Economics

Bank of America’s Guide How To Talk To Your Family About The Economy Over The Holidays

Bank of America’s Guide How To Talk To Your Family About The Economy Over The Holidays

By Bank of America chief global economist, Aditya Bhave

We’ve…

Bank of America’s Guide How To Talk To Your Family About The Economy Over The Holidays

By Bank of America chief global economist, Aditya Bhave

We’ve all been there. You work in finance, so inevitably someone will approach you at a holiday gathering and ask you about the economy. But we’ve got your back. In this report, we list 10 questions you might get asked. For each question, we suggest both a short response – in case dessert is served or you just don’t want to talk shop – and a more detailed response – if you really want to engage in the conversation. As a disclaimer, these are the views of BofA Global Research’s US Economics team. Others might answer these questions differently, but that would only liven up the discussion!

1. “Are we in a recession? Didn’t we have two consecutive quarters of negative GDP growth this year?”

Short answer: Not yet.

Longer answer: We had two consecutive quarters of negative GDP growth in 1Q and 2Q 2022. This amounts to what’s known as a “technical recession”. But the National Bureau of Economic Research (NBER) makes the “official” call on whether we are in a recession. The NBER looks at several economic indicators, not just GDP. A few of those indicators are related to the labor market (job creation and wage growth), so it’s unlikely that we will enter an NBER-defined recession until the labor market cracks. At the moment the labor market is still very hot, due to both strong demand for workers and labor supply shortages.

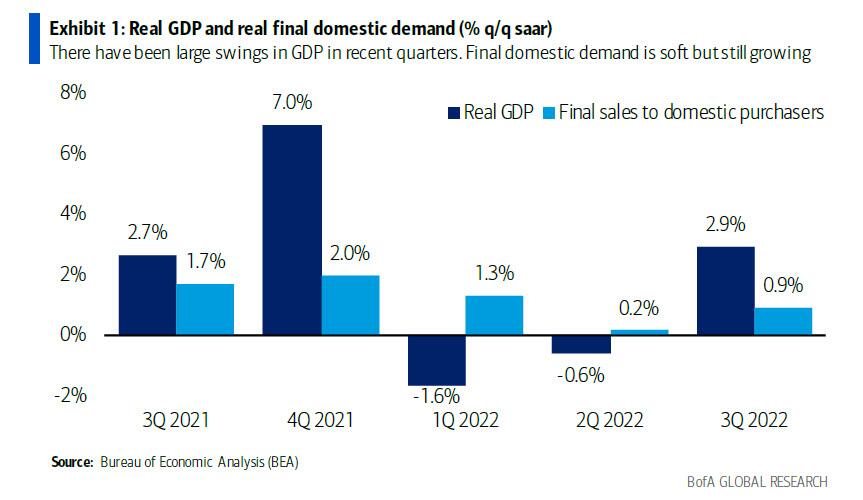

Technical recessions typically overlap with NBER-defined recessions. This time is different because GDP has been distorted by large swings in the trade and inventory data. Once we exclude these components, we see that final domestic demand (i.e., consumer spending, residential and business investment, and government spending), is weak, but is still growing (Exhibit 1).

* * *

2. “So when will the next recession start?”

Short answer: Probably next year.

Longer answer: The tipping point for a recession should be when the labor market slows materially. Consumer spending has been relatively resilient so far. If the labor market breaks, not only will the NBER’s recession criteria likely get triggered, but consumer spending will also probably weaken significantly. Since the consumer is nearly 70% of the economy, that would drive domestic demand lower. We will probably go into a mild recession next year.

The labor market is likely to weaken next year for a few reasons. First, hiring has outpaced GDP growth by a long way this year. Payrolls have grown by over 2.5%, while real GDP growth has been less than 1%. This is not sustainable. Second, higher rates (due to Fed hikes) are hurting business and residential investment. The housing market is already in a recession and the manufacturing sector appears to be following suit. This should eventually translate into job losses. Third, the Fed hiked rates by 425bp this year and Fed hikes affect the economy with “long and variable lags”. So a lot of the economic and labor market damage from this year’s Fed tightening probably hasn’t happened yet.

* * *

3. “This feels like the most widely anticipated recession that I can remember. Is there a chance that we could talk ourselves into a recession?”

Short answer: Yes and no.

Longer answer: There is some truth to the idea that recessions can be self-fulfilling prophecies. If businesses expect weaker consumer demand, they might stop investing and start laying off workers. Similarly, consumers might pull back on spending if they are concerned about an economic slowdown. Such precautionary behavior would likely create the recession that everyone was worried about.

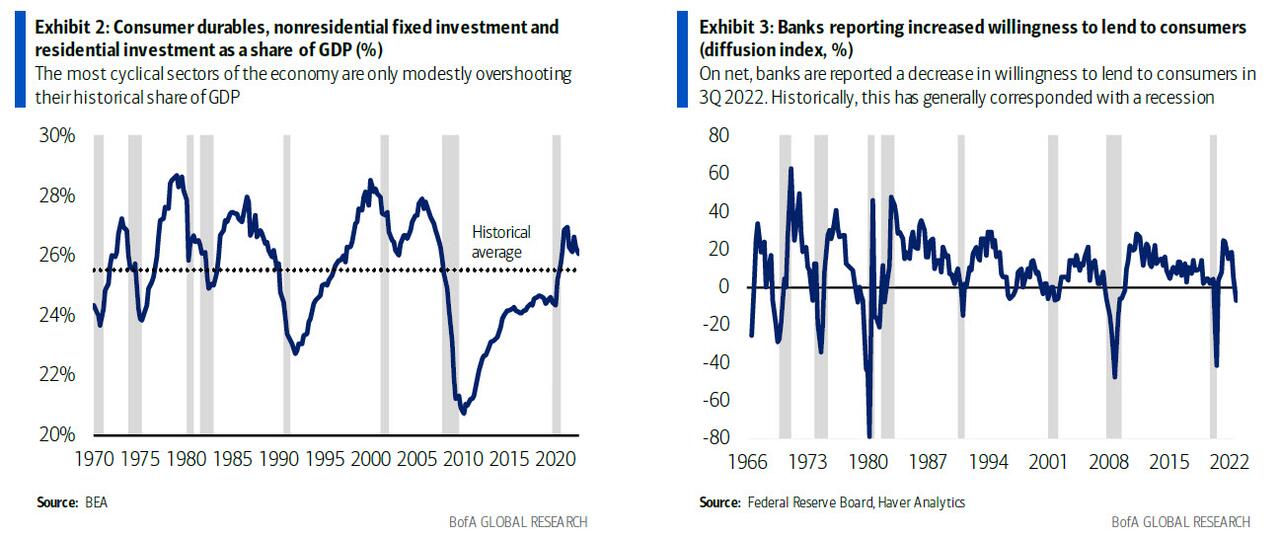

But it isn’t as simple as that. Painful recessions are generally due to the build-up of excesses in the economy. If consumers and businesses start to become cautious before such excesses build, that could limit the scope of any potential downturn. The three sectors in the economy in which these excesses usually build are consumer durables, residential investment and business investment. Currently there only modest signs of excess in these sectors (Exhibit 2). Yet banks have already started to become less willing to lend to consumers (Exhibit 3). So perhaps the recession has been so well telegraphed that it turns out to be self-inhibiting rather than self-fulfilling.

* * *

4. “You said the housing market is in a recession. Are we headed for a housing crisis?”

Short answer: Probably not.

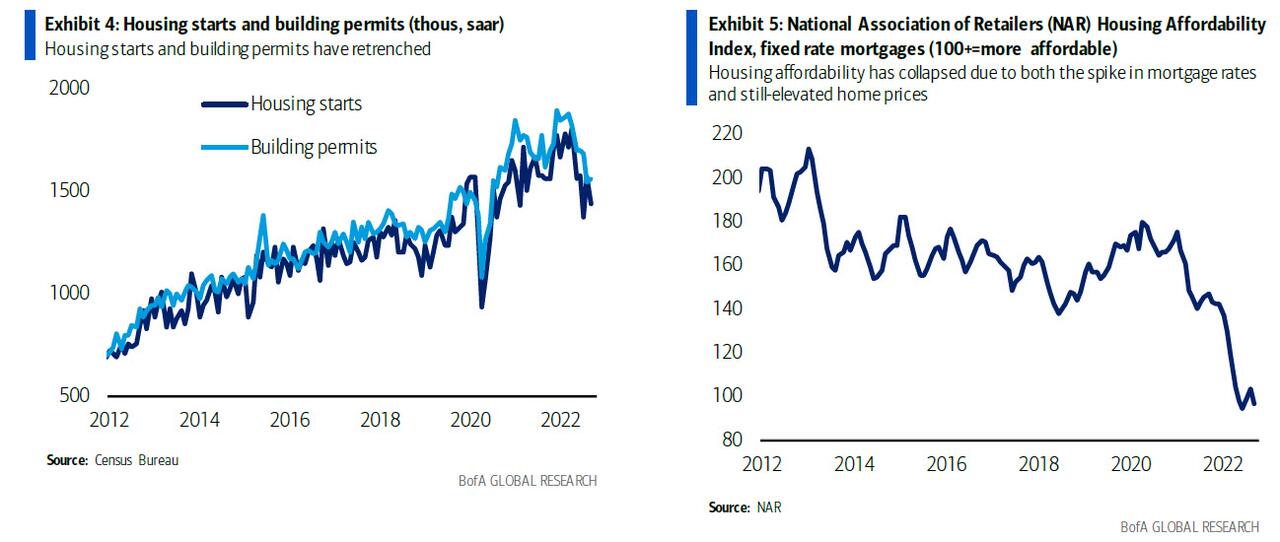

Longer answer: Housing is arguably the most rates-sensitive sector of the economy. Therefore it is no surprise that very aggressive Fed hikes have pushed the housing market into recession (Exhibit 4). After all, the 30-year mortgage rate increased from around 3% at the start of last year to more than 7% briefly, and is still well north of 6%. Tight supply – of construction labor, materials, etc. – has further hindered housing activity, although it has helped support prices (Exhibit 5).

However, this doesn’t mean we are headed for a crisis. Slowdowns in specific sectors turn into economy-wide crises when there are conditions in place that amplify their impact. In the run-up to the financial crisis, speculation (rather than fundamentals) played a big role in the demand for housing, adjustable-rate mortgages were more common, lending standards were loose and households were levering up their home equity using home equity lines of credit (HELOCs).

In the post-pandemic housing boom, demand was driven by a big generation of millennials moving into larger spaces, a very large majority of mortgages were locked in at fixed rates (so people who already have mortgages will generally not be hurt by Fed hikes), lending standards were relatively tight and there was limited use of HELOCs. Moreover, regulators are much more vigilant about the risks of a housing crisis. At the start of the pandemic there was significant forbearance for borrowers. This is likely to repeat if there is growing risk of a crisis, in order to prevent fire sales. All of this suggests that another housing crisis is unlikely.

5. “You don’t sound overly concerned about the economy. Is there a chance we’ll avoid a recession entirely next year?”

Short answer: There’s always a chance, but we’re likely to have at least a mild recession.

Longer answer: We won’t get a recession until the labor market weakens materially. Job growth has been resilient of late. We probably added around 4mn jobs in 2022, and over 800k in the last three months. To put that in context, we need to create just 50-100k jobs per month to match the growth rate of the population. This means it’s quite possible that the economy could avoid a recession in the first half of 2023.

However, it will be harder to avoid a recession for the full year. Here’s the issue. As long as the labor market remains hot, there is a risk that job growth and higher wages will create more inflation down the line. So the Fed would likely respond by raising rates even higher, which would inflict even more pain on the economy later next year. In other words, a delayed recession might mean a deeper one. We need to be careful what we wish for.

* * *

6. “You make it sound like the Fed is determined to break the labor market. What’s so special about 2% inflation anyway? Wouldn’t it be better to accept higher inflation than cause a recession?”

Short answer: There is nothing special about 2%. But abandoning the target now would put the Fed on a slippery slope. Unfortunately, the only way to get and keep inflation under control is to materially weaken the labor market.

Longer answer: In general, low but positive inflation is considered best for economic growth. Why? On the one hand, outright deflation causes consumers to delay purchases in anticipation of lower prices. As we have seen in Japan, this damages growth prospects. On the other hand, high single-digit or double-digit inflation is problematic because it tends to also be more volatile, creating uncertainty, which in turn slows spending and investment. Central banks across developed markets settled on 2% because it is a low rate of inflation that still gives them a sizeable buffer from deflation.

This is the first time the Fed’s commitment to taming inflation has been seriously tested in about four decades. If the Fed were to change its inflation target to say 4%, it would be on a slippery slope (Global Economic Weekly: What is so special about 2%?). If 4% is acceptable, why not 6% or 8%? So the target would lose credibility in the eyes of investors. But it’s possible that if inflation gets stuck a little bit above target (say 3%), the Fed would accept a longer time frame to get back to 2% instead of inflicting a lot of economic pain to get there sooner.

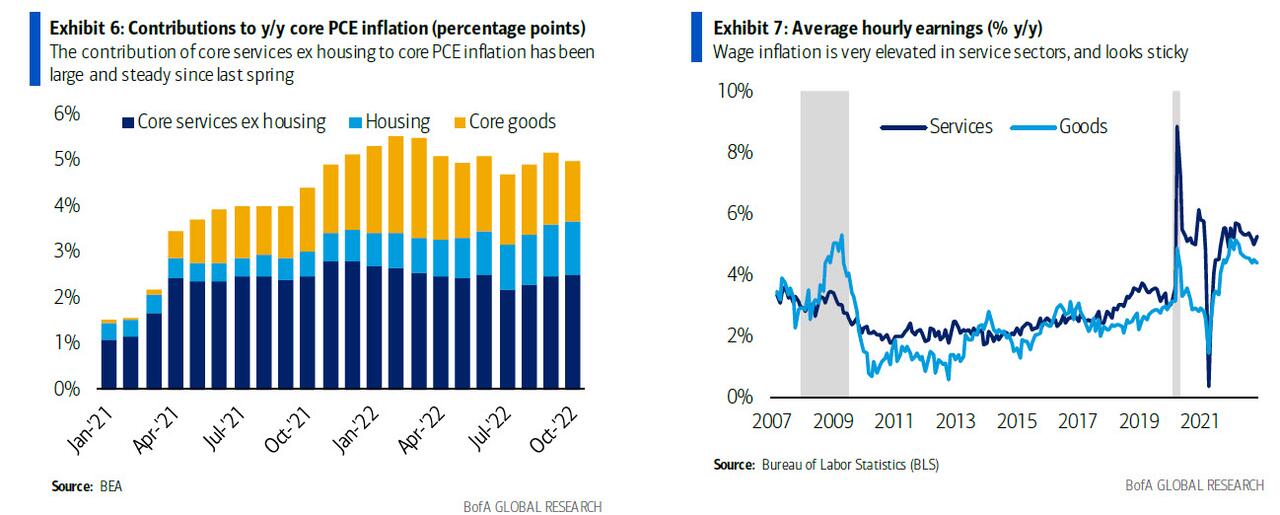

The Fed generally looks at core inflation, i.e. inflation ex of food and energy, because food and energy prices tend to be more volatile and driven by factors outside the Fed’s control (such as the Russia-Ukraine conflict). In a recent speech, Fed Chair Powell noted that services besides housing make up more than half of the core consumer spending basket (Exhibit 6). These services are labor-intensive and are seeing rapid job and wage growth as consumers return to pre-pandemic spending habits. Higher labor costs are pushing up prices (Exhibit 7). Therefore the only way for the Fed to bring core inflation back to 2% in a manner that is sustainable over time is to weaken the labor market.

* * *

7. “But inflation is already getting better, right?”

Short answer: Yes, but it might not last.

Longer answer: Goods prices spiked in the spring of 2021 because of supply-chain disruptions and huge demand for stay-at-home goods from US consumers who were awash with cash. At the time, the ARPA (American Rescue Plan Act) had just been implemented. It was the last of three big stimulus packages, the others being the CARES (Coronavirus Aid, Relief, and Economic Security) Act and the CAA (Consolidated Appropriations Act) of 2020. Now supply issues have largely been sorted out and goods demand is slowing. So goods prices have started to fall. That’s helping to slow overall inflation, but the faster goods prices correct, the sooner they will stop correcting.

The US economy is predominantly a services economy. And as we discussed earlier, the only way to bring services inflation under control is to slow the labor market down. Unless that happens, the risk is that overall inflation will pick up again once goods prices stop falling.

* * *

8. “How are US consumers dealing with higher inflation, particularly in necessities such as food and energy?”

Short answer: Inflation is painful, but a strong labor market and pandemic-era stimulus have helped the consumer to remain resilient.

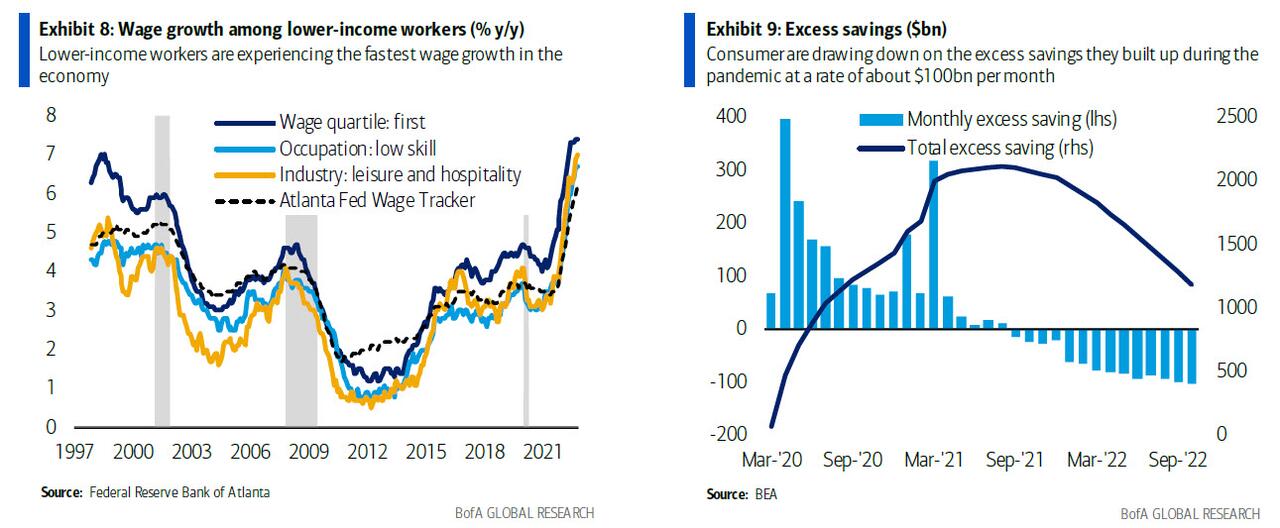

Longer answer: For the US consumer, there is an ongoing tug-of-war between inflation and labor market gains. Food and energy inflation has been particularly challenging for lower-income households, who spend a larger share of their income on necessities. But they are also experiencing strong job growth and the fastest wage inflation in the economy (Exhibit 8). This is offsetting some of the pain from inflation and allowing consumer spending to remain relatively resilient.

The US consumer is also still being propped up by excess savings from the pandemic-era fiscal stimulus packages. Consumers still probably have more than $1 trillion in excess savings, which they are drawing down at a rate of about $100bn per month, partially in response to the inflation shock (Exhibit 9). So these savings could be a tailwind to consumer spending for a few more quarters.

* * *

9. “I read that US consumers have racked up nearly $1trillion in credit card debt. How concerning is this?”

Short answer: It isn’t very concerning yet.

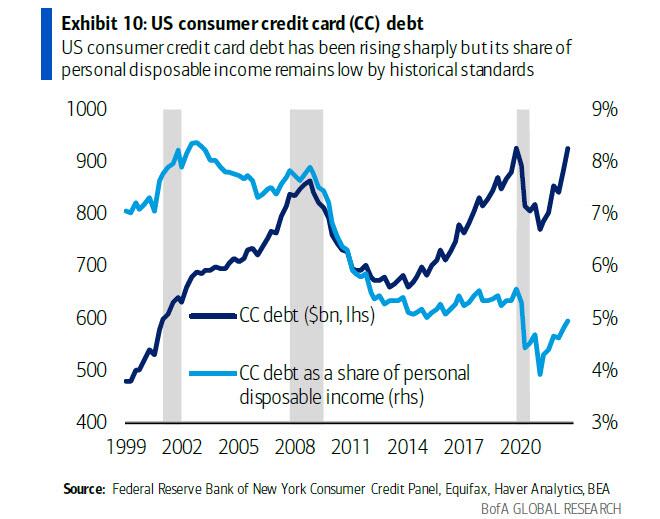

Longer answer: Credit card debt has increased from less than $800bn at the start of last year to $925bn as of 3Q 2022. This is a sharp increase that certainly bears watching. It is probably being driven by both liquidity constraints for consumers and increasing interest rates. The level of credit card debt is close to the all-time high, reached just before the pandemic.

But it is important to remember that what matters with debt is consumers’ capacity to service it. Income has also been growing rapidly, and that helps a lot. Credit card debt was less than 5% of disposable income in 3Q 2022 (Exhibit 10). This is lower than at any time before the pandemic (the data go back to 1999). The trend is similar with credit card delinquencies: they are on the rise, but they are still below pre-pandemic levels.

* * *

10. “Are consumers spending as generously over the holidays as they did last year? Also, could you please pass the cranberry sauce?”

[First pass the cranberry sauce]

Short answer: No, but that isn’t a big surprise.

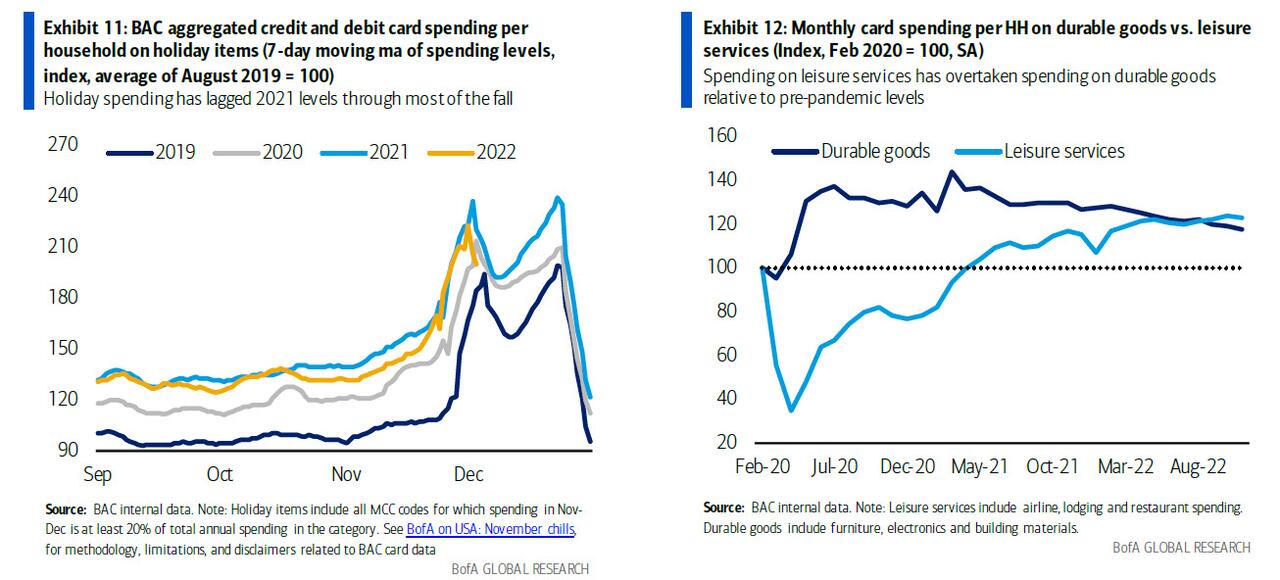

Longer answer: The holiday shopping season is obviously very important for the US consumer. Last year’s shopping season was historic, so it isn’t a huge surprise that we’re tracking weaker spending on holiday goods this year (Exhibit 11). Another factor weighing on the dollar value of holiday spending this year is that discounts have potentially been deeper and more back-loaded than last year. So we really need to adjust for inflation/deflation and wait until the end of the holiday season to get a full picture of holiday spending.

Finally, consumers are rotating back to services from goods as the impact of the pandemic fades (Exhibit 12). Last year, consumption of services during the holidays was disrupted by the omicron variant outbreak. People responded by spending more on holiday presents. This year, they are probably traveling more, dining out more and attending shows, concerts, sports events, etc.

Tyler Durden

Sun, 12/25/2022 – 17:30

dollar

inflation

deflation

markets

interest rates

fed

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…