Base Metals

Raw Steels MMI: Steel Prices Flatten, Slowly Edge Downward

The Raw Steels Monthly Metals Index (MMI) fell by 3.04% from September to October. U.S. steel prices continued to drop throughout September. However, declines…

The Raw Steels Monthly Metals Index (MMI) fell by 3.04% from September to October. U.S. steel prices continued to drop throughout September. However, declines for both hot rolled coil prices and cold rolled coil prices slowed to a sideways trend. Plate prices, which have shown the most strength of steel prices, traded down for the second consecutive month. They now sit at their lowest level since September 2021.

Steel and other commodity markets are constantly shifting. Get all of the latest updates with MetalMiner’s weekly newsletter.

U.S. Steel Idles Two Furnaces as Steel Prices Slide

As steel prices continue their slow descent, one steelmaker appears eager to cut capacity. In early September, U.S. Steel idled its 1.5 million short ton per year blast furnace with no scheduled restart date. The company attributed the decision to “high import levels and market conditions.” Most likely, this was a reference to the steep price declines among steel commodities since October 2021.

More recently, U.S. Steel announced the indefinite idling of its 1.4 million-short-ton-per-year Mon Valley blast furnace. The furnace was previously taken offline on September 3 for maintenance. Although the company initially planned to return it to production after 30 days, they later announced it would remain idle. According to a company statement, management wished to “balance our production with our order book.”

The steelmaker’s latest decisions suggest that the domestic markets continue to grapple with oversupply despite the loss of competitively priced European imports. Amid many compounding economic pressures, demand has begun to show signs of easing. Meanwhile, ongoing ramp-ups from new and expanded mills continue to inflate domestic capacity.

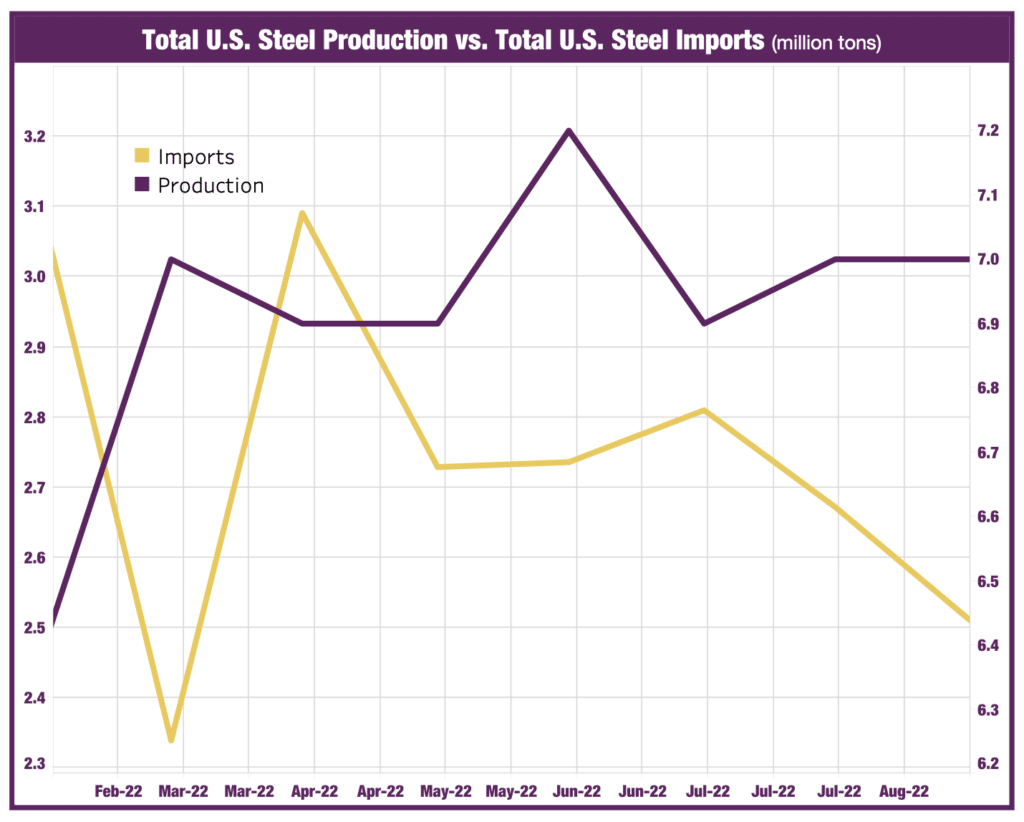

Over the past six months, steel production has enjoyed an upward trend. Imports, however, continue to decline from March highs.

MetalMiner just released it’s 2023 U.S. Cold Rolled Stainless Steel report. Get expert advice on where stainless prices are headed in 2023, as well as how much to purchase and when. Learn more and order here.

Following $120/St Drop, Nucor to Keep Plate Prices Flat

U.S. Steel is not alone in its attempts to stop the decent of steel prices. After complaints over the record-high spread between HRC and plate prices, Nucor dropped plate prices by $120/st in late July. The company also attempted (albeit unsuccessfully) to raise HRC prices by $50/st. Since that announcement, plate prices have fallen $168/st.

Following two months of declines, the steelmaker now wishes to push the plate price trend sideways again. In early Octobor, Nucor announced no change to November plate prices from its last quote of $1,620/st. That said, it’s uncertain whether the latest move will stick. It’s true that the spread between the late-April peak and current prices continues to expand. However, the overall declines thus far have been slow, with plate prices diverging from the much steeper descents of HRC, CRC, and HDG. That said, U.S. plate prices still hold a premium over their global counterparts. This means domestic market dynamics will largely determine future price direction.

Are you under pressure to generate steel cost savings? Make sure you are following these five best practices.

Europe Looks to Protect Steel Sector After Curtailments

Meanwhile, European countries have begun implementing emergency measures to mitigate rising energy prices. The steel sector is among multiple energy-intensive industries that are particularly vulnerable to the ongoing energy crisis, thus impacting steel prices. Rising input costs, on top of eroding demand, have already caused a wave of curtailments that threaten the viability of Europe’s entire metal sector.

By late September, Italy approved energy bonuses for companies. As part of the decree, operating steel producers will receive a 40% tax discount for energy spending from October through November. According to the GMK Center, scrap processors will receive a 30% discount.

Germany is particularly vulnerable due to its outsized reliance on Russian gas. The country assembled two multi-billion dollar aid packages at the beginning and end of September in hopes of bridling energy prices. The first of those packages earmarked €1.7 billion to provide tax benefits to 9,000 energy-intensive businesses.

Beginning in October, the UK established electricity price limits for British companies, which could cut wholesale prices by half. This policy will last for six months. However, scheduled governmental reviews will determine any support beyond that date (March 2023). This will continue to impact steel prices.

Many of the measures approved thus far appear limited in scope, considering the energy crisis could realistically last years. It remains uncertain how effective these efforts will be in preventing the permanent loss of European steel capacity in the long term. However, recent actions suggest that countries see protecting their industrial sectors as strategically important. This appears a stark contrast with placing the focus only on individual consumers.

European countries have thus far allocated roughly €500 billion in total to the energy crisis. This should go a long way in helping to minimize European sourcing disruptions for the capacity that remains operational.

The MetalMiner Annual Outlook consolidates our 12-month view and provides buying organizations with a complete understanding of the fundamental factors driving prices and a detailed forecast you can use when sourcing metals for 2023 — including expected average prices, support and resistance levels.

Biggest Moves for Raw Materials and Steel Prices

- Of the two components that traded up last month, standard Korean steel prices saw the largest increase. All together, the index rose 13.2% to reach $261 per metric ton by October 1st.

- Chinese coking coal prices rose 7.45% to $391 per metric ton.

- Meanwhile, Chinese slab prices declined 3.14% to $611 per metric ton.

- Chinese billet prices fell 4.99% to $525 per metric ton.

- U.S. Midwest three month HRC futures declined 5.49% to $775 per short ton.

Enjoy this article? Sign up for MetalMiner’s free Monthly Metals Index Report. Get price trends and updates for 10 different metal industries, including steel, copper and aluminum. Sign up here.

White House Prepares For “Serious Scrutiny” Of Nippon-US Steel Deal

White House Prepares For "Serious Scrutiny" Of Nippon-US Steel Deal

National Economic Adviser Lael Brainard published a statement Thursday…

How to Apply for FAFSA

Students and families will see a redesigned FAFSA this year. Here’s how to fill it out.

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…