Economics

Doesn’t Goldilocks Get Eaten In The End?

Doesn’t Goldilocks Get Eaten In The End?

Authored by Peter Schiff via Academy Securities,

Yesterday was a great “everything” rally day!…

Doesn’t Goldilocks Get Eaten In The End?

Authored by Peter Schiff via Academy Securities,

Yesterday was a great “everything” rally day! The market “finally” or “once again” got to price in a “soft landing”. It is possible that Goldilocks survives in the end, but growing up with Slavic folk tales, the stories rarely seemed to work out with “Hallmark” endings.

It started with a deluge of data.

-

ADP jobs were weak, but no one understands how their new methodology works.

-

The price and inflation components of GDP came in higher than expected, but not by much.

-

JOLTS, job opening were down, but better than expected (and still much higher than I find believable).

-

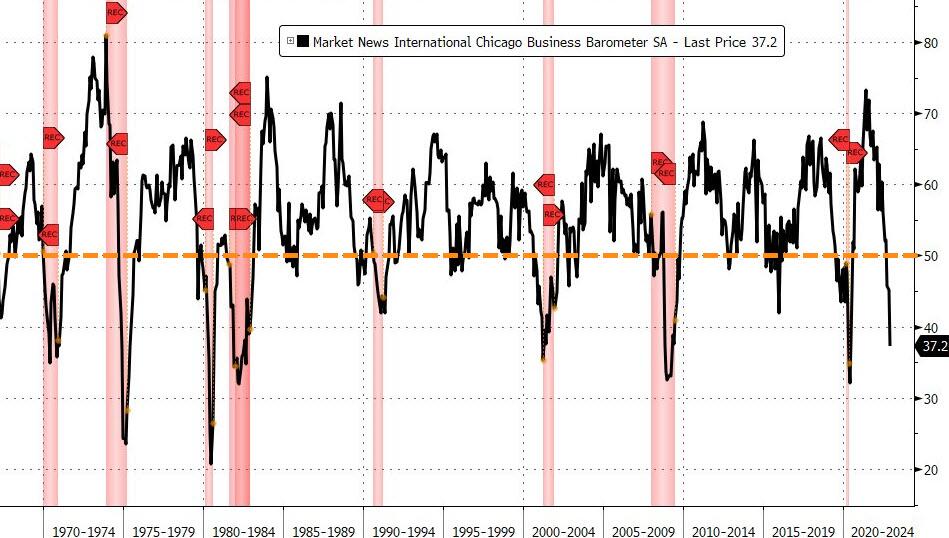

Chicago PMI was “Showgirls” bad! Maybe it is “specific” to the Chicago area, but this number stuck out like a sore thumb.

We only had worse data during the lockdown, in the aftermath of Lehman and at the height of the dotcom bubble bursting (and some fraud at massive IG companies). We will come back to this!

All that really mattered, was Powell.

-

Powell confirmed, what us and many other have been saying for some time, the pace of hikes has to slow! That the risk of overtightening is real (we think they already have overtightened, but that’s another story).

-

His words helped:

-

Lower the terminal rate to 4.9% according to Bloomberg WIRP. Still a touch high as discussed in this weekend’s Positioning & Key Drivers.

-

Sent the 2-year treasury from 4.55% to a low of 4.31%. The entire yield curve moved and we had some serious bull steepening (or less inversion). There should be more steepening to come!

-

The S&P 500 was up 3% with Nasdaq up 4.5% and the beleaguered ARKK ETF up 7.7%.

-

DXY, a dollar index had a weak day, which continued overnight, and is now the lowest it has been since August and could break through to levels not seen since June!

-

Even crypto participated, though the crypto rally started overnight. More on this another time as it is a sideshow for the moment.

-

We are also getting signs that China, while technically not submitting to the protestors, is submitting to the protestors. There are hints that China’s “official” policy is noticing changes in how COVID is affecting people, which would support a decision to ease restrictions.

Doesn’t Goldilocks Get Eaten in the End?

Back to the main theme of today’s quick report.

We have been looking for lower yields and admission by the Fed that they have potentially gone too far, too fast. We got that.

But what is next?

-

If for no other reason than we got an almost 5% rally in the Nasdaq, look for some Fed speakers to try and talk markets down. It won’t be horribly effective, but it won’t stop them from trying.

-

What if the PMI is a sign of things to come? What if, far from being an outlier, this is indicative of the direction the economy is headed? I remain staunchly in the camp that the recession is coming sooner and will be deeper than consensus. It will be driven by high paying jobs being lost, the wealth effect and the inventory overhang!

-

NFP should now be set up for a “bad news is bad” trade.

-

Don’t underestimate the power of daily and weekly expiration options to drive markets far more than they should be on days like yesterday. It is anyone’s guess on which way the traders driving the market with Friday expiration options will decide to try and drive the market, but after yesterday’s big move, where we started with relatively “neutral” positioning, trading to the downside on any catalyst seems easier than driving it much higher. But in any case this trading pattern has introduced a new randomness to the size of the moves (less so to the direction).

-

The quiet grind of QT continues. Liquidity, slowly, but steadily is leaving the system. Far less dramatically than how QE inserted the liquidity, but a likely headwind, nonetheless.

Bottom Line

Small fade on the rates move. Generally think front end yields are still too high and we should see steepening (less inversion).

Larger fade on the equity side. A China reopening would be a wildcard against this, but that, realistically is a spring thing and we have plenty of issues to deal with before then.

It is encouraging that the Fed is finally on the “nearly done hiking” page, but once that gets fully priced in (and it may already be), then we can move to the “done too much hiking already” phase, which won’t be pretty for risk assets (there was a time, in a galaxy far away, where “risk-off” was a thing and stocks did poorly as yields went lower.

The market is in the “just right” stage of the 3 bears story, but I don’t think that is how the story ends!

Tyler Durden

Thu, 12/01/2022 – 09:45

dollar

inflation

markets

policy

fed

bubble

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…