coming in hotter than expected for much of the period, the market reaction hasn’t been exactly favorable.

So with some of the key banks all expecting CPI to come in hotter than the median expectations, it’s pretty much a done deal that stocks will tumble tomorrow right? Maybe not.

Maybe not: as Goldman FICC trader John Flood writes, positioning has indeed turned more defensive into this print: last week the GS Prime book saw the largest net selling in 7 weeks, driven by Macro Products (index ETFs, futures, and baskets), which saw the largest short sales in nearly 5 months. In terms of S&P’s reaction function to headline YoY print, Flood thinks risk is skewed to the upside “as pain trade remains higher and this mkt continues to seek max pain whenever it gets a chance (yes some of this was pre traded today).” Translation: yes, we may get a jerk lower after the hotter than expected CPI, but unless this is powerful enough to monetize puts, which have seen their price surge in recent weeks, at a profit…

… we will likely reverse and squeeze higher on the back of a plain vanilla short squeeze, coupled with a delta (and possibly gamma) squeeze.

And speaking of a bull pre-trade, JPM chief TMT flow trader Ron Adler writes that “whether it’s strategists echoing their concerns ahead of the CPI or more talk of “no landing,” it seemed like everyone was giving their best bearish impression this morning and over the weekend, yet the market soldiers on. It’s tranquil ahead of tomorrow’s data (SPX volumes -26%) while our HT volumes are down MSD% yet skewed 1.3:1 better to buy. There’s a bit of a bias towards growth this am while high short-interest

stocks continue to behave as expected.”

JPMorgan’s market intel team is even more bullish (don’t tell JPM chief sellside analyst and recently converted permabear, Marko Kolanovic). This is what market intelligence head Andrew Tyler wrote this morning:

Our view is that the print will come in-line with the Bloomberg survey. Given that positioning is much more neutral than in 2022, a surprise in either direction should not produce as dramatic a move as we have seen in several of the 2022 prints. That said, TMT/Consumer Discretionary positioning remains low so a dovish CPI print that pulls yields/USD lower could trigger more money flows into those sectors where the MegaCap names; though that would likely take several days. As we consider the next few weeks, an inflationary spike appears to be the biggest downside risk of the “known knowns”. While the China inflationary impulse has yet to materialize, Russia cutting supply has surprised the market with a 500k cut pushing WTI up +2.1% at the time of this writing. Could further cuts be forthcoming?… I do not think WTI needs to go to $150 to reset market expectations more bearishly; if WTI breaches $90, then think you will see Fed expectations and inflation worries become the dominant narrative. What’s the trade? We like being long Tech (QQQ and SMH), China (KWEB and FXI), and Energy (USO and OIH); we think a market neutral approach makes sense, for now.

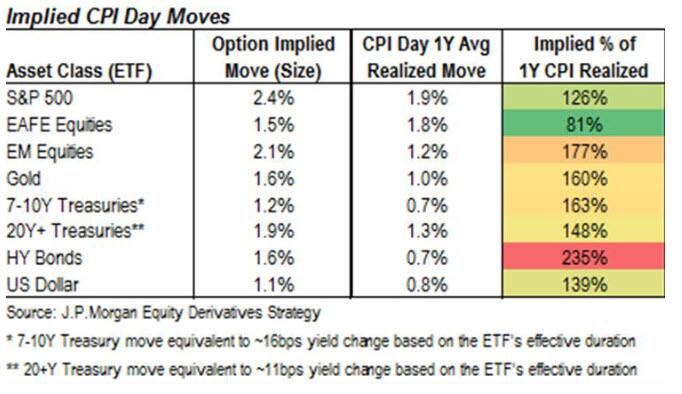

Here JPM’s chief US derivatives strategist Bram Kaplan also chimes in and writes that SPX options are pricing in a 2.4% implied move for the CPI release which is in-line with the market’s average realized move on CPI releases over the past year, but is below what we observed in Jan and Dec. The table below lays out several other implied day moves by asset class:

Finally, in terms of market reaction scenarios, this is what JPMorgan laid out earlier today in terms of CPI buckets and market reactions. Bottom line: 70% odds the CPI report will push the S&P at least 1.5% higher.

- PRINTS ABOVE 6.5%. This bearish outcome would align with the resurgent inflation hypothesis and could be driven by services where the consumer has shown a rebound in spending, evidenced by the latest Manheim print. More troubling for bulls is that this scenario would occur before we have witnessed an inflationary impulse from China. Any print above 6.7% represents a tail event. To monetize this view, would look to sell Expensive Software [JP1XSFT], Crypto [JP11CRYP], and SPACs [JP1BSPAC], and High Short Interest baskets [JPTASHTE]. You may also consider buying TLT and going long USD. SPX down 2.5%; Probability 5%

- PRINTS BETWEEN 6.4% – 6.5%. The hawkish outcome here would not be as negative as if this occurred last year and may be proxied by the Sep 2022 print where we saw CPI stepdown from 9.1% in July to 8.5% in Aug to 8.3% in Sept. That print triggered a -4.3% reaction in the SPX. Positioning is unlikely to lead to as dramatic a result. The recent backup in bond yields may be enough such that we do not see another rate hike priced in given that we would have the March print before the next Fed meeting. . You may consider selling the JPM Cyclicals vs. Defensives Index [JPPQCYDE]. SPX down 75bps – 1.5% with the lower end of the range being more likely if the SPX holds 4k into the print; Probability 25%.

- PRINTS BETWEEN 6.0% and 6.3%. This bullish outcome would likely pull yields lower, along with the USD, and boost risk assets. It may have investors question the pace of disinflation given the previous two prints had 60bps declines from the prior month. The market move would be led by Tech in this scenario with additional outperformance by Cyclicals. To monetize, consider NYFANG Index futures as well as Semis [JP1BSEM] which have outperformed the NDX by ~9% YTD; SPX +1.5% – +2% and then see the rally faded; Probability 65%.

- PRINTS BELOW 6.0%. A print of this magnitude likely re-prices expectations for the Fed to complete two more rate hikes to just one more rate hike. Equities would be boosted by a fall in both the USD and bond yields; Think you would see a low quality/everything rally as we see more short covering. Anything below 5.7% represents a tail event. SPX +2.5% – +3%; Probability 5%.

And here is Goldman’s CPI scenario forecast, which while more to the point than JPM, is generally in agreement on the breakevens:

- <6% S&P up at least 3%

- 6.0 – 6.2% S&P up 1 – 2%

- 6.3% – 6.5% S&P down 1 – 2%

- >6.5% S&P down at least 2%

Much more in the CPI Preview folder in the usual place for professional subs.

Tyler Durden

Tue, 02/14/2023 – 07:44

inflation

derivatives

markets

fed

central bank

inflationary

deflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…