Economics

Fed Is Using Talk To Get The “Longer” In “Higher For Longer”

Fed Is Using Talk To Get The "Longer" In "Higher For Longer"

Authored by Simon White, Bloomberg macro strategist,

The Federal Reserve is…

Fed Is Using Talk To Get The “Longer” In “Higher For Longer”

Authored by Simon White, Bloomberg macro strategist,

The Federal Reserve is attempting to use the dots to reduce the size of the “pivot” expected by the market, so as to amplify the effect of rate hikes made so far and limit the need for further rate rises.

Higher for longer has been largely a chimera for central banks in this cycle. While the market has reluctantly priced in a higher peak for rates as the Fed et al hiked, it has brought that peak closer, and then priced in steeper cuts thereafter. The market’s message is: if you’re going to make the economy sick, then we better have the medicine ready.

Data released on Thursday pushed US yields higher, with almost one-and-a-half 25bps Fed hikes now expected by November. But progress on the “longer” part of higher for longer is lacking.

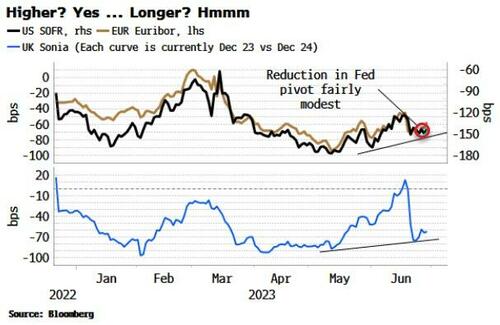

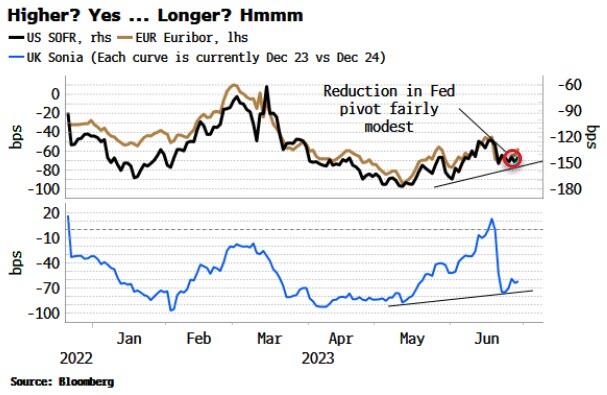

The SOFR curve is still inverted by 135 bps between Dec 2023 and Dec 2024. This has risen since May, but as the chart below shows, it’s still way below where it was just before the banking mini-crisis in March.

Similarly for the ECB and the BOE, where there are still sizeable cuts priced in for next year.

This is a problem for central banks, as the priced-in cuts dampen the transmission of monetary policy. Forcing rates higher becomes counterproductive if the market believes the economy is soon going to be plunged into a recession.

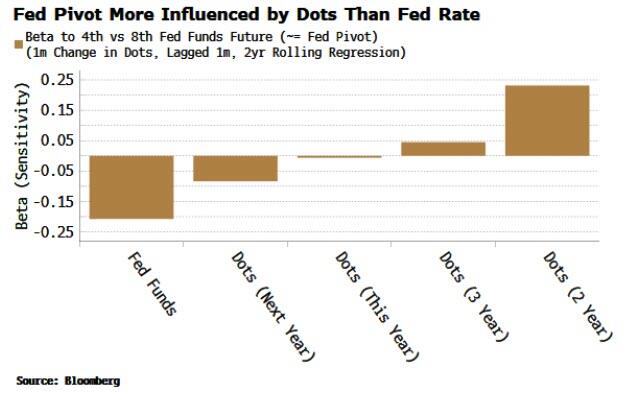

Which is why the hawkish rhetoric has been turned up a notch in a few weeks. The Fed earlier this month did not raise rates, but went out of its way to sound as hawkish as possible, raising its rate projections in the dots.

The dots, it turns out, have more impact on the depth of the pivot than the Fed rate itself. In fact, the Fed rate has a negative relationship with the shape of the curve after the peak rate, whereas the longer-term dot projections have a positive relationship. Words speak louder than actions when it comes to the pivot.

The ECB has turned up the hawkish dial too recently, shifting the goalposts from reining in core inflation to lowering unit labor costs.

But while ECB speakers have sounded deadly serious about the need for tighter policy, with a July hike a done deal, reading between the lines they still have wriggle room to not go in September.

The BOE’s plight underlines why talk over action, at this stage of the cycle, is a good strategy for central banks.

Even though the MPC surprised markets by hiking 50 bps in June, there are still more cuts priced in now than there were a few days before the rate rise.

Tyler Durden

Mon, 07/03/2023 – 08:30

inflation

monetary

markets

reserve

policy

fed

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…