Economics

CPI Preview: Inflation Is Cooling But Will It Be Enough

CPI Preview: Inflation Is Cooling But Will It Be Enough

As discussed earlier, most banks agree that while the midterms are important over…

CPI Preview: Inflation Is Cooling But Will It Be Enough

As discussed earlier, most banks agree that while the midterms are important over the medium and long run, Thursday’s CPI print will be the most important factor to shape the expectations for December FOMC and the market’s near term reaction. Here, courtesy of Newsquawk, is what to look for.

- Analysts expect headline consumer prices to pick up by 0.6% M/M in October, accelerating from the 0.4% M/M rate in September while the core measure is seen cooling to 0.5% M/M, lower than the 0.6% M/M in September, but a still elevated level vs historical levels.

- On an annual basis, headline CPI is expected to rise 7.9%, down from 8.2% last month; core CPI sill also slow to 6.5% from 6.6%.

- The data will be framed in the context of how much progress the Fed is making towards lowering inflation. After the November FOMC meeting, Fed Chair Powell said it was “very premature” to consider pausing or ending the rate hiking cycle, noting that inflation remains well above the Fed’s longer-run goals, with price pressures evident across goods and services. Although longer-term inflation expectations still appear well-anchored, the Fed wants to see inflation coming down decisively, and is prepared to stay the course until the job is done.

As a reminder, the message from Powell last week was that the Fed is strongly committed to its inflation target of 2%. Powell did, however, allude to a potentially slower pace of rate hikes in December – the statement said the Fed will consider the “cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments” when determining the pace of future rate increases. Analysts rationalised that with rates in restrictive territory, the Fed can downshift to a slower pace of normalization to assess the impact of the 375bps worth of rate tightening unleashed since March.

Currently, the market is split in its views about whether the Fed will implement a 50bps or 75bps rate hike in December.

Accordingly, the market seems to be of the view that if inflation metrics move lower (and traders are keeping an eye on aggregate inflation data, including CPI, PCE, wages metrics within jobs data, consumer inflation expectations via surveys, etc), this gives the Fed cover to downshift to the lower increment. However, if inflation data does not cooperate, then the Fed will prefer the larger sized hike, and potentially an even a higher terminal rate (Powell suggested that the eventual peak Fed Funds Rate Target is above the 4.6% pencilled in within the September projections; money markets see the peak at 5.00-5.25% in Q2 2023).

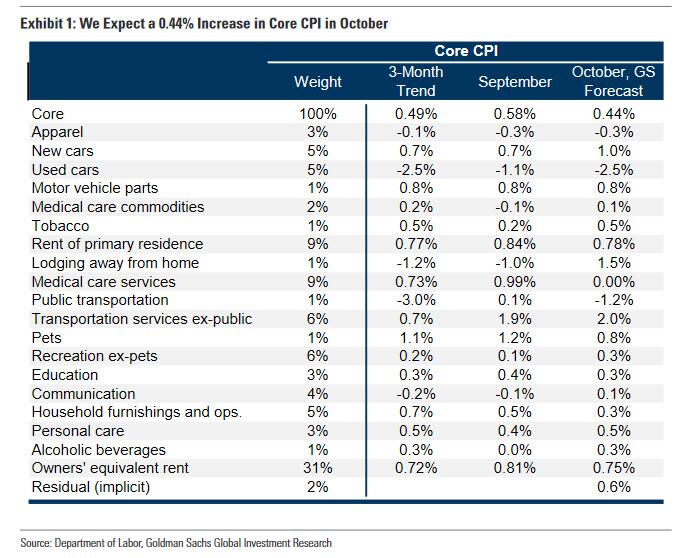

Shifting away from the consensus, we next focus on what Goldman’s economists expect from tomorrow’s print. As discussed in the preview from Jan Hatzius (available to pro subs), Goldman expects a below-consensus 0.44% increase in core CPI in October (vs. 0.5% consensus and 0.6% prior), which would lower the year-on-year rate to 6.46% (vs. 6.5% consensus and 6.6% prior).

The bank expects moderate increases in both food and energy prices to raise headline CPI by 0.49% (vs. 0.6% consensus and 0.4% prior), which would lower the year-on-year rate to 7.8% (vs. 7.9% consensus and 8.2% prior).

The bank’s research team also highlights 3 key component-level trends this month:

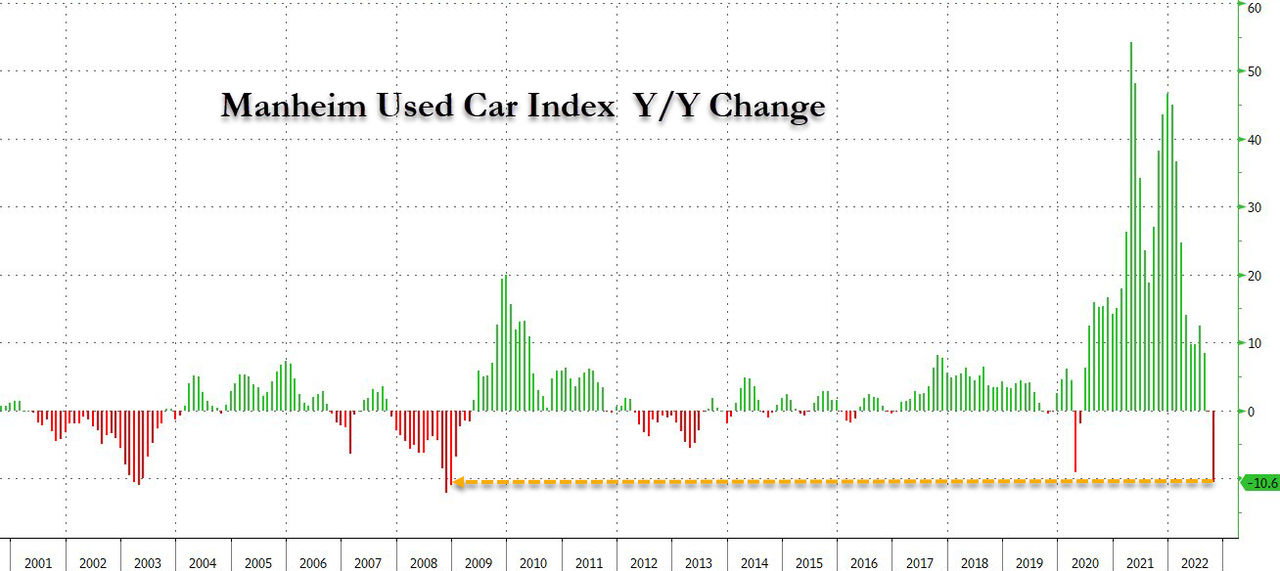

1) Expect CPI used car prices to catch down (-2.5% in October) to auction price data, which have now plunged substantially from their peak, and just tumbled at the 3rd fastest pace on record.

2) The small but volatile health insurance component should finally swing from providing a large boost over the past twelve months to providing a large drag over the next twelve months (-3% in October) with the incorporation of new data on health insurer profit margins. The reason is that the CPI incorporates source data on health insurer profitability once per year and feeds them through for the next twelve months. Last year, roughly stable premiums coupled with reduced health care use amidst Covid fears caused profit margins to rise, leading to a year of very strong health insurance inflation (+2.1% in September; +28.2% year-on-year). Now, the rebound in health care use has caused profit margins to fall, which should lead to a year of very negative health insurance inflation (-3% in October; -28% next twelve months). That would cause the contribution to the core from this small component to fall by 65bp over the next year.

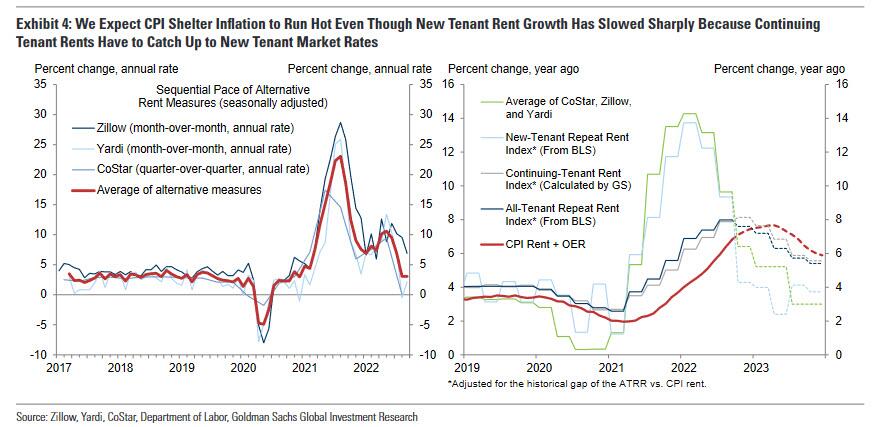

3) Goldman also expects shelter inflation to run hot (rent +0.78%, OER + 0.75%), even though as we discussed extensively, real-time alternative web-based measures of new tenant rent growth have slowed—because continuing tenant rent levels still have a long way to catch up to new tenant market rates. In other words, rent inflation will keep coming in hot even as prices slump outside of excel models.

Elsewhere, Goldman also expects a 2% pullback in airfares based on timely data and also expects another large increase in the car insurance category (+1.6%), as carriers push through price increases to offset higher repair and replacement costs.

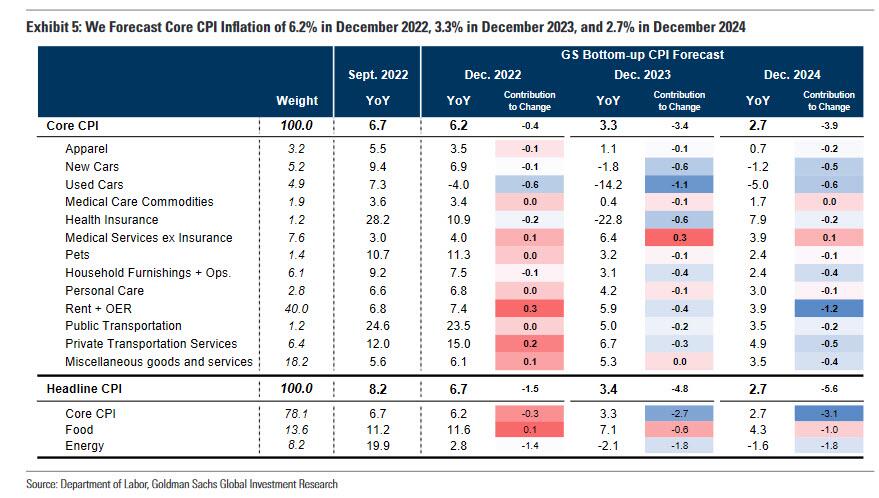

Going forward, the bank expects monthly core CPI inflation to remain in the 0.3-0.4% range for the next couple of months before edging down to 0.2-0.3% next year. Goldman expects year-over-year core CPI inflation of 6.2% in December 2022, 3.3% in December 2023, and 2.7% in December 2024. The deceleration we expect in 2023 is driven more by goods than services categories. Of course, a sharp recession will unleash deflation much sooner.

Shifting from Goldman to JPM, this is what its head economist Mike Feroli said in his preview:

We estimate that the consumer price index (CPI) rose 0.6% in October. Even with this strong increase expected for the month, we think year-ago headline inflation will moderate, from 8.2% in September to a still-robust 7.9% in October. The headline strength should come in part from energy prices, for which we forecast a jump in October following a run of three straight monthly declines. We think that food prices continued to climb into October, but we expect additional moderation in this CPI aggregate (following a very strong run), with the food CPI up 0.6% in the month. Away from food and energy, we forecast that the core CPI rose 0.38% in October, with this measure coming in 6.4%oya (down from 6.6% in September).

We think that continued firmness in the CPI’s rent measures will drive the expected gain in the core aggregate in October. While we think rental inflation will moderate eventually, we don’t see this happening at this point in time, and we forecast that tenants’ rent rose 0.83% in October while owners’ equivalent rent increased 0.76%.These gains would be a little softer than the reported September changes but still quite firm.

Away from rent, we expect softer changes in many of the other main CPI components. Auto industry figures point to recent declines in related prices (particularly for used vehicles) and we look for new vehicle prices to be down 0.1% in the October CPI while used vehicle prices fell 2.2%. We also think that airfares declined in October, which would help push the broader public transportation price index down 2.2%. Apparel prices came down a bit in September and we forecast another modest decline in October, with prices down 0.2%. We also think that communication prices will keep trending lower, with a 0.1% move down reported for October.

We also expect a noticeable downshift in medical care inflation in the CPI, with the BLS set to incorporate an annual update to source data used to estimate health insurance prices. We think overall medical care prices edged up just 0.1% in October, with a near-4% drop in health insurance prices being offset by gains in other related prices on net. This would represent a big shift from the past 12 months, which had monthly gains in medical care prices averaging 0.5% with health insurance prices up about 2% per month. We also look for a fairly modest gain in lodging prices in October, with a 0.3% increase expected to offset a portion of September’s 1.0% decline.

Turning to the market, in terms of the S&P’s reaction function to the headline CPI YoY print here is framework Goldman’s John Flood is using using:

- >8.2% S&P loses 3+%

- 8 – 8.2% S&P loses 1-2%

- 7.8 – 7.9% S&P gains 0 – 1%

Finally, as discussed earlier, JPM was much more hyperbolic in its CPI market scenario analysis:

- CPI 8.4% or higher: this would be a move back to July levels of inflation, which we may see on a MoM basis but think Equity investors care most about the Headline YoY level. This would represent the largest differential between actual and estimated in this cycle. SPX would plunge 4.5% – 6%. Probability 5%

- 8.1% – 8.3%: there have been 4x misses of 20bps or more and the SPX fell 1.6%, 2.9%, 40bps, and 4.3% which is a down 2.3% average. The 40bps outlier came when the SPX was ~3820 the day before the print. In the other 3 cases, the SPX was between 3930 and 4000. SPX would drop 2% – 3%. Probability 30%

- 7.9% – 8.0%: I think bonds, and thus stocks, take this as a small positive since it meets expectations and does not reprice yields higher. Given that we are at the bottom of JPM’s Cash Trading team’s range (3700 – 3900), we may see some covering leading to an uptick in stocks. SPX would rise 1% – 1.5%. Probability 40%

- 7.7% – 7.9%: this could be similar to the August 10 print which had a dovish beat by 20bps and triggered a 2.1% rally in SPX, 2.8% in NDX, and 2.9% in RTY. Cyclicals, Value Shorts, Momentum Shorts, and ARKK the best performers that day. Given the increased bearishness, the magnitude of move could be larger. SPX higher 2.5% – 3.5%. Probability 20%

- 7.6% or below: a stepdown in inflation of this magnitude likely pulls the 10Y yield below 4% (currently 4.158%) and triggers a sharp rally in stocks. This may also reset the yield curve lower with terminal rate expectations falling under 5%. SPX higher 5% – 6%. Probability 5%.

Looking at historical data the past year has seen a decidedly negative reaction to CPI on the day of the report, however when CPI came in below expectations, the SPX is up 0.8%, but down -1.2% when the CPI comes in hotter than expected.

And while there have been decidedly few CPI misses in the past year, any time they do happen they lead to a powerful 5-day rally, certainly more powerful than the drop when CPI comes in hot.

As always,all full reports discussed above are available to pro subs.

Tyler Durden

Wed, 11/09/2022 – 21:30

inflation

deflation

monetary

markets

policy

fed

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…

{kind=link}