Economics

Ch-ch-ch-ch-Changes

Ch-ch-ch-ch-Changes

By Peter Tchir of Academy Securities

Time may change me, but unlike David Bowie, we can trace time (or at least what…

Ch-ch-ch-ch-Changes

By Peter Tchir of Academy Securities

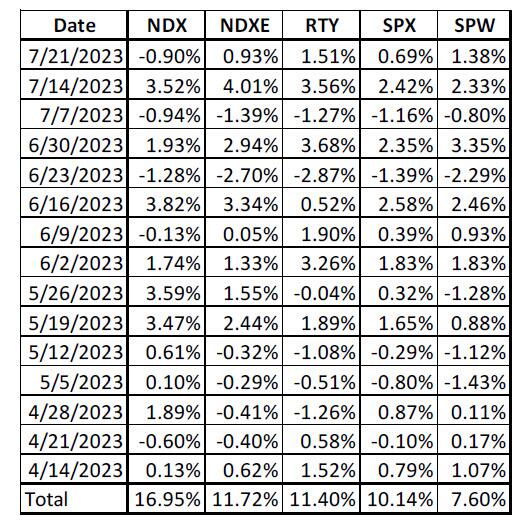

Time may change me, but unlike David Bowie, we can trace time (or at least what went on over time). Let’s look at some weekly performance data for the Nasdaq 100 (NDX), the equal weighted Nasdaq 100 (NDXE), the Russell 2000 (RTY), the S&P 500 (SPX), and the equal weighted S&P 500 (SPW).

The Nasdaq has been leading the charge, but while it went up every week from late April until early June, the performance has been more inconsistent as of late. For the past 3 weeks, the Nasdaq 100 has provided the lowest return of the group (around 1.5% versus almost 4% for the Russell 2000).

What I find most interesting is the performance of the “equal weighted” indices. The Nasdaq equal weighted index outperformed the Nasdaq by 1.8% on the week (its largest weekly outperformance going back to at least the beginning of April). It was the 2nd week in a row (and 3 out of 4) where the equal weighted index did better. We are seeing a similar story line in the S&P 500, where the equal weighted index has also outperformed 3 out of the last 4 weeks after an extended period of underperformance.

Between the outperformance of the Russell 2000 and the equal weight indices, I’m optimistic that piling into the “compression” trade described last week is the correct trade.

Both the S&P 500 and the Nasdaq 100 indices were changed at Friday’s close. The index providers were attempting to reduce the concentration risk of the largest holdings. If you pulled up QQQ (a Nasdaq 100 ETF), MSFT and AAPL were both over 12% of the portfolio. While index providers likely had to buy in that proportion, it made it very difficult (for those trying to run a diversified portfolio) to hold the “appropriate” amount of the mega-caps. For example, the concentration risk of a handful of names at market weight could violate their bylaws. So, what should have happened (as I understand it) was that at the close of trading on Friday, there should have been a large selling of a handful of names offset by an equal amount of buying across the other names.

Most indexing companies (which focus on “tracking error”) presumably waited until near the end of the day on Friday to execute their trades. Some may have tried to add “alpha” by getting ahead of the re-weightings, but I suspect that this group is only a small portion of index funds. This strategy introduces tracking error, which causes more harm than any “incremental good” created by adding “alpha”.

So, my working assumption is:

- The weakness in the Nasdaq 100 (down 0.9%) can be partially attributed to many investors selling the big names ahead of Friday’s re-weighting.

- The bulk (but not all) of the outperformance of the equal weighted indices last week can be attributed to this change in weightings (and investors getting ahead of it), but the trend seems to be bigger than just this.

We will have to watch how the market behaves early next week to determine if practitioners will continue to sell the big stocks and buy the smaller stocks or if what we saw recently was just asset managers getting ahead of the rebalancing. I think that it will be the former rather than the latter.

One weird “paradox” in this so-called passive world is that if we see outflows from Nasdaq 100 funds, the selling of shares will now hit the laggards more than the behemoths. It seems like a paradox to me, since that is not the intention of the rebalancing, but it will be a consequence if we see outflows.

The debate between equal weight and market weight shines a light on how “passive” following an index strategy truly is. Sure, following the index is passive, but picking the index to track is far from passive and it is not without total return repercussions.

I continue to like the laggards and I am pretty neutral on the market as a whole. I’m reluctant to bet against the market, even though it is now crowded from the long side. However, during the slow summer trading sessions, the likelihood is that the current trends will continue.

Is There a Fed Meeting This Week?

Yes, there is a Fed meeting, but I expect to learn very little. We will get a 25 bp hike, lots of chatter about data dependency, and questions about the long and variable lags. I’d be shocked if anything changes my view that:

- The Fed has a high hurdle to hike again this year.

- The Fed has an extremely high hurdle to cut this year.

Moving forward, I just don’t see monetary policy as the market force that it has been for the past year and a half.

The MOVE index (a measure of bond market implied volatility) continued to decline and I think that it will drop significantly after the Fed meeting.

The yield curve actually inverted more last week (2s vs 10s is now back to more than 100 bps negative). The 2-year Treasury yield crept moderately higher, while the 10-year did very little.

The only “excitement” that we could get out of the Fed is if they change their balance sheet reduction plans, but I cannot see them doing that at this meeting.

Credit Doing Well

Credit spreads tightened a touch across the board and there is more room for spread tightening. Once banks are done with their post-earnings issuance, the calendar should be quite slow into August and there is so much “cottage industry” chatter about how credit is overpriced that the pain trade seems to be marginally tighter spreads.

Bottom Line

I think that the Fed meeting will be (relatively) a non-event.

On the economic data front, I think that we will see signs of weakness, but it won’t be universal and won’t start sinking in until next month’s jobs numbers start coming out. This week, unless there is something “shocking”, it will have been “baked into” the Fed decision so the meeting shouldn’t move markets.

I really think that the “compression” trade or the “laggard rally” has legs, but we will be keeping a close eye on that.

Earnings will be key. Earnings will determine whether the overall market rally continues (or not) more than anything else (unless there is some unexpected geopolitical event). Given it is late July, I think that the rally continues, but the leadership changes.

On a separate (and less pleasant) note, please see our recent SITREP – Russia Threatens Shipping, which fits well with our recent pieces on Commodity Wars.

In the meantime, I’m hoping to be able to include “Young Americans” by Bowie in a “thought piece” later this week (which, interestingly, mentions Barbie). I hope that you have a great weekend whether or not you participated in “Barbenheimer.”

Tyler Durden

Mon, 07/24/2023 – 08:08

commodity

monetary

markets

policy

fed

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…