Economics

A bipolar world of stock market performances

US benchmark stock indices continue to maintain global leadership as its cyclical laggards are now playing catch up to the technology-related Magnificent…

- US benchmark stock indices continue to maintain global leadership as its cyclical laggards are now playing catch up to the technology-related Magnificent Seven (Apple, Microsoft, Meta, Nvidia, Telsa, Alphabet & Amazon).

- The laggard Dow Jones Industrial Average staged a bullish breakout from a 7-month range consolidation supported by strong performances in financials/banking stocks.

- China’s latest “New Consumption Plan” has failed to spark bullish sentiment in China and Hong Kong benchmark stock indices.

- Another round of yuan weakness may increase the risk of a deflationary spiral in China.

Bullish rotation into the laggards of the US stock market

Fig 1: Dow Jones Industrial Average medium-term trend as of 19 Jul 2023 (Source: TradingView, click to enlarge chart)

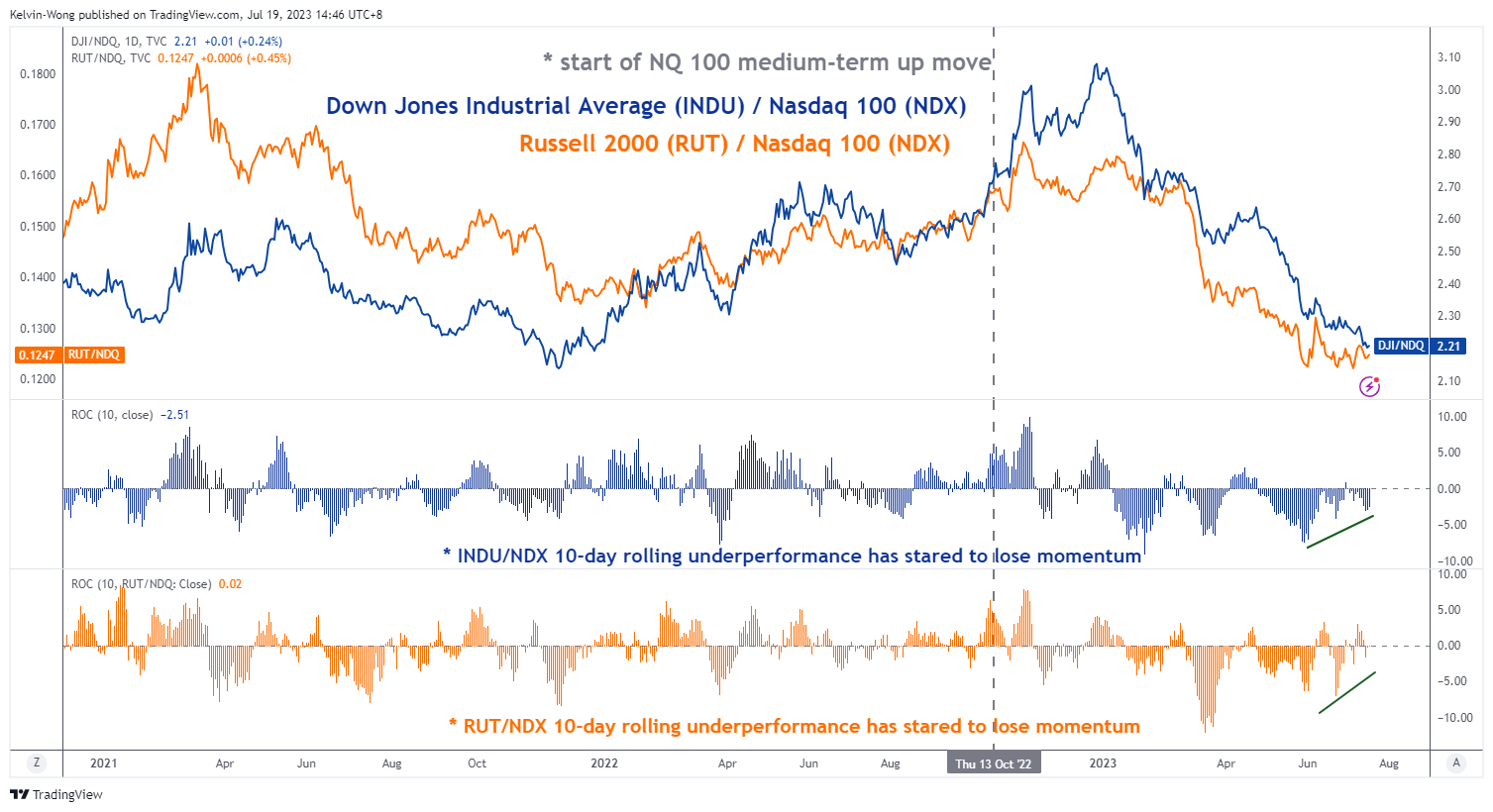

Fig 2: Dow Jones Industrial Average & Russell 2000 relative momentum against Nasdaq 100 as of 19 Jul 2023

(Source: TradingView, click to enlarge chart)

The Dow Jones Industrial Average (INDU) has sparkled back to a bullish tone after it lagged other major US benchmark stock indices such as the Nasdaq 100 and S&P 500 since the start of the ongoing medium-term uptrend phase in place since late October 2022 based on the S&P 500.

At the end of last week, 14 July, the DJIA just notched a meagre 2023 year-to-date return of 4%, around ten times below the top performer, Nasdaq 100 with a gain of 42% and S&P 500 ‘s return of 17% over the same period.

The underperformance of the INDU has been primarily due to a higher combined weightage of its constituents that are concentrated in the financials, banks, and industrials sectors (cyclical stocks) that lagged the information technology sector that commanded a “safe haven” premium after the onset of the US regional banks’ turmoil in mid-March and the rising optimism in generating longer-term productivity gains from Artificial Intelligence (AI).

Yesterday’s better-than-expected Q2 earnings results from two US major banks; Bank of America and Morgan Stanley shrugged off fears of a potential second round of banking crisis due to the US central bank, Fed’s current hawkish rhetoric; “higher interest rates for a longer period”.

Overall, these rosy set of earning results triggered a positive feedback loop into the share prices of other banking/financial stocks that allowed the SPDR S&P Banking exchange-traded fund to rally+3.5% yesterday, 18 July. In turn, the INDU gained by 1.06% and outperformed the high-flying Nasdaq 100 (+0.82%).

Also, yesterday’s positive momentum in the INDU has allowed its price actions to stage a bullish breakout from a seven-month range configuration and closed at a 15-month high of 34,951. From a technical analysis and momentum factor standpoint, these observations are considered positive “significant milestones” that may see further potential gains in the INDU in the coming weeks.

A different story in Asia, spooked by China’s deflationary scare

Yesterday, China policymakers released a “New Consumption Plan” to be implemented jointly by 13 government departments to boost and rejuvenate retail spending after retail sales for June came in worse than expected. The coverage of the consumption plan has so far highlighted only the optics; better access to credit to purchase household products, expand the availability of home-related products to rural areas, and provide cheap renovation services but lacks the details such as the monetary value of these support measures.

The net effect from a behavioural standpoint is bearish sentiment prevails in the short-term for the broad-based China benchmark stock indices and its proxies, the Hang Seng indices. The CSI 300 had shed by -1.5% week-to-date at this time of the writing. The Hang Seng Index, Hang Seng Tech Index, and the Hang Seng China Enterprises Index fared much worst as these indices tumbled by around -3% week-to-date.

Yuan weakness is on the rise again

Fig 3: USD/CNH medium-term trend as of 19 Jul 2023 (Source: TradingView, click to enlarge chart)

One of the major catalysts that led to the current weak performances of China-related equities is the revival of the bullish tone seen in the USD/CNH (offshore yuan) despite the stronger-than-expected opening fixing reference level for the onshore yuan (CNY) against the US dollar today by China central bank, PBoC; 7.1486 versus consensus of 7.1798 per US dollar.

Last week’s decline of the USD/CNH has managed to find support at the upward-sloping 50-day moving average at 7.1200 supported by a positive momentum reading seen in the daily RSI oscillator. In addition, the 2-year yield premium of the US Treasury over the China sovereign bond managed to tick higher since last Thursday, 13 July which reinforces further potential yuan weakness.

A clearance above 7.2160 (also the 20-day moving average) may add further impetus for USD/CNH to see the next key resistance at 7.3450 which in turn may spark further weakness in China-related equities.

Also, further yuan weakness is likely to put more financial burden on the current offshore bonds payment obligations of Chinese property developers where the property industry still faces a credit crunch issue due to a weak internal demand environment.

Brewing financial stress of major Chinese property developers is on the rise again, prices of their onshore dollar bonds tumbled significantly in the last two days; in light of a trading halt announcement made by Sino-Ocean Group in a local note that is due to mature in two weeks, and Dalian Wanda Group issued a warning to its creditors of a funding shortfall for a bond that is due for redemption on 23 July.

Hence, the failure to negate the current negative sentiment in the China stock market may further reinforce a negative feedback loop into the real economy which in turn increases the risk of a deflationary spiral.

dollar

monetary

interest rates

fed

central bank

us dollar

deflationary

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…