Base Metals

With few projects in industry pipeline, Copper Road’s exploration story is a must-follow – Richard Mills

2023.07.24

Simply put, the road to reaching net zero begins and ends with copper. All infrastructure built to support renewable energy uses large amounts…

2023.07.24

Simply put, the road to reaching net zero begins and ends with copper. All infrastructure built to support renewable energy uses large amounts of copper, as the metal is a highly efficient conductor of electricity and heat.

To keep the energy transition going, millions of feet of copper wiring will be required for strengthening the world’s power grids, and hundreds of thousands of tonnes more are needed to build wind and solar farms. An offshore wind turbine, for example, contains 8 tonnes of copper per megawatt of generation capacity.

Electric vehicles, now a fast-rising source of demand, use over twice as much copper as gasoline-powered cars, which contain about 30 kg. Not to mention, there is more than 180 kg of copper in the average home, reminding us just how indispensable the metal really is.

Adding it all up, demand for copper is going to be staggering as we look ahead into the future.

Copper Supply Gap

According to McKinsey, global electrification is expected to increase annual copper demand to 36.6 million tonnes by 2031, compared to the current demand of roughly 25 million tonnes. However, the consultancy firm forecasts copper supply to be around 30.1 million tonnes, leaving a gap of 6.5 million tonnes by the start of next decade.

Green uses of copper accounted for 4% of copper consumption in 2020, but this is expected to rise to 17% by 2030, Aditi Rai, an analyst at Goldman Sachs, wrote in a note. He added a “net-zero emissions” path would mean the world would need an additional 54% of copper by 2030 on top of that forecast.

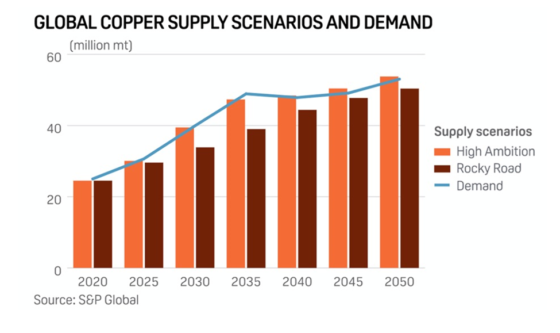

S&P Global Market Intelligence goes a bit further out, projecting that annual global copper demand will nearly double to 50 million tonnes by 2035. Last year, global copper mine production sat at approximately 22 million tonnes, short of even the current demand.

“Assuming mining output continues to grow at a rate of 2.69% annually (as it has done for the past decade), global output will reach a mere 31 million tonnes, a far cry from the 50 million figure that we’d need as previously mentioned,” S&P said.

“The challenge is that if current trends continue … there’s a huge gap,” said S&P Global vice chair Daniel Yergin upon the release of the copper analysis. “And even if you put on your roller skates and your jet burner [to realize optimistic supply growth], and everything goes right, there’s still a gap, because it’s enormous. And it’s important to recognize that now, not in 2035.”

“The market overall is pretty tight,” Robert Edwards, copper analyst at CRU, mentioned in a recent Wall Street Journal piece. “Longer term there’s a narrative around resource scarcity and the green transition with EVs and renewables as well as the build-out of electricity grids. On paper it’s quite a substantial supply gap opening up over the next 10 years.

All of this means one thing — that the global copper market is entering an age of deficits so large that it could derail our climate goals.

Some of the world’s largest mining companies and metal traders are warning the shortfall could arrive as early as 2025.

The International Copper Study Group (ICSG) says the copper market is facing another year of deficits. The group’s April forecast, via Reuters, calls for a supply shortfall of 114,000 tonnes in 2023, compared to a 431,000-tonne deficit in 2022.

When ICSG last met in October, it was expecting global mine production to grow by 3.9% in 2022 and 5.3% this year. It now thinks growth was 3% last year, and revised its forecast down to 3% in 2023.

The Reuters story says the expected wave of new supply from four new mines — the DRC’s Kamoa-Kakula, Quellaveco in Peru, along with Quebrada Blanca II and Spence-SGO in Chile – is being offset by multiple hits to existing operations:

The ICSG cites as reason for its lowered mine growth expectations “operational and geotechnical issues, equipment failure, adverse weather, landslides, revised company guidance in a few countries and community actions in Peru”.

Supply Prone to Disruptions

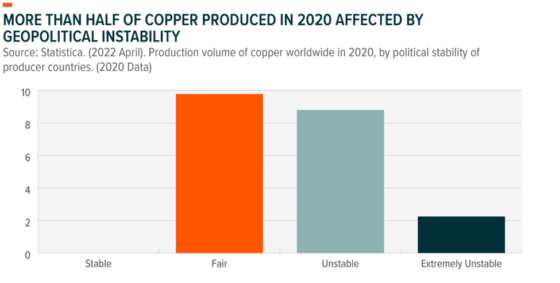

Geopolitics is seen by S&P as a major contributing factor to the shortfall in global copper supply. Of the 20 million tonnes of copper produced in 2020, more than half were from nations categorized as “Unstable” or “Extremely Unstable” (see below).

Since late 2022, Peru, the second-largest producer, has been rocked by political turmoil. The nation has experienced daily rioting, meaning supply chains across the country have been crunched. In January, experts estimated roughly 30% of Peru’s production was at risk

Multiple world-leading mines such as Glencore’s Antapaccay and MMG’s Las Bamba – combining for 2.5% of global copper output, were either shut down or restricted by protestor roadblocks.

Perhaps no country serves a better example of how vulnerable the copper supply chain is than Chile.

As the world’s No.1 producer, Chile’s output has stagnated due to deteriorating ore quality and water restrictions in the arid north. Permitting is also getting tougher.

Research firm Fitch Solutions estimates 2023 copper production in the world’s top producer will be about 5.7Mt, the same as in 2020.

In 2021, leftist candidate Gabriel Boric was elected president of Chile, on a mandate to impose higher taxes, sending a chill through the mining industry which argued the change would impede competitiveness.

Constitutional reform was also on the agenda. Since then, cooler heads have prevailed. A proposed new constitution was rejected by voters last September, while an ambitious tax overhaul plan was voted down by Congress in March.

A government plan for new royalties on mining, which is currently moving through Congress, has been tempered to 46%.

Large mining companies are watching these developments closely. BHP, majority owner of the world’s biggest copper mine Escondida, wants the Chilean government to make further concessions on the tax legislation before investing an estimated $10 billion in the country.

Necessary to Diversify Supply

In the background, though, mining companies are determined to diversify away from high-risk jurisdictions like Chile and Peru, which is why aggressive deals are being made on high-quality copper assets elsewhere.

BHP, for example, went to acquire fellow Australian miner OZ Minerals last year, a move that would boost its copper production by about 7%. Swiss commodities giant Glencore is also seeking to flex its financial muscles, offering $23 billion for Canada’s Teck Resources to create what would be the third-largest copper producer in the world.

Rio Tinto, the leading producer of iron ore, also made significant forays into copper by completing its $3.3 billion acquisition of Turquoise Hill and giving the company a 66% stake in Mongolia’s Oyu Tolgoi, one of the world’s largest known copper deposits.

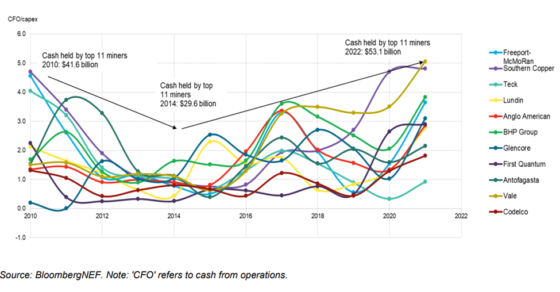

Analysts at BloombergNEF are expecting more consolidation in the near term to boost supply and lower costs. Copper miners have the cash to fund mergers and acquisitions, with BNEF analysis indicating the top 11 miners are sitting on $53 billion of cash and cash equivalents — the highest level in a decade.

But making deals only goes as far as maximizing the output of existing copper operations.

The problem, as identified by Reuters metals columnist Andy Home, is that there is precious little copper supply in the pipeline beyond the four aforementioned mines currently being brought online.

This is what Glencore’s CEO Gary Nagle said in late 2022: “Whatever was planned to be built has been built. There is nothing coming behind [the projects now ramping up into production].”

The commodity trader’s outlook on copper supply is way more pessimistic than, say, McKinsey’s. The firm says if the world is going to meet its zero emissions targets, it will be short 50 million tonnes of copper by 2030.

Clearly, the world needs new copper mines, but they can’t be built and commissioned that fast. In North America, 20 years can elapse between initial discovery and first production. We’ve got less than seven years.

Sam Crittenden, an analyst with RBC Dominion Securities, recently estimated that the energy transition’s copper requirements will mean an additional 1% of copper supply, the equivalent of one large copper mine (a la Escondida) coming online every year.

Quality shovel ready projects are scarce and getting more difficult to build: When we look at the list of available copper projects it’s notable that there is a lot of copper out there but a lot of it may never come out of the ground,” Crittenden said.

A report this week from the Energy Transitions Commission further reinforces the idea that there has been a severe lack of investment leading to new copper discoveries. “Annual capital investment in energy transition metals averaged $45 billion over the last two decades compared with the $70 billion needed each year through to 2030 to expand supply,” the ETC said.

Clearly, to stand a chance of hitting our climate change targets, more copper mines must be built from scratch. This begins identifying exploration projects with such potential, but absent the risks posed by countries like Chile.

Copper Road Resources

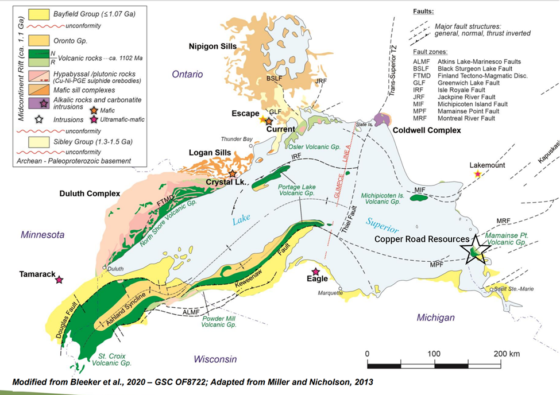

One place the industry has to look to is the Canadian province of Ontario. Often placed amongst the top 10 jurisdictions in the world for mineral exploration, it currently has 35 active mines.

Behind its wealth of minerals is the geological advantage offered by the Mid-Continental Rift, which curves for more than 2,000 km across North America and is one of the world’s great continental rifts. Also called the “Keweenawan Rift”, it stretches across Lake Superior near Marathon, ON, all the way across Minnesota, Michigan, Wisconsin, Iowa, Nebraska and Kansas.

The Mid-Continental Rift is the same structure that formed Lake Superior and the world-class Keweenawan peninsula copper-mining region in the US, which housed the initial copper rush in the mid-1800s and was mined for more than 150 years.

Today, there are only a few copper developments on the Ontario side of the Keweenaw, providing an immense opportunity for exploration companies to make their mark on the industry, with Copper Road Resources Inc. (TSXV: CRD) amongst the most active.

The company’s namesake property covers 21,000 hectares within the Batchewana Bay district, about 85 km north of Sault St. Marie.

The property package has a proven history of copper production, containing two former mines: The Tribag mine, which produced 1.2 million tonnes grading 1.52% Cu, and the Coppercorp mine, with historic production of 1 million tonnes at 1.16% Cu.

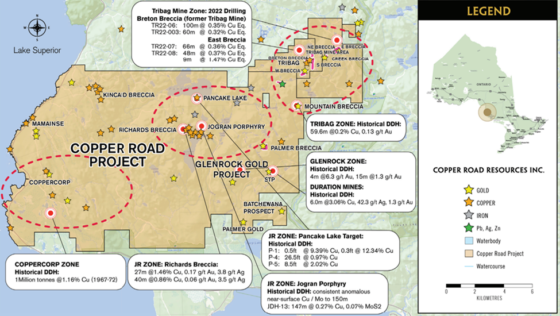

There are several confirmed zones of mineralization within property boundaries — Tribag, Glenrock, JR (Richards/Jogran) and Coppercorp — each hosting multiple targets for exploration. Together, they span a total length of 30 km.

The company is currently focused on two zones of known near-surface mineralization at Tribag and JR, which are approximately 12 km apart.

The former Tribag mine represents a porphyry-style copper deposit, consisting of four breccias (Breton, West, East, South). Its reported historical production (1967-1974) was predominantly from the Breton breccia.

Historical estimates by Teck Resources, its former operator (1966-1972) and a household name in the Canadian mining industry, identified 40 million tonnes at 0.4% copper from the Breton breccia, and estimated 125 million tonnes at 0.13% copper and 0.05% molybdenum from the East breccia.

Last year, Copper Road completed 3,000 m of drilling at the Tribag mine zone, with all eight holes returning significant intervals of near-surface mineralization (i.e. 9m at 1.47% copper equivalent), proving the continuity, depth, and additional mineralization outside of historical models at the Breton breccia.

The JR zone consists of the Richards breccia, a near-surface copper target, and the Jogran surface porphyry, which has been drilled to a depth of 200 m. The two targets are located 900 m apart.

Due to fragmented claim ownership and regional staking closures, the JR zone has only seen limited diamond drilling into these near-surface porphyry and breccia-hosted Cu-Mo-Au-Ag targets.

Historical exploration by Jogran Mines (1964), Phelps Dodge (1966), Duration Mines (1988), and Aurogin Resources (1997) encountered relatively broad near-surface intersections of copper mineralization that is still untested below 150 m in the porphyry, and below 75 m in the breccia.

Last month, Copper Road identified the priority targets at JR for its upcoming drill program, which will test the Jogran porphyry at depth, the extension of the historic high-grade intercepts in the Richards breccia, and another area of mid-grade copper mineralization.

“We are confident that our proposed summer exploration program will demonstrate the potential of the JR Zone to host a large-tonnage near-surface copper deposit containing a suite of by-product minerals,” Copper Road Resources CEO John Timmons commented in a news release.

Conclusion

Currently offering a private placement for gross proceeds up to $400,000, Copper Road Resources is in a great position to accomplish its 2023 exploration goals.

Its progress is also gaining some traction within the investment community. Within a span of two months, the company’s stock rebounded from a low of 5.5 cents a share in May to almost doubling, a show of confidence not only in the company but also where the market for copper junior miners is at.

“We now see some projects coming online in Peru and in Chile, which will add incremental supply, but there is not a lot in terms of pipeline in terms of long run,” Barbara Mattos, an analyst at ratings company Moody’s Investors Service, told WSJ, referring to the general lack of investment in mining projects over the past couple of decades.

As CEO Timmins noted in a May interview with RocksAndStocksNews, there’s not enough supply to meet a projected $2 trillion upgrade that America needs to reach net zero. For a lot of the current mine projects like the Escondida expansion, “the offtake agreements are already in place … but new projects coming online are scarce.”

In fact, he says that high-level fund managers with hundreds of millions of dollars are having a tough time finding good projects to invest in.

Now that the majors are starting to spend their cash, it makes copper explorers sitting on large projects with past production history like CRD worth monitoring, especially in a period of high metal demand. Adding to its appeal is that there are just no new mines coming online here in North America, making its exploration story a “must-follow”.

Copper Road Resources

TSXV:CRD

Cdn$0.105, 2023.07.21

Shares Outstanding 47.3m

Market cap Cdn$4.26m

CRD website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Richard does not own shares of Copper Road Resources (TSXV:CRD). CRD is a paid advertiser on his site aheadoftheherd.com.

This article is issued on behalf of CRD

White House Prepares For “Serious Scrutiny” Of Nippon-US Steel Deal

White House Prepares For "Serious Scrutiny" Of Nippon-US Steel Deal

National Economic Adviser Lael Brainard published a statement Thursday…

How to Apply for FAFSA

Students and families will see a redesigned FAFSA this year. Here’s how to fill it out.

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…