Economics

Frustrated Trader Asks “Why Am I Looking At Numbers At All?”

Frustrated Trader Asks "Why Am I Looking At Numbers At All?"

By Stefan Koopman, Senior Macro Strategist at Rabobank

Jolly JOLTs

The first…

Frustrated Trader Asks “Why Am I Looking At Numbers At All?”

By Stefan Koopman, Senior Macro Strategist at Rabobank

Jolly JOLTs

The first headline that caught my eye when I started writing today’s Global Daily was a rather perplexing one. Bank of Japan board member Naoki Tamura said that even if the Bank of Japan were to abandon negative interest rates, it shouldn’t be viewed as monetary tightening or a rate hike. His logic? Monetary conditions would stay loose regardless. This twisted reasoning left me scratching my head – if a rate hike isn’t a rate hike, then why do I bother analyzing rate hikes at all? (And why does this board member have a job?)

Wondering whether up is down and down is up in the upside-down world of central banking, I then stumbled upon a column arguing that with cooling jobs data, central bankers should move past their “fleeting and misguided infatuation” with labor market flows due to data quality issues. Traders were already known to dismiss the JOLTS figures as delayed, second-rate data. Why wait almost a month on JOLTS when the payrolls are coming out first Friday? And now central bankers are advised to look away as well? Why am I looking at numbers at all?

Yet, last time I checked, a rate hike is a rate hike, and central bankers are swearing by data-driven decisions. They have elevated relatively novel metrics like the V/U ratio as key data points, so there got to be at least a grain of importance in these numbers. So, perhaps against better judgement, let’s dive into those jolly JOLTs.

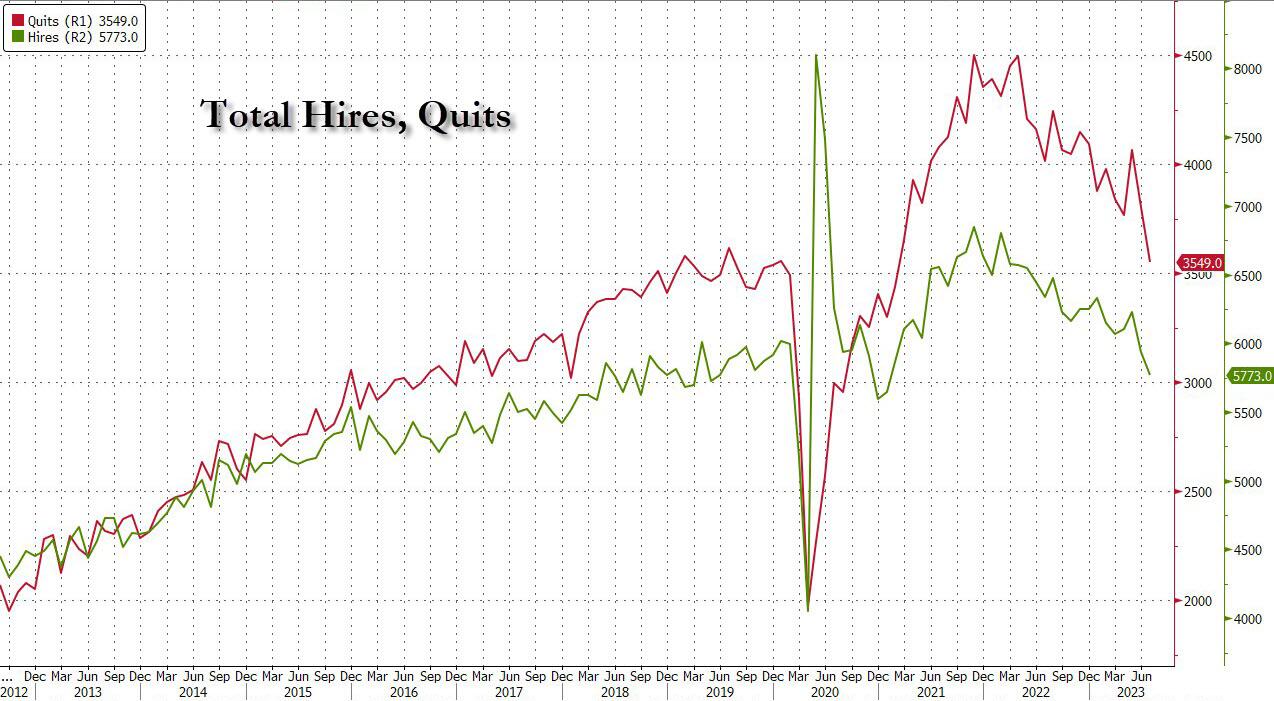

The headline was a sharp drop in vacancies to 8.83 million in July – the lowest since early 2021 and the sixth decline in seven months. The decline is accelerating. Over the past three months, 1.49 million openings have vanished, signalling rapidly falling labor demand. The labor market might be cooler still if you believe the number overstates real demand by including fake job openings. It has been reported that some companies post cheap online ads they might not really be trying to fill. That said, that V/U ratio of openings to unemployed has retreated to 1.51, down from almost 2 earlier this year.

Another measure points to normalization as well. The quits rate, which measures voluntary job leavers as a share of total employment, fell to 2.3%, the lowest since early 2021 and equaling the pre-pandemic average. The “Great Resignation”, or, better, the “Great Reshuffling”, with millions more workers quitting their jobs to take on better-paying jobs elsewhere is over. This reduced job-hopping suggests cooling wage growth in coming quarters, as employers feel less pressure to attract and retain workers.

The reduction in openings and quits is happening at the same time as layoffs remain at around all-time lows. This is a necessary ingredient for a soft landing. So that’s good news, but of course a soft landing is not secured. Given the monetary lags and a lot of policy pain still in the pipeline, there is no guarantee these labour market dynamics will suddenly stabilise at rates that are consistent with roughly 3% pay growth and 2% inflation. Indeed, in recent weeks the economic surprise index has been rolling over pretty quickly, taking place just as Wall Street went all-in on the soft landing thesis.

Coincidence or not, the Conference Board’s consumer-confidence index showed a renewed deterioration in sentiment. The headline rate fell to 106.1 in August from 114.0 in July. Crucially, the sub-index that measures how hard it is to get a job ticked up to 14.1, the highest since April 2021 – indeed, right before the Great Reshuffling – while the sub-index of those saying that jobs are plentiful fell to 40.3 from 43.7. This 26.2 point labour differential is a fresh low for this cycle and consistent with an increase in the unemployment rate. So, when consumers are telling the same tale, the JOLTS figures aren’t as flawed as some would suggest.

Tyler Durden

Wed, 08/30/2023 – 11:25

inflation

monetary

policy

interest rates

negative interest rates

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…