Azarga Metals released an updated PEA on the Unkur copper-silver project

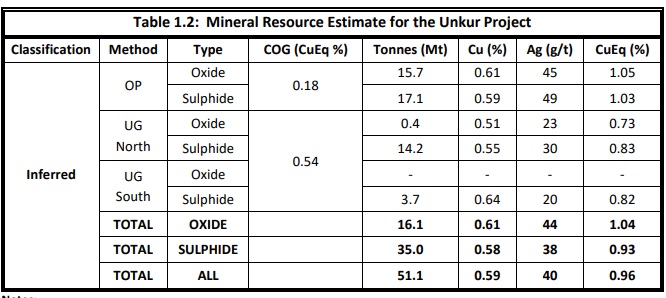

Azarga Metals (AZR.V) was able to release an updated resource estimate and Preliminary Economic Analysis on its Unkur Copper-Silver project in Russia. The new economic study is based on the updated resource calculation which contains 51.1 million tonnes of 0.599% copper and 40 g/t silver.

The economic study is based on a 4 year open pit mine life at an annual throughput of 2.75 million tonnes (using a SART plant for the oxidized material), followed by an underground mining scenario for about 10 years at an annual throughput of 2 million tonnes per year. The total mill feed will be just under 32 million tonnes, which represents about 60% of the total resource estimate. As the total resource remains open along strike and at depth, one could anticipate additional tonnes being added to both the future resource updates as well as the mine plan.

The initial capex is budgeted at US$152M but the sustaining capex is about 65% higher at US$249M as the company has deferred the capex for the underground mine later in the mine life and hopes to be able to fund the majority of the underground development expenses using the cash flows from the open pit phase.

The average annual production will be about 25 million pounds of copper per year as well as 2.8 million ounces of silver, and the silver credit helps to keep the C1 production cost of the copper low at just 30 cents per pound of copper, using a silver price of US$25/oz to calculate the by-product revenue.

Using the base case scenario copper price of US$3.86 per pound and a silver price of US$25/oz, the after-tax NPV8% is estimated at US$206M while the IRR comes in at 27%. Using a more aggressive pricing scenario of US$4.54 for copper and $28 silver, the NPV jumps to US$380M while the IRR increases to just over 44%.

The Unkur project still is a small project as the total amount of recovered copper and silver will be just over 350 million pounds and just under 39 million ounces respectively.

Interestingly, the company also looked at an open pit only scenario where it would be in production for just 4 years. This would result in an NPV8% of US$95M and a 46% IRR based on the consensus price. So this could be an interesting way to sanction the project for the first phase, and the company can (in theory) remain uncommitted to the underground mine scenario for the time being. Of course, the combined open pit and underground approach results in the highest NPVs.

Disclosure: The author has no position in Azarga Metals. Please read our disclaimer.