Economics

Can Italy revive ailing economy with Russian rubles?

Even though the Italian economy has largely returned to positive growth in recent quarters, it has struggled to maintain momentum since the strong one-off…

Even though the Italian economy has largely returned to positive growth in recent quarters, it has struggled to maintain momentum since the strong one-off rebound post global lockdowns.

Data from the IMF World Economic Outlook shows that Italian GDP at constant prices fell by 8.9% in 2020, which in turn supported the 6.9% increase in 2021.

However, following the diminished base effect, growth in 2022 moderated to 3.6%.

IMF forecasts suggest that full-year growth for 2023 will be subdued at 0.7% while GDP growth is unlikely to exceed 1% until 2025.

In terms of industrial production, the Italian Institute of Statistics (ISTAT) reported that the three-month industrial production index continued to deteriorate in Apr-June 2023, declining 1.2% compared to the previous interval.

Although consumer inflation has moderated since hitting nearly 12% YoY in Oct-Nov 2022, as of July 2023, it is still at elevated levels of 5.9% YoY.

Following global disinflationary trends, declines were seen across the board, with goods falling from 7.5% YoY in June 2023 to 7.0% in July 2023, and services seeing a similar reduction from 4.5% YoY to 4.1% YoY.

In terms of special aggregates, energy products eased meaningfully from 2.1% YoY in June to 0.7% YoY this month.

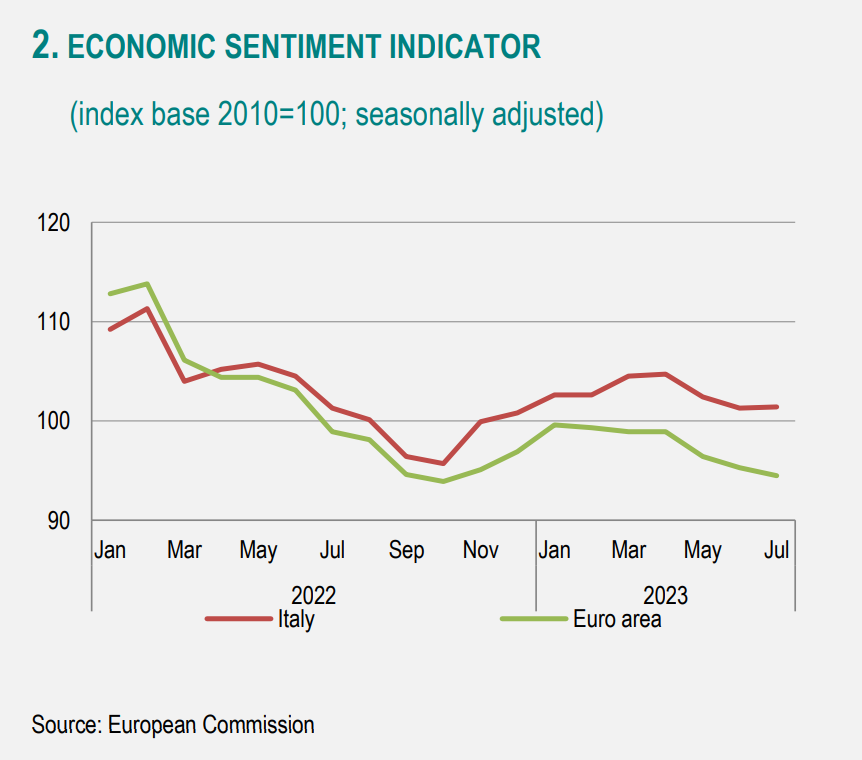

Encouragingly, the Economic Sentiment Indicator for Italy remained broadly stable, rising 0.1 points since last month, while the euro area declined by 0.8 points.

The Institute noted that the economy was dominated by mixed signals such as an improvement in consumer sentiment but a deterioration in business sentiment.

In addition, the majority of the workforce and small businesses remain vulnerable to the global environment as central banks are poised to continue to tighten monetary policy.

Italian-Russian trade flows in dire straits

In 2023, external trade for Italy has been a relative bright spot for the economy, with ISTAT noting a 6.9% YoY improvement in January-June exports.

Robust growth in outbound goods enabled Italy to accumulate trade surpluses of nearly EUR 6 bn in the first third of the year, compared to a deficit of EUR 12.4 bn in 2022.

Cumulative trade balances from January to June 2023 ballooned to EUR 26.1 bn.

However, this seemingly pleasant picture masks the devastation that occurred in the crucial trade channel with Russia, upon which Italy’s very survival has been dependent.

Historically, Russia has been the primary exporter of energy products to Italy, which in turn, fuelled the country’s competitive manufacturing sector and an important market for Italian-made goods.

Yet, this synergy has been short-circuited since the rollout of Western sanctions in response to the Ukraine war.

In an interview with RIA Novosti, Ferdinando Pelazzo, President of the Italian-Russian Chamber of Commerce, a 350-member organization that has been active since 1964, clarified that these sanctions do not apply to financial flows between Italy and Russia, but instead, to select goods.

Accordingly, 49% of Italian exports to Russia are non-sanctioned and can theoretically be sold to Russian companies, without objection.

Yet, the now common practice of excluding Russian banks from SWIFT, the international network which is used to communicate payment orders, has made it extremely challenging for customers to pay for Italian imports.

Intermediary banks that would ordinarily have transferred funds from Russia to Italy are electing to block these transactions.

Consequently, Russian banks and customers are unable to raise the euros to participate in trade.

A trade relationship, imploded

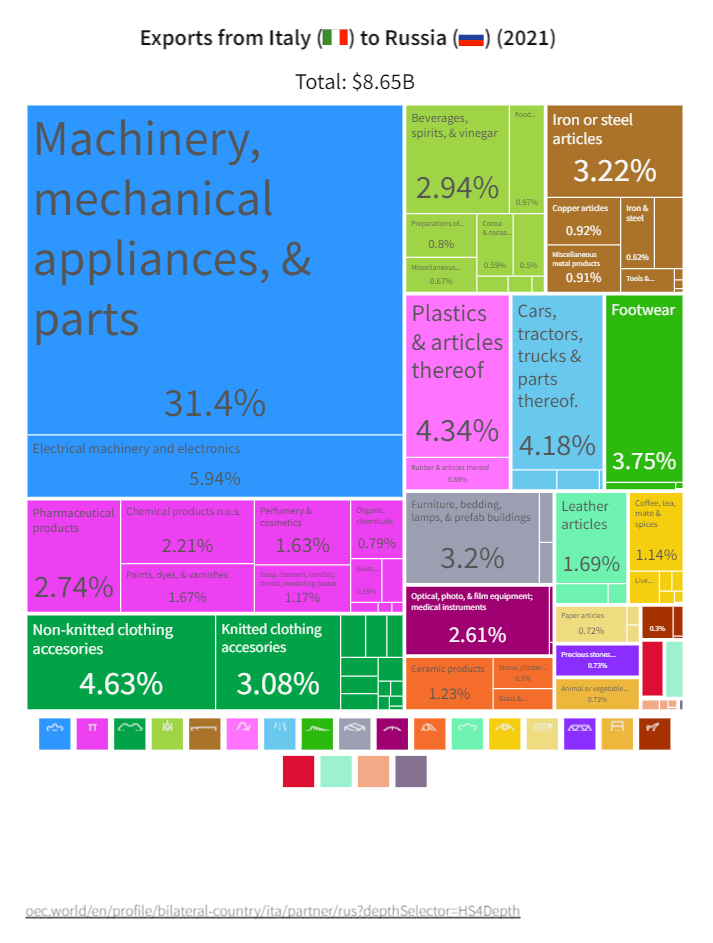

As per the Observatory of Economic Complexity (OEC), Italian exports to Russia were worth $8.65 bn in 2021.

These exports were highly disaggregated and dominated by machinery, mechanical appliances, and associated parts, which made up 31.4% of total exports to Russia in dollar terms.

Non-knitted clothing accessories; plastics and related articles; and cars, tractors, trucks, and related parts, each comprised more than 4% of the aggregate.

Wine exports accounted for 2.1% of total exports at $182 mn in 2021.

Consistent Russian purchases were vital to the survival of these businesses as most Italian enterprises are small producers and relied heavily on targeted relationships with specific clients.

Each month, the ISTAT publishes updated trade data sliced by partner country.

Current situation

For May 2023, the ‘Foreign Trade with Non-EU Countries’ report showed that this bilateral trade link virtually collapsed.

Italian exports to the Russian Federation were sharply down by 32.6% YoY and suffered a significant decline of 15.6% on a cumulative basis in the first five months of the year.

The updated numbers for June 2023 continue to paint a bleak picture, showing a year-on-year decline of 27.5% and an even deeper cumulative loss of 17.8%.

By and large, most Italian exporting companies lack the capacity to maintain relationships in sophisticated banking circles, are unable to navigate such delicate geopolitical situations and are not equipped to source opportunities in new markets.

This has proved to be a major body blow to small and medium Italian export businesses.

A 2021 report from the European Investment Bank highlights the potential scale of the problem.

The study found that 80% of employment in Italy comes from small and medium enterprises, of which 95% is from micro-enterprises.

Micro-enterprises are defined as having fewer than 10 employees and a turnover of under EUR 2 mn per year.

Together, these enterprises account for 53% of all exports, well above the EU average of 40% and twice that of either France or Germany.

In case that sounds bad, the June report showed that compared to year-ago figures, Russian imports were decimated by an unfathomable 90.3%.

Brutal energy sanctions pulled vital supplies into the doldrums.

On a cumulative basis, for the first six months of the year, Russian imports plummeted 83.6% compared to 2022, all but vanishing into thin air.

Pelazzo reflected on just how far-reaching these sanctions proved to be,

Exports from Russia are easier: gas, chemical products…large companies that have long had certain connections with the banking sector, this is easier for them.

Italy’s heavy dependence on Russian energy

Energy has been the centrepiece of Italian-Russian trade relations for decades.

Much of the decline in trade volumes can be attributed to the impact of direct sanctions on energy exports.

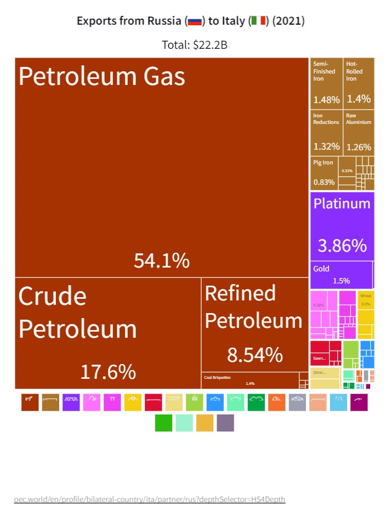

The OEC data shows that before the Ukraine war, in 2021, exports from Russia to Italy were heavily concentrated, with 81.7% (in dollar terms) being comprised of mineral fuels and associated products such as petroleum gas, crude petroleum, refined petroleum, and coal.

According to Statista, Russia supplied 29.2 billion cubic metres of natural gas to Italy in 2021, making up approximately 40.5% of total natural gas imports.

Another data point from Statista shows that the country’s natural gas dependency stood at 94.3% in 2020, and has remained over 90% since 2015.

This refers to the proportion of imports required to maintain the Italian natural gas complex, implying the country is almost completely dependent on the overseas market.

Italian energy imports since the war

Despite the standoff between Russia and the G7 countries, the graph below shows data from CREA’s Russia Fossil Tracker regarding aggregate purchases of Russian fossil fuels since the outbreak of the Ukraine War till the 5th of August 2023.

Kindly note that I have calculated the totals by addition of the fossil fuel components which include coal, oil, and gas.

This data suggests that Italy has been highly dependent on Russian energy imports even after the war began, particularly with the emphasis on topping up its energy storage ahead of the previous winter.

In aggregate, the country was the third largest consumer in Europe behind Germany and the Netherlands, and the sixth largest in the world.

In terms of oil and coal, Italy imported 10% and 12.4% of aggregate European oil imports from Russia, respectively, ranking third in the EU for both commodities.

In terms of gas, this was 10.2% of European imports since the war began, coming in fourth behind Germany, Hungary, and Austria.

As per a report on Italy published by the International Energy Agency,

Italy’s energy sector is strongly reliant on fossil fuel imports from the Russian Federation, which in 2021 accounted for one-third of total energy supply (TES) of fossil fuels.

However, post the sanctions, Italy has taken considerable steps to reduce its dependence on these energy sources.

Thus, smaller businesses are facing pressure from both the SWIFT curtailments and Italy’s energy and foreign policy.

Delinking from Russian gas in 2023?

Since February 2022, the US, EU and G7 have placed severe sanctions on Russia’s exports, which curbed earnings by limiting access to finance, capital investments, and new technology, as well as implementing an oil price cap.

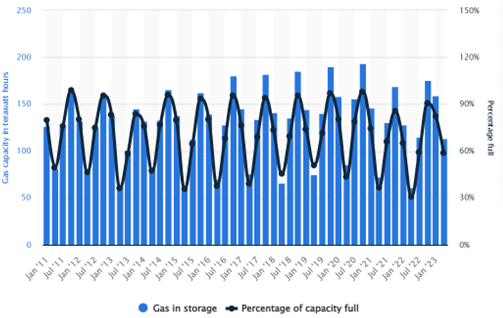

Fearing that Russia could stop supplying gas to the country at a moment’s notice, Italian officials scrambled to top up gas storage tanks ahead of the winter season, while security breaches in the case of the Nord Stream pipelines only served to heighten the urgency.

90.7% of the country’s gas storage capacity was filled as of October 2022 against a record low of 30.9% as recently as April 2022.

This improvement is borne out from the Russia Fossil Tracker which shows that the government was forced to continue to import vast volumes of energy from Moscow.

Several other measures were rolled out to reduce oil consumption for transport, new incentives for EV adoption, promotion of alternative fuels, and sizeable energy efficiency investments.

In Q1 2023, Qatar and the U.S. shipped vast amounts of LNG to Italy, accounting for 39% and 28% of the total supply, respectively.

In an April 2023 interview with Corriere della Sera, Italian Environment and Energy Security Minister Gilberto Pichetto Fratin, noted,

Previously, we used to obtain 40% of our gas needs from Russia, but today we only rely on them for a little over 10%. As a result, we have successfully reduced our dependence on Moscow.

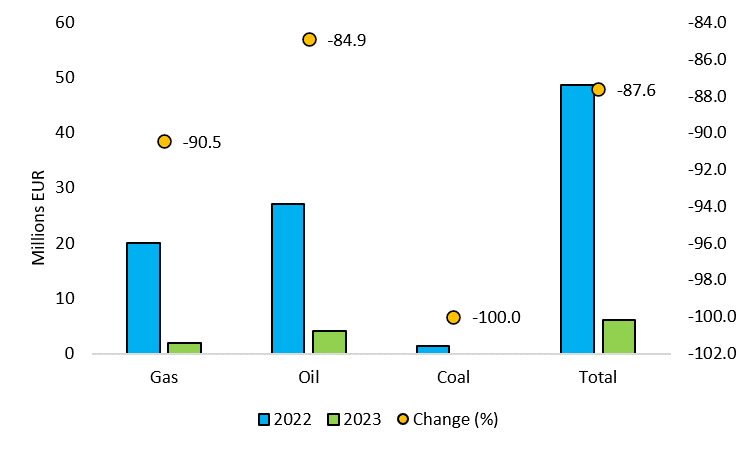

As of 5th August 2023, estimations from data provided by the Russia Fossil Tracker show that year-to-date, average Italian daily purchases of energy products fell drastically from EUR 48.6 mn in 2022 (since the war) to EUR 6.0 mn in 2023.

This implies an 87.6% reduction in average daily spend but must be interpreted with some caution since this refers to expenditure on a variety of products, continuously changing market prices, the introduction of oil price caps, the improved position of gas-storage tanks and the exit from winter.

The government achieved this reduction primarily by formalizing new agreements with Algeria and Libya, as well as relying on the Trans-Adriatic Pipeline (TAP) which sources gas from Azerbaijani fields to the tune of 2,249 mcm in Q1 2023.

The Italian government also committed to building two new LNG terminals, which are expected to come online by 2024.

It should be noted that although Italy is determined to minimize Russia’s hold over its energy security, April 2023 gas storage levels dipped to 58.6%, which may once again pressurize the country closer to winter.

In addition, an explosive report by Ana Maria Jaller-Makarewicz of the Institute for Energy Economics and Financial Analysis earlier this month, argues that 202 mcm of gas that was purchased by Italy during Q1 2023, had an unknown origin and may have been Russian gas routed through Spanish terminals.

A solution to bilateral trade

The Italian-Russian Chamber of Commerce actively promotes interstate cooperation, economic partnerships, and cultural ties.

The organization is in the process of developing a ruble-based payment mechanism to kickstart diminished trade flows between the two countries to support the unsanctioned space.

To prevent a further collapse in volumes, the Chamber is attempting to operationalize a financial channel that would enable Russian companies to purchase Italian goods by depositing ruble payments in banks located in favourable third countries.

Once this step is achieved, euro payments would be forwarded directly to business accounts in Italy.

Such an arrangement would allow parties to trade authorized goods without violating sanctions while also circumventing potential disruptions in the SWIFT network.

To make this a reality, Pelazzo notes that the Chamber will be looking to register as a ‘payment agent,’ and draw upon the organization’s long history and ‘fairly high reputation’ to instil confidence in Russian buyers.

To do so, the Chamber is approaching the respective central banks of potential partner countries.

Building a sound working relationship with the financial regulator would be key to ensuring that the arrangement can be closely monitored and any future pitfalls are minimized.

For example, the Chamber must assure authorities as well as partner banks, that it will be equipped to prevent any illegal financial flows to pass through the system, such as in the case of money laundering.

Dezan Shira and Associates, a pan-Asia, multi-disciplinary professional services firm, noted that Turkey, Armenia, and Dubai may be suitable choices to complete the currency exchange from rubles to euros.

Although the chamber has provided an innovative solution, setting up such a channel will take many months, during which time, ailing Italian businesses would continue to suffer and may be pushed closer to bankruptcy.

Potential responses of European countries

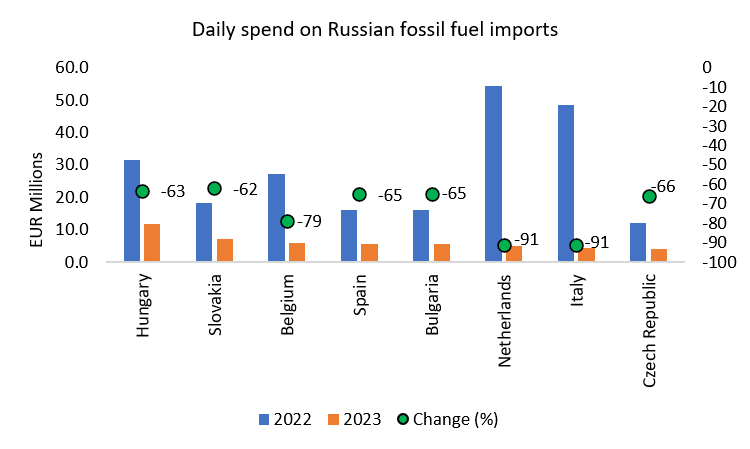

This data reflects the average daily spend on Russian fossil fuel imports by each country since the outbreak of the Ukraine War till the end of 2022 (‘2022’), and from January 1, 2023, to 5th August 2023 (‘2023’).

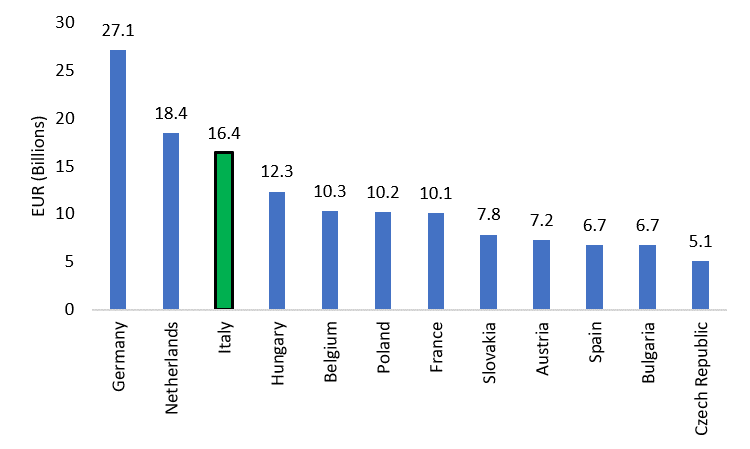

Of the eight countries represented, The Netherlands and Italy were the leading purchasers of Russian fossil fuels in 2022, but in 2023, have been replaced by Hungary and Slovakia, respectively.

Hungary leads the pack, having purchased a total of EUR 2.5 bn of Russian fossil fuels in 2023, accounting for 12.5% of EU imports from the country, nearly double the 6.9% registered in 2022.

However, it must be re-emphasized that all countries have seen marked declines in such Russian imports in 2023 compared to 2022.

Potential supporters

Each of these countries is acutely aware that lasting dependence on Russian energy could prove dangerous, either in terms of economic security or in drawing the ire of Western governments.

Yet, they are not able to switch overnight and current import levels may act as a proxy for their willingness to extend Russian economic integration with Europe.

For instance, Hungary and Slovakia, both negotiated exceptions to the EU-Russia oil embargo.

Further, a recent RFERL report noted that Bulgaria became the third-largest buyer of Russian oil in the world in 2023.

All three of these countries have generally called for a less strict approach towards anti-Russian sanctions, and are likely to support Italy’s attempts at a new mechanism to circumvent financial hurdles in trade flows.

In a Eurobarometer survey published in autumn last year, Hungary, Bulgaria and Slovakia were at the bottom end of the spectrum on public support for actions against Russia, coming in at 56%, 49% and 47%, respectively.

It should be noted that the same question also enquired about providing military, financial and humanitarian aid to Ukraine.

However, a recent change of guard in Bulgaria saw the Nikolai Denkov-led government assume charge in June 2023, which has so far positioned itself in a largely pro-Ukraine position.

This included signing an agreement earlier last month to supply approximately 100 armoured vehicles to the war effort.

Although the government is likely to support the new payment mechanism for now due to its heavy reliance on Russian oil, this administrative change may raise some doubts about the country’s position on the matter in the months to come.

In the case of the Czech Republic, it remains one of the leading importers of Russian energy in 2023, despite it assuming an increasingly anti-Moscow stance.

Dependence on Russian gas is estimated at 90% of Czech requirements, and 50% in the case of Russian crude, which would likely combine to supersede other considerations.

Earlier this year, the government adopted the Sanctions Act, to accelerate unilateral measures against select individuals such as asset freezes and restricting the use of Czech financial networks.

Although significant, such measures are likely to have little impact on the business environment.

The country would remain heavily dependent on Russian imports at least until linked to the Transalpine Pipeline in 2025, which also runs through Italy, Germany, and Austria.

This may imply that the government would be pressured to extend quiet support to continued economic integration with Russia in the interim.

Another potential supporter of the Chamber’s move may be Spain, which has seen Russian LNG imports peak as recently as April 2023 at over 6,500 GWh, registering an incredible three-fold increase since January 2022.

Spanish re-exports of Russian LNG to Europe have proved highly profitable and will continue to find support in the government.

Belgium too continues to benefit from Russian energy supplies, with the IEA noting that Brussels had a 25.6% reliance on the country in 2021.

In this case, reliance is defined as the ratio of Russian imports to domestic fuel consumption.

Earlier this year, Roger Housen, a former colonel in the Belgian army, made some controversial remarks, and stated,

…from the end of February to the end of September the value of goods and services imported from Russia rose by 130% compared with the comparable period the previous year…. we are one of the main sponsors of Russia’s war.

Belarus has been a key economic partner of Russia; they share close cultural ties while the country has also been subject to sanctions such as prohibitions on receiving euro-denominated banknotes from overseas.

Possible detractors

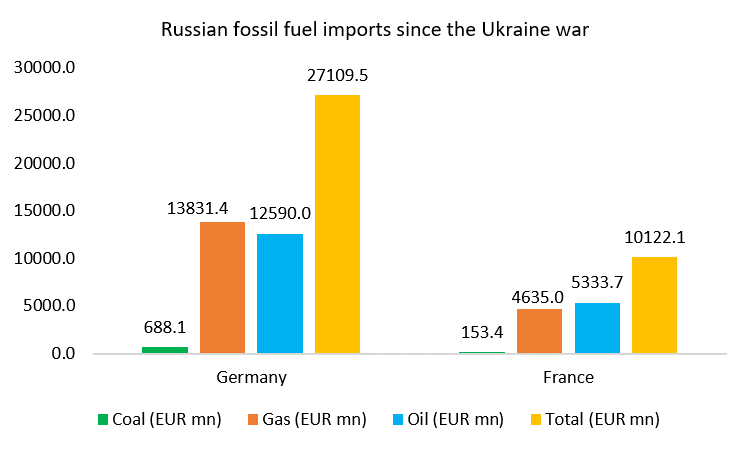

Germany, Europe’s largest economy has maintained an assertive stance against Russia, since the outbreak of the Ukraine war, even committing two battalions of battle tanks to the war effort, earlier this year.

The Russia Fossil Tracker data shows that since the outbreak of the war, it has been the number one importer of Russian energy products into the EU, and was larger than Spain, Austria, Bulgaria and the Czech Republic combined.

However, this has changed drastically with the country not appearing in the top-20 list (including the EU as a bloc) for 2023, after committing to diversifying energy sources by re-opening coal plants, keeping nuclear reactors operational and inking new energy agreements with the USA and Norway.

For his part, President Macron of France had professed wanting to de-escalate tensions between Ukraine and Russia, and even met with Vladimir Putin earlier this year.

However, France, which was the fourth largest importer since the war began, did not feature in the top-20 list in 2023 either.

Any goodwill towards favouring negotiations has all but evaporated, with the French President announcing on June 1, 2023,

…we confirmed the readiness to develop the framework to start the training of Ukrainian combat aircraft pilots when appropriate for Ukrainian Air Force… we have tasked our ministers of defence to work together in order to prepare formal decision on concrete scope and the mechanism of the training of pilots and technical staff, based on the request of the Ukrainian side, to be taken at the next Ramstein meeting with all nations part of the fighter pilots’ training initiative.

Although important trade partners, Poland and Russia have long maintained frosty relations, with the Kremlin threatening retaliation against Warsaw as recently as May 2023, for occupying a Russian school in the city and forcibly ousting teachers and other employees.

In 2022, a Pew poll showed that 94% of Poles surveyed viewed Russia as a ‘major threat.’

A Baltic research study published by LSE IDEAS at the London School of Economics and Political Science in December 2022, noted,

Estonia has maintained a hard stance against Russian aggression despite its own internal political issues…. (Latvia’s) parliamentary elections in October 2022 reflected a major shift away from pro-Russian sentiment… In May (2022), the Lithuanian Parliament recognised the war in Ukraine as a genocide and classified Russia as a terrorist state.

Of the three countries, Lithuania was, by far, the most dependent on Russian energy, with the IEA estimating its reliance as high as 166.1% in 2013 which steadily fell to 97.5% in 2021.

However, the LSE paper also notes a radical transformation in the country’s energy security, adding,

Lithuania made the strategic decision to build a modern LNG terminal as an alternative natural gas supply source, beginning operation in 2015. Today, the LNG terminal—appropriately named Independence—can fully meet Lithuania’s gas demand, as well as supply gas to neighbouring countries, thereby freeing the country from its Russian dependence.

These reforms enabled Lithuania to completely exit Russian energy exports in 2022, while LNG was imported from the USA, and electricity was bought from partners such as Sweden, Poland and Latvia.

These measures were taken in light of the offensive on Ukraine and as trading of Russian electricity ceased on the pan-European Nord Pool power exchange.

Conclusion

As a result, Hungary, Slovakia, Bulgaria, the Czech Republic, Spain, Belgium, and Belarus would likely support, to varying degrees, closer economic ties with Russia.

However, they each are reducing dependence on Russian energy, which suggests that any support may be relatively short-lived, other than in the case of close historic allies such as Belarus.

Having said that, even Belarus is looking to reduce Russian supplies from 90% of total energy imports to 70% by 2035.

On the other hand, the main powerhouses of Europe, such as Germany and France, as well as other countries such as Poland and the Baltic states are likely to oppose such a move.

This may ultimately have a direct bearing on the mechanism itself, as it may require approval from European regulators to become functional in the first place.

Since such a mechanism would be seen as going against the tide of sanctions, Italy would likely be in favour of pushing this instrument through as soon as possible.

At the same time, even countries that support the initiative may find it convenient if the discussion process is delayed, to buy time and further reduce their dependence on Russia over the next couple of years, rather than being forced to select sides in a slippery geopolitical situation.

The post Can Italy revive ailing economy with Russian rubles? appeared first on Invezz.

dollar

inflation

commodities

monetary

markets

policy

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…